Jun 02, 2017

Strategy Bulletin Vol.182

Are people correct to say this economic upturn has matured and stocks are overpriced?

Low inflation and the ability to manipulate the yield curve give the Fed more power to avoid a recession

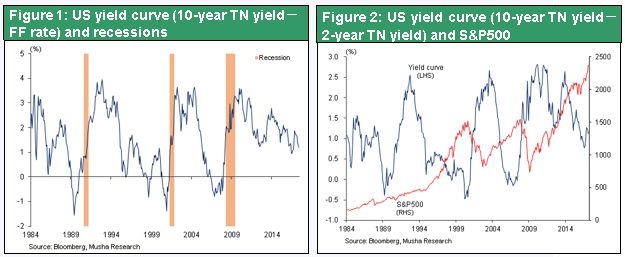

People are wondering if the economy has matured and stocks have become overpriced. But this view is obviously wrong. In the May 31 Daily Report, Ed Hyman, one of the most trusted US economists, stated that economic growth will continue as long as inflation is under control. This is because inflation would result in monetary tightening. Mr. Hyman alluded to a well-known August 1997 statement by Professor Rudiger Dornbusch that no post-war recovery died of old age. The Fed murdered every one of them.

The same progression of events has occurred repeatedly during the post-war era without exception. Rising concerns about inflation lead to excessive monetary tightening. The result is an inversion of the yield curve and ultimately a recession. Consequently, worries about a recession should not surface as long as there is no need for tightening to the point of making short-term rates higher than long-term rates. Furthermore, the Fed’s power is not limited to short-term interest rates. The use of tapering (changing the size the Fed’s balance sheet) gives the Fed considerable influence over long-term interest rates, too. As a result, like the Bank of Japan, the Fed has also gained the ability to control the yield curve. These factors make it very unlikely that we will see an inverted yield curve in the near future.

Low inflation and interest rates are not indicators of a weak economy

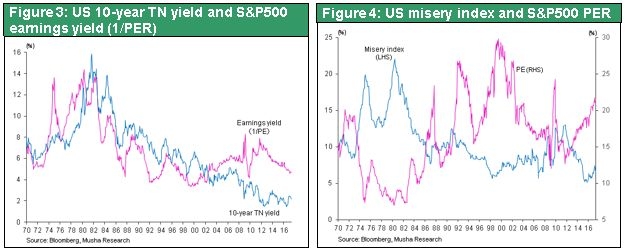

Although these points cannot be denied, there are still doubts created by the length of this economic upturn and the high valuations of stocks (PER of 18.3 compared with the historic average of 15.5). However, as Professor Dornbusch stated, the duration of an economic expansion is in no way related to the economy’s maturity. Economic expansions last anywhere from three to 10 years after WW2, and no one knows this time. Moreover, the PER alone is not the absolute standard for determining if stock valuations are too high or low. As you can see in Figure 3, changes in the US earning yield (the reverse of the PER) between 1970 and 2000 mirrored movements of the long-term interest rate. This leads to the conclusion that the long-term interest rate determines the proper level for the PER. Therefore, today’s low long-term rates can be used to justify a very high PER.

The historical factors that justify a high PER

Central banks use quantitative easing to control long-term interest rates. Therefore some people refuse to believe that a high PER can be justified by low rate simply because long-term rates are manipulated. However, as Figure 4 shows, there is a strong inverse correlation between the PER and the misery index (unemployment rate + inflation), which is a highly reliable indicator of the economy’s health. When the US misery index was at an all-time high in 1980 (hitting a peak of 22% in June), the PER of US stocks fell to a record low (dropping to 6.96 in April). With the misery index currently at a historic low, no one should be surprised to see the PER well above its historic average.

