Jan 01, 2015

Strategy Bulletin Vol.132

The two primary targets for investors in 2015: Japan and the US

Happy New Year from Musha Research!

A fabulous 2015 – The start of Japan’s full-scale resurgence has arrived

A favorable economic environment of unprecedented magnitude has emerged for Japan. We may never see this again. Even when Japan was posting its fastest economic growth, a powerful US economic recovery, robust Japanese government support for economic growth, a weakening yen, cheap crude oil and other events we see today did not all happen at once. We are able to take advantage of this favorable environment precisely because there was a business model transformation of Japanese companies. This switch did in fact take place during the difficult times of Japan’s so-called ’lost 20 years’. Companies succeeded in moving from price competition to a focus on technology and quality, while companies and the people of Japan endured considerable hardships. Now, the benefits are beginning to appear. This is why I believe that 2015 will be a fabulous year when Japan will benefit from good fortune and timing, geographic superiority, and solidarity among its citizens.

From the standpoint of investing, financial markets in Japan have so far almost entirely ignored this good news. Stocks are extremely undervalued. I think we are about to see the type of stock investing opportunity that comes around only a few times in one’s lifetime.

I wish you all a healthy and prosperous 2015.

Ryoji Musha

January 1, 2015

Focus on Japan and the US in 2015

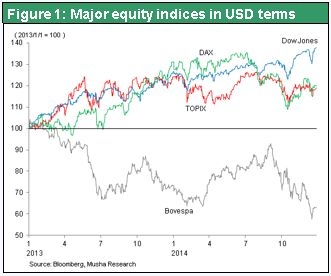

In 2015, we will see changes first in financial markets, then in the real economy, and finally in the socio-political environment. Financial will be a leading indicator and socio-political thinking will be a half-step behind. From a financial standpoint, 2014 was a year when the US was the world’s sole winner from start to finish. Japan, which was far behind the US, slowly took off. In 2015, these two countries are likely to be the global leaders in economic growth. On a dollar basis, stock prices were down an average of 2% worldwide in 2014. The only increase was in the US, where stock prices rose 9%. Next was Japan with a 5% downturn followed by declines of 6% in emerging countries, 8% in the UK and 9% in the EU. Let’s take a closer look at the key points about Japan and the US, the two primary targets for investors in 2015.

(1) The full-throttle US economy; US dominance becomes increasingly clear

US core competences are head and shoulders above others

In the news, we often hear about the unpopularity of the Obama administration and the decline of US global influence. Despite all this talk, I believe that the US will show the world its overwhelming strength in 2015. The country’s superiority is increasing in many respects: 1) unquestioned influence regarding political and military policies; 2) ICT revolution leadership and control of cyberspace; 3) a dominant position regarding financial matters; 4) global leadership in energy thanks to the shale gas revolution; and 5) leadership involving the determination of policies (as the only industrialized country that ever succeeded in using market functions to create credit). The strength of the US economy will become an increasingly critical theme during 2015.

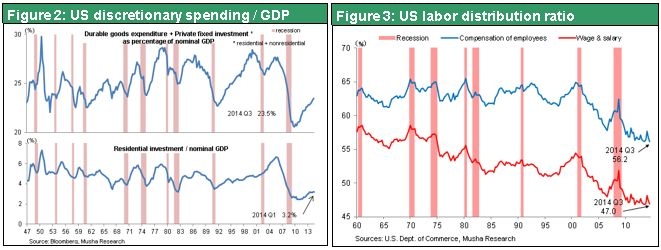

Relentless US quantitative easing has led to accelerating economic growth and the dollar is now starting to reveal its true strength. The primary reason for this cyclical upturn of the US economy is that discretionary spending (consumer durables, housing, capital expenditures, etc.) is still insufficient (Figure 2). Over the next two or three years, I expect to see even more growth in US demand as pent-up demand is released, especially for housing and capital expenditures.

The cyclical rebound is only at the half way point or slightly more

For the second reason behind the cyclical US economic recovery, investors need to determine if the US has advanced to the stage where higher wages are fueling solid growth in consumption. In past economic cycles, there is a well-established pattern. During a recovery’s first half, labor’s share of income drops as companies hold down wage increases. But during the second half, wage growth accelerates (rising labor distribution ratio) (Figure 3). This leads to a big jump in spending and even faster economic growth. Applying this pattern to the US economy today indicates that the economy has reached the turning point where the labor distribution ratio has stopped falling and is about to start climbing. We can therefore expect to see US consumption increase as wages move up.

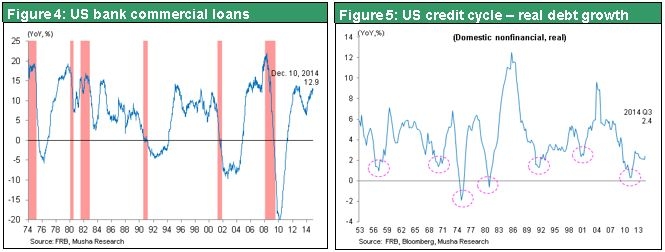

The third reason is that the US credit cycle has entered an expansion phase. Credit growth and the economy generally move together in a cycle that spans 10 years. The credit cycle hit bottom in 2011 and is now in only about its third year of recovery (Figure 4, 5). Since this cycle is still young, we will probably see more growth in credit. That means there is substantial potential for more economic growth. Stock prices are very unlikely to peak before the economy reaches its peak. Consequently, a US stock market rally and the strong dollar will probably be the engines that fuel global risk-taking in 2015.

