Apr 24, 2017

Strategy Bulletin Vol.180

Forces behind a stronger yen have disappeared

– The next Abenomics rally is imminent

The global stock market correction that began in the second half of March may have been simply a technical pullback in the wake of the Trump rally (higher stock prices, interest rates and dollar). The correction is probably near the end in terms of the length and size of this downturn. In addition, worries about geopolitical instability have settled down for now because of the increasing likelihood that Emmanuel Macron, who supports the EU, will win the French presidential election. Two completely unexpected events occurred in 2016: Brexit and Donald Trump’s victory. Although people expected stock prices to plunge, prices instead moved up rapidly following these events. The conclusion is clear. Geopolitical uncertainty is nothing more than an excuse for a technical sell-off and actually creates an excellent buying opportunity.

(1) The global stock market rally will continue as the economy remains strong

The unusual upbeat outlook of the IMF

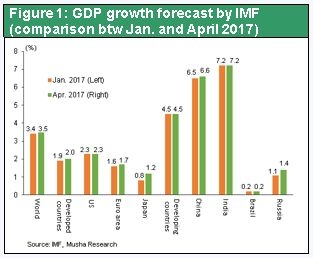

On April 18, the IMF announced a small increase in its outlook for global economic growth in 2017 to 3.5% from the January forecast of 3.4%. The IMF stated that the global economy is gaining momentum and may now be at a turning point. This demonstrates that economists have become very confident about the outlook. Growth projections were raised significantly for Japan, where the forecast increased from 0.8% in January to 1.2%, and for Britain, where the forecast increased from 1.5% to 2.0%. Among industrialized countries, the United States has the highest 2017 economic growth forecast at 2.3%. Overall, a worldwide economic upturn is taking place as the economies of all areas of the world strengthen.

Global economic growth will continue

Earnings are increasing rapidly as companies benefit from innovation and higher productivity made possible by the information and Internet revolution. Strong earnings are very likely to spark a worldwide investment boom. In the United States, expectations about the Trump administration’s business-friendly posture have greatly improved corporate sentiment. The small business optimism index is close to an all-time high of about 104 since December 2016 after remaining between 88 and 96 following the global financial crisis. US interest rate hikes have started, but there is still a firm commitment to monetary easing. Moreover, there is a large volume of money available for investments worldwide and interest rates are low. This environment has greatly increased the animal spirits of entrepreneurs. A recovery is occurring in the natural resource, energy and mining sectors as the price of crude oil climbs. In addition, the high-tech economic cycle is entering a growth phase after stagnation in late 2015 and early 2016. Major reasons are the completion of high-tech product inventory reductions, an improvement in the product cycle, and the rapid growth of semiconductor and LCD investments in China. In Japan, both internal and external demand are fueling growth in orders for semiconductor manufacturing equipment, electronic components and machine tools.

Worldwide risk-on sentiment and a resumption of rising US stock prices

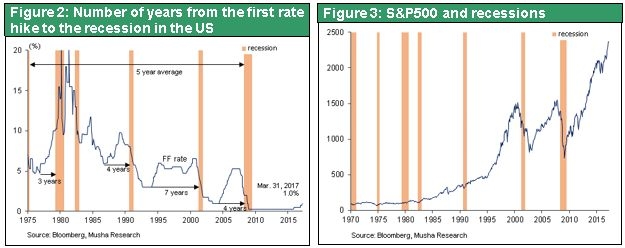

One key point about the outlook is whether or not China continues to use fiscal and monetary measures to support the economy even after the Communist Party National Congress this fall, an event that happens only once every five years. Nevertheless, the current global economic expansion will probably continue for the time being. The primary reason is that there is no need for significant monetary tightening. Inflationary pressure is minimal as information technology advances and low wages in emerging countries hold down wage increases. In the United States, a recession typically begins anywhere from three to seven years after the first interest rate hike. Five years is the average. Since the first hike was only a little more than one year ago, a recession is unlikely to start for several years. Furthermore, experience tells us that stock prices will not reach a peak as long as the economy is growing. We must therefore conclude that the current stock market upturn still has a long way to go. Therefore, the recent drop in stock prices was most likely merely a technical correction after the Trump rally. Pullbacks in interest rates, stock prices and the dollar are all likely to reverse direction once they have run their course in terms of the length and size of these downturns. At this point, about 80% of the correction is probably behind us. US interest rates are very likely to increase. The primary reasons are sound US economic fundamentals along with Fed interest rate hikes, expectations for tax cuts and rising prices, including the price of crude oil. Consequently, the dollar will probably continue to appreciate for many years.

