Sep 03, 2014

Strategy Bulletin Vol.123

Hope not disappointment for policy driven Japanese equities

(1) Will disappointment about Japan be dispelled?

The Japanese stock market rallied on September 2 driving stock prices to their highest level since January on the news that former Chief Cabinet Secretary Yasuhisa Shiozaki was likely to be appointed Minister of Health Labour and Welfare in the coming Abe Cabinet reshuffle. Mr. Shiozaki has been driving discussions on the GPIF's reform. In addition, the dollar recorded its annual high on ISM data that showed that the U. S. economy was buoyant. Obviously, two factors, government policy and the brisk U.S. economy, are having a significant impact on Japan’s stock market and the Yen.

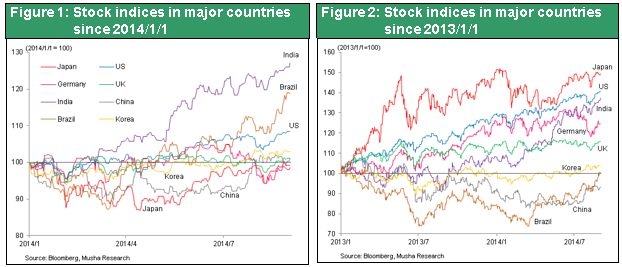

The performance of Japanese equities since the beginning of the year has been the worst of any market globally, and much-trumpeted Abenomics has run out of steam

Up to last week, there was a sense of disappointment in the performance of Japanese equities. From the beginning of last year (start of 2013), the performance of Japanese equities had been the strongest in the world, but it has posted the steepest decline recorded globally since the beginning of this year (start of 2014). Indeed, overseas investors were merely spectators of the Japanese equities markets at present. Declining expectations for Abenomics seemed to have become the prevailing view in the pages of the Financial Times, the Wall Street Journal and other US and European financial newspapers. It's certainly true that the trend towards economic recovery recorded since the second half of last year seems to have come to an end as a result of the hike in the consumption tax rate in April. April-June GDP recorded a huge year-on-year drop of 6.8%, and the rate of recovery has been sluggish following a surge of demand since last year that had anticipated the introduction of the higher consumption tax rate. The bad weather recorded this summer has of course been a further negative for consumer spending this year. Although it's likely that, from the July-September quarter on, we can expect to see growth get back on track following the disappearance of the temporary disturbance caused by the hike in the consumption tax rate, it is still undeniably the case that it won't be particularly strong. I don't think there's any doubt about the ultimate success either of the drive to escape deflation or of Abenomics itself, but market consensus is not prepared to go that far as yet. The government will have to come up with additional policy initiatives to ensure that the current bull market driven by a weak Yen continues.

Impossible to close our eyes to the post-consumption-tax change in tone

The problem seems to be that the effects of the first arrow have run out of steam. During the period in which the success of Abenomics in having a beneficial effect in the real economy was evident an indispensable change in market prices (share prices, and in the Yen rate) was achieved, but over the course of the last year absolutely no such change has occurred. Inflationary pressure was starting to dampen down in response to the cessation of the rise in import prices. It is now looking as if it will be extremely difficult for the Bank of Japan to achieve its inflation target of a 2% rise in prices in 2015. The Bank of Japan watches the UTokyo Daily Price Project Index very closely and the rate of decline in this index has been accelerating sharply since June. Surely this decline in inflationary pressure can no longer be ignored? In fact it really looks as if, with things as they are, it will become necessary to shoot the first arrow again at some point. The central banks of the USA and the UK have been continuing with quantitative easing policies in an attempt to inject some animal spirits into decelerating markets, and they have been rewarded with expansion in their real economies. In the UK, a hike in the consumption tax rate (from 17.5% to 20%), and cuts in annual expenditure in 2011 adversely influenced an economy that was unable to emerge from the after effects of the Lehman shock, but from the latter half of 2011 onwards the Bank of England was able to take control of this situation by expanding its policy of quantitative easing. Bank of Japan Governor Kuroda has continued with a positive attitude towards a consumption tax rate hike and stressed that the negative impact of the higher tax rate would be mitigated by monetary policy. Surely, when the feasibility of a further 2% hike in the consumption tax rate is being deliberated upon towards the end of the year, even the Bank of Japan will find it impossible to countenance further sluggishness in the markets.