(2) Japan will be rewarded for its hard work in 2015

The sacrifices of Japan’s workers and savers are about to be rewarded

I believe that Japan will stage a powerful economic rebound in 2015. Good luck does not last forever and neither does bad luck. Success without meaning will inevitably break down while failure with meaning will be rewarded. When investors formulate their 2015 strategies, they should search for where these empty successes have occurred and where meaningful events are still waiting to be rewarded. Thus far, Japan is the country that has the most significant unrewarded events with positive undertones. But we will probably see substantial rewards come to the surface in 2015. In this context, the rewards will be higher wages and a lower risk.

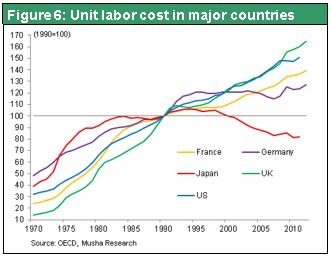

High productivity and low wages (low unit labor cost) = Much room for wage hikes

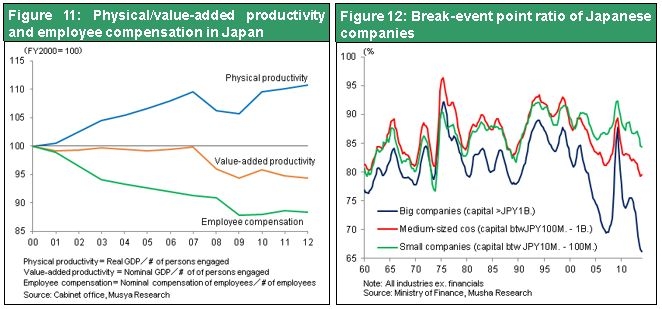

Examining the balance between accomplishments and benefits requires determining if the two key sources of economic input, providers of labor and providers of capital, are being rewarded in an appropriate manner. For labor, this is a question of whether or not workers are being properly compensated for their efforts and receiving wages that reflect the results of their jobs. Unit labor cost, which is wages divided by productivity, is the key factor. As unit labor cost figures in Figure 6 show, Japan clearly ranks first in the world. No workers anywhere have been more poorly compensated for their efforts than in Japan. With respect to the viewpoint of ’people get what they deserve’, this indicates that there is substantial potential for wages to rise in Japan.

Rebounding earnings and low stock prices (high risk premium) = Substantial upside potential for stocks

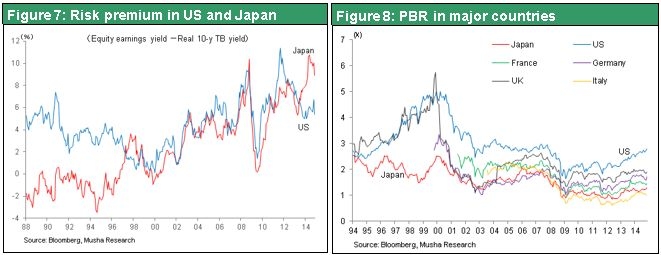

The next question is whether or not providers of capital are receiving suitable compensation. The best indicator for answering this question is the risk premium for stocks. To determine this, we can look at the difference between the return that capital providers demand (a) and the cost of capital (b). Watching changes in the difference between the earnings yield (a) and real long-term interest rate on Japanese government bonds (b) is an easy way to monitor this risk premium. Based on this simplified stock risk premium, we can see that Japan’s risk premium is much higher than in the US (Figure 7). Furthermore, Japan’s risk premium is at an all-time high (other than during the volatility after the Lehman Brothers collapse). A high risk premium tells us that even though companies are producing sufficient returns on capital, shareholder value (the result of stock prices) is low and the high returns on capital are not being properly distributed to shareholders. The resulting undervaluation of stocks means that there is substantial room for an upward correction of stock prices. Moreover, a high risk premium is a sign that the cost of procuring capital is extremely low in relation to the ability of companies to use capital to generate profits.