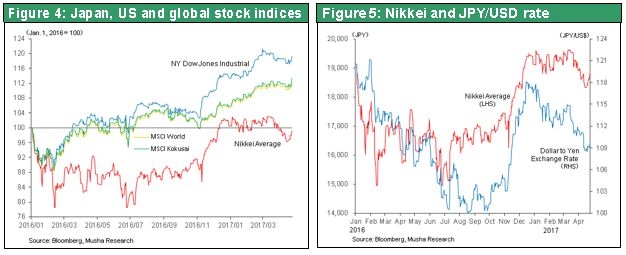

If US stocks climb to new highs again, upward pressure on the yen by risk-off sentiment will be limited. As a result, any appreciation of the yen will probably go no farther than about ¥108 to ¥110. As I explain in the next section, almost all reasons for a stronger yen have disappeared. Japanese stocks are now poised to join the global rally led by the United States.

(2) Japanese stock market volatility will be amplified by the yen exchange rate link, leading to more speculation

The extreme volatility of Japanese stocks

No major stock market in the world is more volatile than Japan’s stock markets. During the recent correction, stock prices in Japan fell more than in any other major stock market. The reason is the link between stock prices in Japan and the big swings in the dollar-yen exchange rate. In a risk-off environment, investors sell Japanese stocks because of declining US stock prices as well as the yen’s appreciation. In a risk-on environment, investors buy Japanese stocks because of rising US stock prices as well as the yen’s decline. The result is bigger upturns and downturns. These characteristics make Japanese stocks an ideal place for speculators.

There are three primary reasons.

- Foreign speculators account for a large share of stock market trading in Japan = Foreigners hold 30% of stocks but generate 60% to 70% of trading volume, about 90% of which is estimated to be speculative.

- Foreigners are probably using forex hedges for about 20% of their investments. When stock prices are climbing, investors sell the yen for these hedges. When stock prices are falling, investors buy the yen to close out their hedges. This buying and selling increases the volatility of the yen-dollar exchange rate. = Japanese stock market capitalization is ¥580 trillion and foreign ownership is 30%. Multiplying foreign ownership by a 20% forex hedging rate results in a hedge position of ¥35 trillion. Therefore, a 5% drop in stock prices in Japan produces ¥1.7 trillion of demand for buying the yen, which reinforces the link between forex and stock prices.

- Japan has net foreign assets of $2.9 trillion, more than any other country. One reason is the massive amount of foreign security holdings of Japanese investors. = As a result, foreign exchange rate volatility increases when market sentiment shifts to risk-on or risk-off.

Japanese stocks will quickly reverse direction once the yen peaks

Linkage between forex and stock prices is likely to continue for some time. That means the outlook for the dollar-yen exchange rate is critical to determining an outlook for Japanese stocks. Three major factors influence stock prices in Japan. First is US stock prices, which are an indicator of the global appetite for risk. Second is Japan’s economic fundamentals. Third is the dollar-yen exchange rate. For these reasons, if a global risk-on environment emerges and US stock prices climb, prices of Japanese stocks are very likely to move up even more.

(3) Reasons for a stronger yen have largely disappeared

Fundamentals and supply-demand dynamics no longer point to a stronger yen

Foreign exchange rates have a decisive impact on stock prices as well as the entire Japanese economy and this vulnerability creates some problems for Japan. The most significant cause of Japan’s deflation was the rapid appreciation of the yen that took place under the leadership of the Democratic Party of Japan prior to the start of Abenomics. Today, ending the yen’s appreciation once and for all is vital to ending deflation and achieving an economic recovery. As I explain more thoroughly below, the disappearance of almost all reasons for the yen to strengthen has created the best possible environment for the Japanese economy and investing in Japanese stocks.

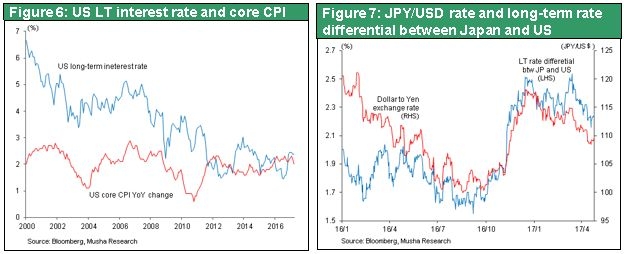

From the standpoint of fundamentals, the dollar is unquestionably stronger than the yen. The US economy is growing faster and interest rates are moving up. On the other hand, Japan is forced to adhere to extreme monetary easing, with long-term interest rates at zero, because of the threat of deflation. The US long-term interest rate pulled back from a peak of 2.6% to 2.1% during the Trump rally correction. As the gap between US and Japanese interest rates narrowed, the dollar briefly declined and the yen appreciated. However, a further decline in US long-term interest rates is unlikely due to the sound US economic fundamentals. They can probably go no lower than 2.1% or 2.2% of the core CPI inflation rate. As a result, the interest rate gaps between Japan and the US will expand again from here.