(2) ‘Low interest rates = monetary policy for capital surplus’ being questioned, source of differential from world equities lies in this policy

Cause of interest rate reductions lies in policy to solve capital surplus

Although US equities prices are recording new record highs, concerns about equities linger worldwide. The main reason for this is that bond yields are declining sharply because growth in economies across the world remains inadequate. The decline in the long-term interest rates for the major nations was not anticipated by most market participants, and the consensus view at the beginning of the year was that interest rates would rise and so would share prices in a great rotation scenario, but the reality is that, conversely, bond prices are rising, and that share prices are underperforming relative to bonds. The decline in interest rates has been particularly evident in Europe and has been especially striking for the sovereign debt of countries in the south of Europe. Right up until last year, long-term bond yields for Spain and Italy, whom it was feared might break away from the euro, were roughly equal to those of the USA or had even fallen lower. Yields on German Bunds dropped below 1% for the first time in history. What does this global decline in yields mean?

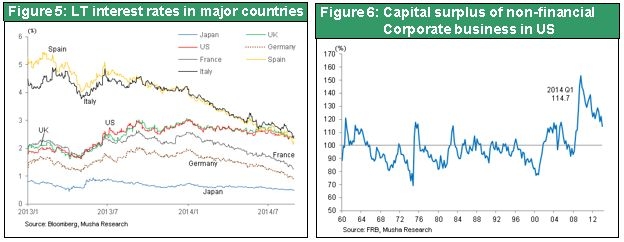

The view that a general decline in the latent growth rate and a worsening in other economic forecasts lie behind this fall in interest rates is too superficial. This decline in interest rates - global interest rates - indicates weakness in demand for funds, in other words ‘slack’ in demand for capital. Why has this ‘slack’ increased to the point where it has become a problem? I think the root cause lies in an increase in corporate capital and in rising labour productivity. The new industrial revolution of IT, smart phones, cloud computing, and other factors, is propelling globalisation, driving up productivity to unprecedented levels, and dramatically reducing the volumes of capital and labour inputs required. In other words these trends are simultaneously delivering remarkable increases in corporate earnings but also producing ‘slack’. The progress made in IT technology is also resulting in a dramatic decline in machinery prices. Moreover, the benefits of globalisation are greatly lowering the costs of building factories in developing countries. This in turn is facilitating huge reductions in the amounts of capital that companies need to invest in their businesses. It has long been the case that, in both the USA and in Japan, companies no longer need to reinvest amounts equal to all of their depreciation and amortization expenses. Figure 6 illustrates the trend in capital surpluses (cash flows in excess of capital expenditures = capital surplus) in the US corporate sector, and we can soon see that, since the start of the noughties and particularly so in the wake of the 2008 Lehman Shock, a capital surplus culture has taken hold. Leading companies like Apple and Google having gigantic capital surpluses is becoming the norm. Popular opinion analyses the decline in US Treasury yields as representing declining profit margins (diminished ability for companies to generate earnings), but the reality is that capital surpluses are therefore piling up in place of high margins, and this can be said to be the factor that's driving long-term interest rates down (for a more detailed analysis, please refer to our Strategy Bulletin No. 121 of 2 June 2014 ‘Why declining US Treasury yields are causing share prices and the dollar to rise’).

Why is quantitative easing correct?