Where have the surplus earnings gone? Funds for a business model conversion

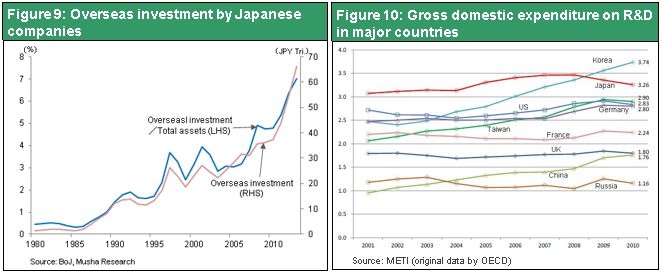

In Japan, companies have been efficiently utilizing both labor and capital. But the people of Japan (workers and savers) have not received any benefits. At first, this may appear to be extremely unfair for Japan’s workers and savers. This situation should have resulted in surplus earnings for companies. However, the earnings of companies in Japan were low until about 2012 even though there obviously should have been substantial extra profits due to the availability of cheap labor and capital. There are two causes for this disparity. First, buyers took surplus earnings away from companies as selling prices and export prices dropped because of deflation (falling CPI and asset prices) and the yen’s strength (Figure 11). Second, companies used their extra earnings for developing technologies and investing in overseas operations in order to transform their business models (Figure 9, 10).

However, as I have just explained, this period of transition is almost over. First, the end of strong-yen deflation in Japan means that buyers are no longer taking surplus earnings away from companies. Second, Japanese companies have largely completed the business model transformation process. Companies now specialize in high-tech, high-quality products and have constructed global supply chains. As a result, the problem of high cost structures is no longer significant. In other words, Japanese companies have at last reached the point where the surplus earnings from their ability to use cheap labor and capital can start to drive rapid earnings growth. This is evident in the steep decline in the break-even point of companies in Japan. The resulting record-high earnings distributions by companies will probably fuel a favorable economic cycle in 2015. In more specific terms, we can expect to see the start of a powerful upturn in wages accompanied by a rapidly shrinking risk premium as stock prices and interest rates increase.

Japanese companies have acquired many growth drivers

Looking back from this vantage point, we can see that Japan’s “lost 20 years” were actually a time when the country was putting together the conditions required for growth. Amid considerable headwinds, Japanese companies were able to:

1) Streamline operations and cut costs on an unprecedented scale

2) Create a business model centered on developing advanced technologies and providing solutions (unifying manufacturing and services)

3) Establish global networks and become citizens of the world

4) Accumulate large volumes of capital (resulting in an enormous capacity to make investments; ample capital is a critical condition for progress, as can be seen by the success of investments by Fuji Film)

All of these accomplishments were made possible by the sacrifices of workers and savers that I discussed earlier. Now that the days of a strong yen and deflation are over, the benefits of these accomplishments are starting to emerge in the form of powerful earnings growth. Consequently, I believe that 2015 will mark the beginning of a favorable economic cycle in Japan as companies in Japan distribute their strong earnings. Benefits will finally reach the people of Japan in the form of higher wages for workers and higher stock prices (and eventually higher interest rates) for savers.

Changes in Japan’s trade structure demonstrate the business model shift

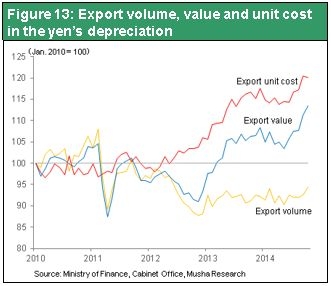

The transformation of the business model used by Japanese companies is altering the composition of their foreign trade. In the past, a weaker yen boosted the Japanese economy by enabling companies to cut dollar-denominated export prices. Lower prices led to higher overseas market share and export volumes, which increased manufacturing in Japan. But as the yen weakened this time, there has been a big increase in export unit cost while export volumes stayed low, as you can see in Figure 13. Japanese companies are no longer using prices to compete. Yen-denominated export unit cost have increased significantly because there is no need to cut dollar-denominated prices even when the yen weakens. On the other hand, a weaker yen no longer sparks a favorable economic cycle created by higher production volume. This is because companies do not engage in price-based competition when the yen falls, so there is no growth in export volumes. In the past, Japanese companies used a beggar-thy-neighbor business model of using price competition to capture market share. Now, these companies have completed the transition to the business model of avoiding competition by specializing in products that are superior in terms of technologies and quality. Switching to this model has not produced trade friction. Instead, the result is very strong demand in other countries for the high-tech, high-quality Japanese products that are vital to progress in these countries. Another result of the new business model is higher earnings at Japanese companies.

In 2015, price-volume synergies will give a big boost to earnings and ROE

There will probably be a large increase in Japan’s production volume in 2015. The first reason is the shift of manufacturing back to Japan. One sign of this shift is the annualized decrease of 5% in imports from China since the summer of 2014. Loans to fund capital expenditures at small and midsize companies in Japan, which have been competing with Chinese companies, are currently increasing. In addition, machine tool orders in Japan are nearing an all-time high. The second reason is the outlook for a big improvement in trade volume. A number of companies are bringing manufacturing back to Japan. For instance, Toshiba and Micron Technology (Elpida Memory) are expanding their factories in Japan. The third reason is that domestic demand is increasing now that the negative effects of the April 2014 consumption tax hike have come to an end. Synergies produced by higher production volume and higher selling prices are likely to trigger economic vigor in Japan reminiscent of the country’s era of rapid economic growth.

Underpinned by these solid fundamentals, Japan appears to be poised to advance in 2015 to the second sweet spot of what I believe is the “market of the century” that began in November 2012.