US long-term interest rates will rebound

Fundamentals are the fundamental cause of the recent rapid decline in US long-term interest rates. First, US economic indicators started weakening in March. Job growth slowed and retail sales, the industrial production index and housing starts were all down from February. Second, the first quarter GDP growth rate is expected to decrease to about 1% because of the nature of standard seasonally adjusted statistics (an advance estimate of the growth rate will be announced on April 28). Third, the increase in the CPI slowed in March (core CPI was up 2.0% YOY vs. 2.2% over the prior 12-month period) because of a slower growth rate of imputed rent and a decline in communication and apparel prices from February. The consensus among economists is that all these figures are merely noise rather than a sign of a change of direction in the economy. The US long-term rate will probably bounce back.

Japan has no trade surplus and enormous external investments – Strong demand for the dollar

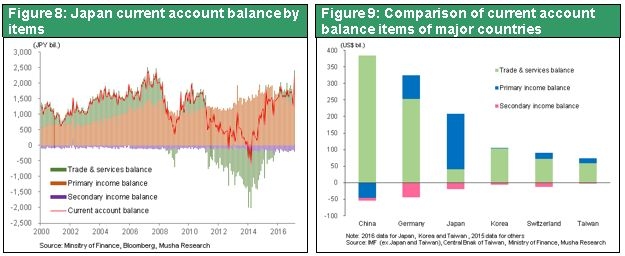

With respect to real demand, there is almost no demand for selling the dollar and buying the yen because Japan’s exports and imports are almost the same. However, there is a huge current account surplus of ¥20 trillion, which is 3.8% of Japan’s GDP. Most of this surplus is the primary income balance, which has almost no effect on the supply and demand of currencies. Primary income is mainly the earnings, interest and dividends that Japanese companies receive from overseas investments and loans. But companies are reinvesting most of this income overseas rather than bringing it back to Japan. Therefore, overseas investment income does not create upward pressure on the yen because companies use these funds mainly in the original currency or dollars without converting into yen.

Furthermore, Japan’s institution investors and individual investors alike cannot ignore the high US interest rates as these investors look for places to park their money. As the yen was weakening in 2016, the dollar premium for basis swaps increased rapidly, but now it has declined sharply. This will probably be another reason for the high level of overseas investments by Japanese securities investors, which will in turn greatly raise demand for dollars. For these reasons, there are almost no logical reasons for the yen to appreciate from the standpoints of the dollar, the yen, economic fundamentals, and currency supply and demand dynamics.

The Trump administration’s illogical attempt to weaken the dollar will quickly end

Why are people afraid that the yen will appreciate? The answer is most likely worries about the Trump administration’s pressure on foreign exchange rates. On April 12, President Trump said the dollar is too strong. At the G20 finance ministers meeting as well, the United States worked on limiting the depreciation of currencies of other countries. However, the Trump administration’s desire to weaken the dollar is logically flawed. Moreover, this stance is completely inconsistent with US interests. Consequently, President Trump will have no option other than to terminate this stance eventually.

President Trump’s misunderstanding of this issue is a disgrace. Three common-sense economic principles underpin the exchange rate debate. First, the US trade deficit is not a problem and there is no need for so-called corrective actions. Second, internal US factors (notably the balance between investments and savings) are responsible for the trade deficit (current account deficit). The blame cannot be shifted to other countries. Third, a trade balance cannot be altered by using foreign exchange rates. Perhaps President Trump is simply saying things that he hears from Ford and other companies. Eventually, he will probably realize that others made him play the role of a clown. US Treasury Secretary Mnuchin has stated that a strong dollar is in the best interests of the United States, and this is going to become evident. (More information about this point is in Strategy Bulletins 173 through 176.)

Good current account income balance – Bad current account trade balance

In general there is no reason to be critical of Japanese current account surplus because most of it is the primary income balance. The current account balance consists of the trade balance for goods and services and the income balance. Goods and service exports represent the export to other countries of items produced in Japan. As a result, there is some truth to the view that countries with a trade surplus are stealing jobs that should otherwise exist in other countries. However, an income surplus is the result of income from business and investment activities by Japanese companies in other countries. These activities create jobs, so other countries should be grateful to Japan.