If this is the case, then ‘putting the capital ‘slack’ that exists in the markets to work’ must be a sound and appropriate policy approach. If this unutilised capital slack exists, then surely by lowering capital costs further this can be put to use to enhance social welfare economically. According to former Federal Reserve Chairman Bernanke, a well-established monetary policy = quantitative easing that is creative, and so he set the elimination of ‘slack’ in the economy as one of his policy targets but ‘slack’ does not refer merely to labor but also to capital. The reality is that surplus labor and surplus capital are two sides of the same coin and they move in lockstep. In actuality, situations in which there is a labour surplus can also be described as situations in which there is a capital surplus. Thinking about it in these terms, depressed or declining long-term interest rates, since they represent the existence of surplus capital that can be used, are actually a good thing. The problem is determining whether policies that can put this surplus capital to use in an effective manner are being adopted, or whether policies are being followed that obstruct this aim. If the former, then share prices will rise. If the latter, then share prices will fall, and so it is reasonable to say that the equities market is now in a situation in which it is greatly reliant upon monetary policy.

Disparity between share prices and economic performance being driven by policy

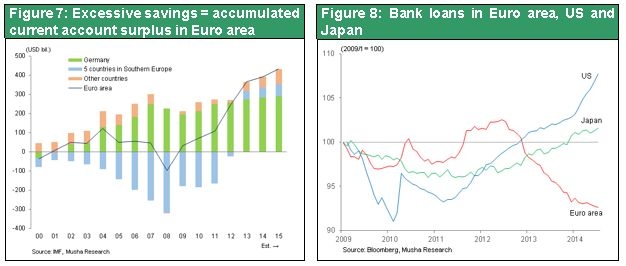

There is a great degree of difference in the share price performances of the advanced nations and to a certain extent this depends upon whether or not policies are in place that are able to make effective use of capital surpluses. US equity prices are recording new highs, and it is clear that because appropriate demand policies are being implemented the outlook for the economy is bright as discussed below. In Europe, on the other hand, share prices have been faring poorly and interest rates have been declining dramatically as demand remains sluggish and assets remain underutilised in response to government budgetary constraints and austerity in monetary policies. The countries of southern Europe have eliminated their savings deficits and massively reduced both their budget deficits and their external deficits by dramatically lowering their standards of living over the course of the euro crisis. But because Germany and the countries of Northern Europe continue to maintain huge external current-account surpluses and have neglected demand creation, the capital surplus for the euro zone as a whole is rising still higher. Consequently, it can be said that the euro zone as a whole lacks policies to counter this combination of lack of demand and surplus capital. Moreover, the banking revolution in the Eurozone is lagging behind and bank lending continues to decline as a result of strict restrictions on capital. The fact is that the effects of the quantitative easing undertaken by the ECB are not being felt outside of the banking system. Consequently, it may be said that if, once financial constraints are eased in Europe too, and the ECB embarks upon a programme of quantitative easing, stress testing for banks is completed this autumn, then there is plenty of surplus capital available to be directed into the real economy. Japan is also stuck in a situation in which share prices have stagnated in response to the instability caused by the negative impact of the hike in the consumption tax rate, but I think that the adoption of additional quantitative easing policies would completely transform this situation.

(3) Pessimism being dispelled by fiscal policy contribution, shift to second stage of long-term rising wave for Japan shares

US share prices to continue to record new record highs on cyclical recovery in the economy

