Sep 22, 2014

Strategy Bulletin Vol.125

The weaker yen and stronger stocks with no overheating signal a new trend

(1) A new trend is on the horizon

The year-long deadlock is ending

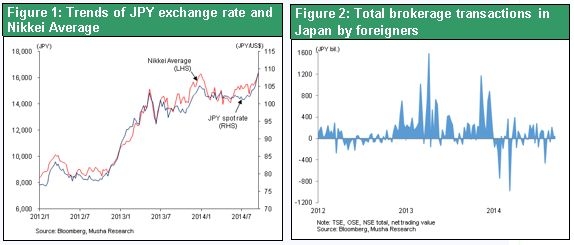

At the end of last week (September 19), the yen reached a new low, falling to ¥109 to the US dollar, and the Nikkei Average rose to a new high of ¥16,321 following the collapse of Lehman Brothers. For the past year, the yen had remained between ¥100 and ¥105 to the US dollar and the Nikkei Average was stuck between ¥14,000 and ¥16,000. Now both have broken out of their respective trading ranges. Investors should view this as the beginning of a new trend. Two factors are responsible for the recent downturn of the yen and upturn in the stock market. First is the outlook for higher US interest rates because of the strengthening economy. Second is the reconfirmation of the determination of the Abe administration and Bank of Japan to execute their financial policies (Prime Minister Abe is determined to implement GPIF reforms and BOJ governor Haruhiko Kuroda said he is confident that 2% inflation can be achieved).

The stance of pessimists has been repudiated

If we believe that a new trend of higher stock prices and a weaker yen has actually started, this signifies the repudiation of two convictions of pessimists. First is pessimism about Abenomics. There was a belief that the stock market rally and weaker yen backed by government policies up to the middle of 2013 ran of steam because of Japan’s worsening economy resulting from the failure of Abenomics. But this stance is no longer valid. The stock market welcomed BOJ governor Kuroda’s statement that the positive cycle of Japan’s economic recovery has not ended despite the temporary downturn following the consumption tax hike. He went on to say that even if worries surface, he believes that a recovery can be sustained and 2% inflation achieved by using additional financial measures. Second is pessimism about the US economy. Pessimists anticipated long-term stagnation of the US economy. They thought that US ultra-easy-money policies would be unable to sustain the economic recovery and job creation. But this belief as well has been rejected.

A new type of central bank initiative is what is underpinning the current economic and financial market rebounds in Japan and the US. The central banks are using quantitative easing to alter the expectations of financial markets. The market seems to have given a vote of confidence to the central banks’ approach. In the US in particular, monetary easing has been entirely directed at achieving the complete use of “slack” (surplus labor and capital). To respond to the emergence and eventual bust-up of an asset bubble and subsequent financial system instability, the US used macro-prudence rather than financial measures. This has extended the reach of monetary easing. The result has been a further increase in risk-taking by market participants.

A resurgence of the yen carry trade, too

The factors that have created this new trend in financial markets are completely different than in 2013. The strongest force behind financial market movements in Japan that year was the carry trade; foreign investors were selling the yen and buying stocks. But now, the primary force is long-term investors within Japan (Figure 2). If in fact the participation of the Japanese investors is responsible for the start of this new trend, the trend may be reinforced by foreign investors and their carry trade of yen-selling and Japanese stock-buying may accumulate more than in 2013. Japan may have reached a stage in which speculative yen sales increase the more that outcries about the yen’s rapid depreciation grow in certain industries and among some economists. In that case, we could see accelerated depreciation of the yen and overshooting of Japanese stocks. Just as in the past when the outcries for persistent speculation regarding a stronger yen were ignored, we saw it go too far in the reverse direction. Financial markets could test Mr. Kuroda’s resolve to see to what degree he can tolerate a weaker yen. If this happens, it will not tie Mr. Kuroda’s hands. On the contrary, a weaker yen and higher stock prices will offset the need for further easing. The expected carry trade in which global speculators sell the yen and buy Japanese stocks is not contrary to the BOJ’s policies. In fact, this carry trade is consistent with the BOJ’s goals. After all, isn’t fueling the appetite of investors for risk precisely the goal of the BOJ’s QQE (quantitative and qualitative easing)?

(2) A perfect environment for weak-yen speculation means no end to the yen’s decline