The shift from high-wage intellectual labor to low-wage manual labor

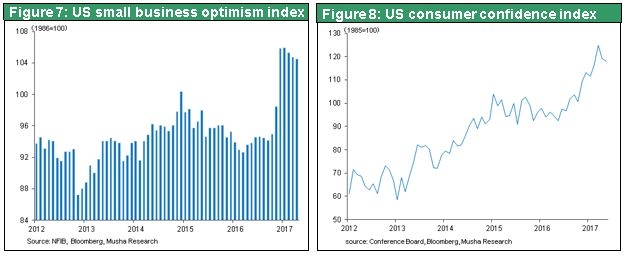

Minimal inflation and low long-term interest rates are regarded as signs of economic weakness by some people. They believe this environment will cause stocks and the dollar to decline. But this view is inconsistent with the facts. With a 4.3% unemployment rate, the US is unquestionably at full employment. One explanation is that a decline in the labor participation rate is responsible for low unemployment. However, the United States has added an unprecedented more than10 million jobs during the current economic expansion. Obviously, the supply of labor is becoming tighter year after year.

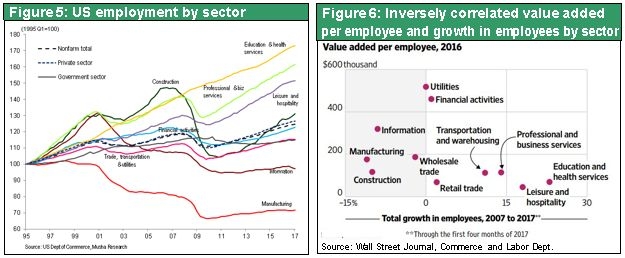

Wages are climbing at an increasing pace. Nevertheless, wage increases and inflation are still below the Fed’s inflation target of 2%. The reason is that most job creation is occurring in categories with low productivity and low wages. A structural shift is taking place due to the absence of job creation in high-productivity categories. The Internet and high-tech revolution has rapidly reduced the need for intellectual workers. At the same time, demand for manual laborers has grown.

In the US retail industry, the market share of e-commerce has increased from 3% 10 years ago to the current 9% and is expected to climb to 30% over the next decade. Growth of e-commerce is creating a severe shortage of truck drivers and other workers engaged in delivery services. A similar situation exists in Japan. There are high rates of both job creation and wage increases in low-wage categories and low job creation and wage increases for intellectual workers.

Figure 6 clearly shows the inverse relationship between per capita value-added and job creation. Machines replaced manual laborers during the first industrial revolution. Now, the Internet and artificial intelligence industrial revolution is about to replace intellectual workers with machines. As intellectual workers are replaced, the increasingly limited supply of manual laborers will create a long-term upturn in wages for manual jobs. This trend is likely to reduce the income gap between intellectual and manual workers significantly. In Thomas Piketty’s capitalism, there is an inevitable widening of the income gap. But this outlook shows that signs of the limits of Piketty capitalism are starting to appear.

The historical factors with rising savings and capital productivity have produced low interest rates

This discussion raises the question of whether or not low long-term interest rates are the precursor of a recession. In other words, are falling interest rates the result of declining demand for capital investment caused by increasing pessimism about the future? Business sentiment and consumer sentiment alike have improved dramatically since Donald Trump’s election victory. This big improvement in sentiment in two key components of the economy contradicts the belief that pessimism about the future is rising. Then how do we explain the low level of interest rates?

Demand for places to invest money is growing because of the worldwide surplus of savings and the big increase in US household and corporate savings. But rising demand is accompanied by a large drop in the cost of investments linked to technological progress involving the Internet, cloud computing and other fields. This is most likely the explanation for low interest rates. Growth in surplus savings and an upturn in capital productivity are occurring simultaneously. It is this structural shift of historic proportions, which is unfolding against a backdrop of a robust economy and high corporate earnings, that is responsible for today’s extremely low interest rates. No major change in these events is likely to occur even if the Fed starts downsizing its balance sheet.

For these reasons, we can regard low inflation and low interest rates as factors that will reinforce the sustainability of the ongoing economic expansion. Also, this reasoning can be used as the justification for a strong stock market rally. Furthermore, even though the current environment makes it difficult for long-term interest rates to move up, there is no reason to expect that low interest rates will cause the dollar to weaken and the yen to strengthen.