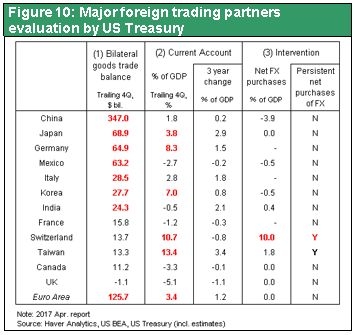

Figure 9 compares the composition of the current account surplus in countries with large surpluses. As you can see, the causes of this surplus can be completely different. For example, Japan has a surplus because of its primary income surplus but the current account surplus in other countries (China, Germany, Korea and others) is mostly the result of a trade surplus. This is why other countries should be appreciative of Japan’s surplus while the surpluses of China, Germany, Korea and other countries deserve criticism.

No reason exists for US pressure on Japan about the yen

There were concerns in the Japanese government and in financial markets about inclusion of the “foreign exchange problem” in the dialog between Deputy Prime Minister Aso and Vice President Pence concerning the US and Japanese economies. But there is no need to worry. Japan’s exports and imports are generally balanced, but the trade surplus with the United States is $68.9 billion, the second largest after that of China. So we cannot say that President Trump is unjust only because he has made an issue of the surplus with the United States.

However, trade surplus criticism is itself inconsistent with economic principles. Sound arguments are needed to end the misunderstandings of the Trump administration and the people at financial markets who are influenced by this administration. Saying the trade balance of only two countries is a problem is a mistake. The mistake is compounded by going on to say the imbalance can be corrected by changing foreign exchange rates. Japan definitely has a big trade surplus with the United States. But Japan also has big trade deficits with oil-producing countries. If altering an exchange rate could end a trade imbalance, then the yen should become much stronger in relation to the dollar. The same argument also means that the yen should become much weaker in relation to the currencies of oil-producing countries. This is impossible because most oil-producing country currencies are linked to the dollar. Consequently, the exchange rate adjustment argument quickly reaches a dead end.

The global economy is rooted in a framework in which oil-producing countries have massive trade surpluses and their currencies are pegged to the dollar. All of these points clearly demonstrate that criticism of Japan’s US trade surplus and calls for reducing this surplus by boosting the yen’s value are positions that are utterly groundless and illogical.

Only China deserves to be subjected to foreign exchange pressure

China is the only country where there is a legitimate reason for the Trump administration to talk about a foreign exchange rate problem. For many years, China used interventions to keep its currency artificially low and build up a huge trade surplus with the US. During the past two years, China has instead been selling dollars because of the significant risk of a big drop in the yuan’s value. But this shift has not ended China’s foreign exchange problem. The United States has very good reason to be wary about China becoming even more price-competitive if nothing is done to prevent a sharp downturn of the yuan.

The most recent foreign exchange report of the US Treasury Department states that the yen is undervalued by 20% in relation to the average yen exchange rate for the past 20 years. The report concludes that there is no evidence the yen is overvalued. But this is not appropriate. During the past 20 years, the yen became very strong and Japan’s ability to sell products at competitive prices declined. Japan went from having the world’s largest trade surplus to a country with largely equal imports and exports. This environment decimated Japanese manufacturers of finished electronic products like semiconductor chips, LCD televisions and smartphones, sectors that were at one time a core strength of Japanese industry. The yen’s exchange rate over the past 20 years was a form of punishment for Japan. Using that rate as the standard for today’s foreign exchange rate discussions is unjust and illogical.

The importance of the hysteresis effects of exchange rates

Over a period of many years, there is no doubt that exchange rates have a substantial influence on the international division of labor. For example, no one can deny that China’s enormous trade surplus is the result of years of interventions to keep the yuan far below its fair value. Similarly, Japan’s trade surplus plunged because the yen stayed far above its fair value. Japan needs to ensure that the United States fully understands how exchange rates cause changes of this magnitude over many years (the hysteresis effect). Today, the yen is weaker relative to the dollar compared with the historical average exchange rate. But it is unfair to compare today’s rate with the past two decades when Japan was being punished by a strong yen. We can expect to see a dramatic easing of the upward pressure on the yen once the mistaken perception among economists and market participants about the yen being undervalued relative to its prior-year level is corrected.

The link between exchange rates and the division of labor as well as the new trade theory must be understood

A key element of the new trade theory, for which Paul Krugman received a Nobel Prize, is the hysteresis effect on the international division of labor. The level of exchange rates was a critical channel for this effect. The use of the strategic trade theory to justify trade friction with Japan was an example of the use of the new trade theory in actual policies. This succeeded at making the yen appreciate significantly. The Trump administration is now trying to use this same successful approach in its current trade negotiations with China. (The nomination of Robert Lighthizer, who was a central figure involving Japan-US trade friction, to be the next US trade representative is proof of the Trump administration’s intention to put the new trade theory to work again). I would like to discuss these points more thoroughly at another time.