The yen’s decline may go too far

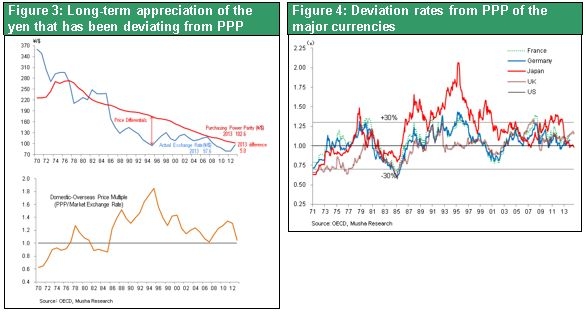

Exchange rates are determined mainly by three components: (1) the speed at which a country prints money; (2) the trade balance (real supply and demand for foreign exchange); and (3) the real interest rate (speculative supply and demand for foreign exchange). Today, all three of these vectors point to a weaker yen for the first time ever. Moreover, geopolitical forces (the interests of the US, the world’s superpower) have shifted to allowing the yen to weaken. These same geopolitical forces had been a reason for the consistent upturn of the yen for 30 years. On a purchasing parity basis, an exchange rate of ¥103 to the US dollar is appropriate. But exchange rate movements always overshoot their marks. As you can see in Figure 4, exchange rate movements of major currencies have gone as much as 30% above and below the purchasing power parity (excluding the yen’s abnormal upturn between 1980 and 2000 that surpassed even 30%). Consequently, we may see the yen weaken to the latter half of the ¥120’s level to the US dollar.

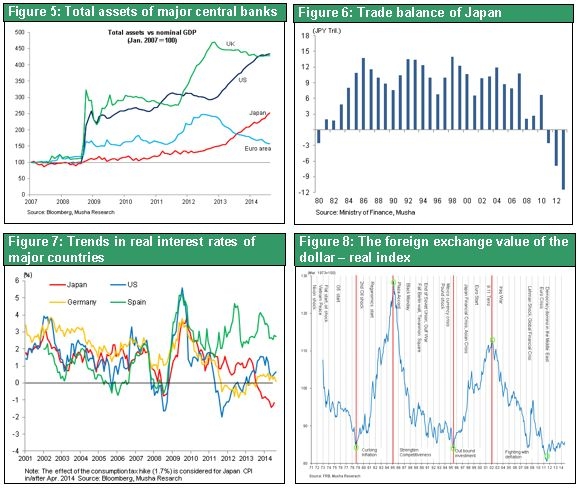

Let’s take a closer look at these decisive shifts in the three major forces that shape exchange rates. The first condition for a weaker yen is the BOJ’s position as the number-one dove among the world’s central banks. Japan’s base money growth rate is the highest in the world. Naturally, the money supply balance is the most fundamental factor that determines the strength or weakness of a currency. The BOJ is printing more money than any other country. This is the biggest cause of the yen’s decline (Figure 5). The second condition for a weaker yen is the unprecedented magnitude of Japan’s trade deficit (annualized ¥15 trillion in 2014). This has generated immense real demand for the US dollar since 2013. In one year, Japan’s importers must buy enough dollars to pay for ¥15 trillion of purchases. Japan had huge trade surpluses for many years. Exporters were constantly selling dollars, which created steady and immense pressure for selling dollars and buying the yen. Now a dramatic reversal has occurred (Figure 6). The third condition is Japan’s real long-term interest rate, which is the lowest in the world and has become negative for the first time ever (Figure 7). But even though Japan had the world’s lowest nominal long-term interest rate, the real interest rate was higher than in other countries because of deflation. A high real interest rate equates to a high cost for loans. Since this motivates borrowers to repay loans faster, the result was a credit crunch of increasing severity in Japan. However, Japan today has the world’s lowest interest rates as well as a negative real interest rate. That means Japan is the easiest place in the world to borrow money. Obviously, taking out a loan means shorting the yen (selling the yen) in terms of foreign exchange transactions. Consequently, the yen has been transformed from the world’s easiest currency to buy into the easiest currency to sell.

The end of the yen’s status as a safe haven

These three decisive forces for a weaker yen show no signs of changing in the foreseeable future. That means the axis for determining the yen’s value has shifted 180 degrees. Until now, the yen was the world’s preeminent safe haven currency. Investors put their money in the yen whenever they wanted to avoid risk. During a risk-off phase, with deflation occurring only in Japan, the yen naturally became more appealing because its real value increased. But now the yen is the currency with the fastest erosion of value because Japan has the world’s lowest real interest rates. In other words, the yen is the currency that investors least want to hold. A momentous shift in the collective perception of the yen among the world’s investors is probably starting to take place. Among Japanese investors as well, a decisive change in perception is about to occur. Until now, households, pension funds, insurers and other Japanese investors shunned all risk by adhering to the “cash is king” belief. But these investors currently have an increasing need to buy more foreign currency-denominated assets as holdings of assets with risk. Japanese investors have been placing too much of their funds in cash, deposits and bonds. We are now likely to see a big increase in their holdings of assets denominated in foreign currencies. Reforms of the GPIF portfolio will probably be the beginning of this shift.

(3) A weaker yen is good for Japan in many ways

Negative effects of the weaker yen will not last long

BOJ governor Kuroda has stated that a weaker yen will not have a negative effect on the Japanese economy. However, concerns about the speed at which the yen is falling are emerging from many sources. One is Akio Mimura, who heads The Japan Chamber of Commerce and Industry, which represents Japan’s small and midsize companies. According to Reuters, Mr. Mimura said “a weaker yen has more advantages than disadvantages for Japan overall. But there are major disadvantages for small and midsize companies and households. If the yen is to fall more, Japan will have to restart nuclear power plants to hold down the cost of energy.”