Firstly, it looks likely that the United States will take the lead in the global economy and in achieving higher share prices. The FRB (Federal Reserve Board) is expressing this cyclical optimism in claiming that capital and labor surpluses can be eliminated by rising growth rates in a post-QE (quantitative easing) cyclical recovery. One way of thinking about the situation is that the economic cycle in the US economy, although the current rate of economic recovery is slow, can be described as being still in the fourth or fifth innings, but that this also only goes to show that there is still plenty of time left until the ninth innings. This is illustrated by the following three factors: (1) it contains plenty of as yet unsatisfied latent demand in the areas of housing and capital expenditures; (2) now that the increase in wages has begun to pick up steam, this factor will continue to be linked to a virtuous cycle driving up household incomes; and (3) the extreme youthfulness in the credit cycle. Despite this economic environment however, there is no sense that share prices are high in relative terms. By applying PBR (price-book ratio), the most basic yardstick for assessing share price valuation, US share prices are the highest amongst the countries of the developed world at just under 3x, but this can hardly be described as excessive given that the ROE (return on equity) of US companies is also so high. Given that the dividend yield is 1.9%, and the share buyback ratio is 3.2%, this means that companies are delivering a huge 5.1% return on current market capitalisation to shareholders - a very high rate of return and one that is equivalent to double the yield on US Treasuries. This healthy rate of value creation by US companies indicates that there is plenty of equity value and that, for the time being, it is therefore unlikely that the current rising trend in US equity prices will be reversed.

Japanese equities to also shift to second stage of rising wave in response to strong corporate earnings and the impact of policy intervention

Japanese companies possess the power to be able to continue to maintain an underlying tone of substantial growth in profits from this point on. This is due to the fact that efforts to recalibrate their business models will pay off handsomely over the long term (please refer to our Investment Strategy Focus No. 296 of 10 June 2014 ‘It hasn’t been 20 lost years but 20 years of model conversion’). Japan's deflation is a deflation of prices for services and wages, and so the victims of this deflation have been the services and other domestic demand oriented industries and workers. The fact that it now appears certain that the economy has finally broken free from deflation also means that the probability is increasing that the services sector and its workers (= consumption) are finally enjoying a come-back. This factor combined with further quantitative easing and reform for the sake of third arrow growth should result in a boost both to Japan's economy and to its share prices.

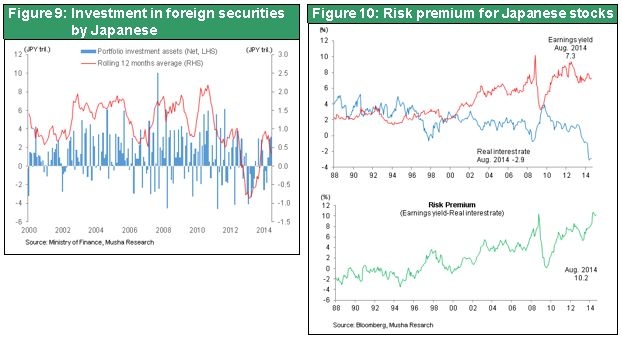

The QE2 supplement to the first arrow anticipated for this autumn should deliver a further round of Yen weakness and share price strength. Although the outlook for the real economy remains unclear, the combination of the consensus that deflation has finally been escaped and the GPIF reform and the portfolio revisions have become a must, adds up to an environment that must surely drive a major transformation in asset allocation by Japanese domestic investors. In a deflationary environment, the holding of cash, government bonds, and similar so-called safe assets is in fact the worst possible asset allocation decision, and one in which ‘Cash is King’ changes to ‘Cash is the Worst’. The shift to investment in risk assets by Japanese investors is also likely to have an impact on the stalemate in the dollar-yen market. Japanese investors increasing their overseas investments translates into pressure towards yen weakness. The Y15 trillion-trade deficit, in addition to the acquisition of and direct investment in overseas companies by Japanese companies, if accompanied by increased overseas investment activity by individuals, pension funds, and insurance companies, would result in truly huge pressure towards yen weakness. Negative real interest rates are providing a further tailwind towards shorting the yen (= the establishment of yen-denominated liabilities positions). Furthermore, if we factor in the existence of the possibility of global speculative money heading towards betting on yen weakness, then spectacular long-term yen weakness can also be assumed.

Moreover, if confidence in the likelihood of sustained strength in both US equities prices and in the dollar takes hold, then at some point an explosive rise in Japanese share prices can also be expected to start up. With zero returns on bank deposits, and JGB yields of 0.5%, there must surely be a strong possibility of a major shift towards equities offering dividend yields of just below 2%.