At this point, the weaker yen has not yet boosted the volume of Japan’s exports. Furthermore, the resulting higher cost of energy and prices of imported goods are lowering real wages. It appears that statements about the harm of the yen’s decline make sense.

The lack of export volume growth shows that Japan’s exports do not rely on prices to compete

All these negative effects will be temporary. A weaker yen is good for Japan for many reasons. Even though the yen is declining, export volume has not increased because most of Japan’s current exports do not compete with other products based on their prices. As a result, Japan does not have to compete by cutting prices. This is why a weaker yen does not lead to price cuts for dollar-denominated exports and a resulting increase in export volume. The absence of export volume growth is therefore proof that Japan’s export structure has shifted to products that are competitive because of technologies and quality rather than their prices. Benefits of a weaker yen are still significant even without growth in export volume. For example, the yen-denominated income of overseas subsidiaries of Japanese companies is increasing because of the lower cost of imports from Japan and foreign exchange gains. This helps support Japan’s current account balance by improving the income balance. Of course, a weaker yen may produce benefits for manufacturing in Japan. In this case, companies may move production activities back to Japan and importers may replace imports with products made in Japan. These events would revitalize Japan’s manufacturing sector. At present, capital expenditures and manufacturing in Japan are sluggish. But this is probably caused by the time lag for benefits to emerge and lingering doubts about how long the yen will continue to fall.

There is no doubt that higher prices caused by the weaker yen will bring down real wages for a while. However, this is nothing more than a process that is required to establish an upturn in Japan’s wages. A weaker yen lowers wages in Japan by the international standards and consequently produces upward pressure on them. It is the same reason that downward pressure on wages increased as a result of the appreciation of the yen. Real income is certain to increase along with wages as corporate income experiences sustained growth.

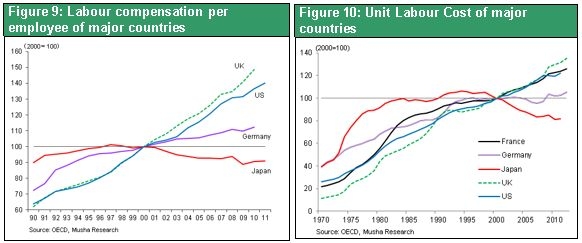

Last week’s issue of the weekly magazine Economist (dated September 16) included valuable analysis (“Stimulative Fiscal and Monetary Policies Have a Downside – Four Miscalculations of Abenomics: Exports, Capital Investment, Personal Consumption and Public Expenditures) by Ryutaro Kono, a leading opponent of reflation. He noted that whether or not a weaker yen or stronger yen is good for Japan’s economy depends on the macroeconomic situation. A weaker yen is preferable when there is inadequate overall demand and substantial slack (idle assets). But he said that there are increasing demerits of the extreme easy-money policy that is fueling the yen’s downturn (because there is no longer any slack in Japan). The first half of this analysis is on target. But I believe the second half is a major misunderstanding of the current situation. During the past 15 years, Japan was the only country where wages decreased (in terms of nominal wages and unit labor cost that factors in productivity). If we regard wages as the best indicator of supply and demand for labor, then we cannot reach the conclusion that Japan has no surplus labor (Labor shortages are limited to certain industries such as construction and there is a substantial labor surplus when it comes to administrative jobs). Moreover, Japan has the world’s lowest nominal and real interest rates. Since interest rates are the best indicator of supply and demand for capital, that means Japan has the largest amount of surplus capital in the world. Therefore, market prices in Japan indicate that there is significant slack (surplus capital and labor) in the Japanese economy. It may be that the estimate of this gap deviates from actual conditions because there is considerable room for arbitrary decisions regarding the calculation of the supply-demand gap. Market prices show that Japan has substantial slack and, according to Mr. Kono, a weaker yen is thus desirable.

The favorable cycle of a weaker yen raising earnings

If we believe that a further decline of the yen is inevitable, the Abenomics goal of ending deflation will be accomplished. The reason is that a weaker yen is a decisive factor that fuels inflation and boosts corporate earnings. The sustainability of corporate earnings is critical for determining the outlook for the economy and stock market. Earnings are the origin of changes in employment, wages (and thus consumption), investments by companies and stock prices. Firmly establishing the yen’s downward trend will be vital to achieving sustained growth in earnings in Japan today. Obviously, more quantitative and qualitative easing by the BOJ will be essential to keeping the yen on its downward track. And there are absolutely no worries about this either.

The forecast for the fiscal year ending in March 2015 calls for record-high corporate earnings in Japan with earnings climbing 10% over the prior fiscal year. Actual earnings may be even higher if the speed of the yen’s decline increases.

I hope that mounting criticism of the yen’s decline will not cause any weakening of Japan’s ongoing monetary easing and initiatives aimed at ending deflation.