May 11, 2015

Strategy Bulletin Vol.139

Buy in May – Signs of the beginning of a favorable cycle are emerging

(1) Buy in May to be ready for the summer rally

The Nikkei Average has recently been moving sideways just below ¥20,000. May is typically a period of stock market volatility, which is why people often say “sell in May.” Investors appear to be bracing themselves because of the uncertainty of how much current sources of uncertainty will bring down stock prices. A negative impact on the stock market could come from Greece and the euro problem, concerns about China, a possible U.S. interest rate hike and its effects, and the balance of payments at some emerging countries.

However, investors have been aware of these problems for some time. Stock prices have factored in this uncertainty each time a problem occurred. Moreover, circuit breakers are in place to prevent a deepening crisis with regard to Greece, China and a U.S. interest rate hike. A sharp rise in interest rates is the only real reason to worry. Higher interest rates would cause bond prices to plunge, resulting in unexpected losses for some investors and financial institutions. If proceeds from sales of bonds are held as cash, financial instability could grow. But if these funds go to stocks and other investments with risk, there would be no reason at all to worry because the risk tolerance of the entire market would increase. Furthermore, in the current environment of global monetary easing, there is almost no possibility that investors will hold their money as cash. The conclusion is that there are no reasons for a major sell-off in May. In addition, we have not seen any of the usual seasonal stock market movements this year. For example, there was no January effect and the Japanese saying that stocks are high in early February (setsubun) and low in the middle of March (higan) did not hold true. Consequently, becoming too cautious is itself dangerous because investors may miss a buying opportunity.

Supply-demand and the economy are robust

There are two reasons to be positive about Japanese stocks. First is the strong improvement in Japan’s real economy. The economy has passed the “green shoots” stage and is now showing signs of a full blossom. Investors will probably become even more confident about Japanese stocks because of the even more solid geopolitical backing following the successful U.S. visit by Prime Minister Abe. Second, a favorable supply-demand balance is expected to continue. In 2013, net purchases of Japanese stocks by foreigners totaled ¥15 trillion. These investors were quiet during 2014. But during the first four months of this year they added ¥2 trillion of Japanese stocks to their portfolios. Nevertheless, the underweighting of Japanese stocks among foreign investors is still significant. Individuals have been major sellers of Japanese stocks with net sales of ¥12 trillion in 2013, ¥5 trillion in 2014 and ¥3 trillion during the first four months of 2015. The Government Pension Investment Fund, pension funds, insurance companies and other institutions are buying more Japanese stocks, too. Overall, investors in Japan and overseas probably have a massive volume of funds that are available for buying Japanese stocks. Although there may be a small dip in stock prices, May should be regarded as a time to make purchases in order to be ready for the coming summer rally.

(2) The emerging indications of a favorable cycle

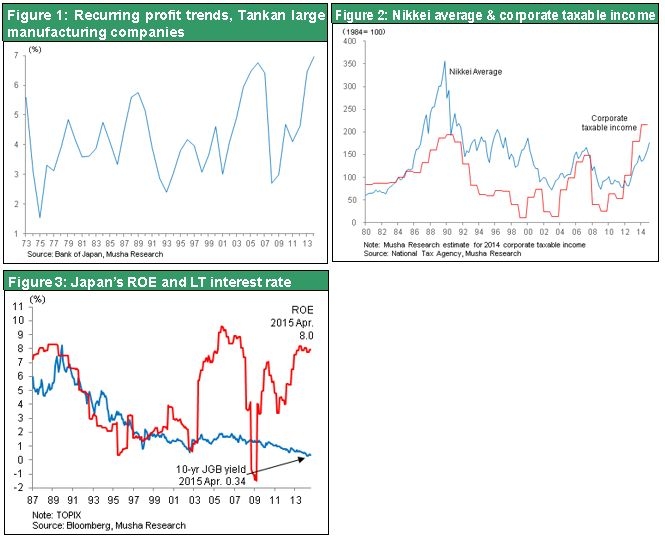

Unprecedented strength in earnings and a big increase in ROE

Many signals are appearing that point to broad-based economic growth in Japan. Most important of all is corporate earnings. Sales and earnings rose about 15% to 20% in FY2014 and will probably continue to grow at this pace in FY2015. In the most recent Bank of Japan Tankan report, the outlook for the ordinary profit margin at large companies is a record-high 7% for FY2014 and FY2015. This margin was only 5.8% in 1990, the peak of Japan’s asset bubble years. The current profit margin clearly demonstrates the magnitude of improvements made by Japanese companies. Furthermore, the aggregate income declared by Japanese companies, which was at about the break-even level early in the previous decade, rose to almost an all-time high in FY2013. In FY2014, aggregate declared income will probably set a new record that is far higher. Obviously, these companies have become much more profitable. Additionally, the ROE will probably move even higher as companies buy back stock and boost dividends.

Not long ago, volume rather than earnings was the basis for competition among companies in Japan. Earnings were small because companies wanted to increase market share and sales volume. But Japanese companies have shifted their emphasis from price-based competition to superior quality and technologies. As a result, companies have business models that prioritize earnings. The upturn in profitability is likely to continue for some time, and strong earnings will probably lead to a favorable cycle. Until recently, companies in Japan were cautious. They held on to their earnings to be prepared for unexpected events. After the global financial crisis and a number of other crises, executives believed that they needed a substantial financial cushion. Companies retained most of their earnings and the amount of cash on the balance sheets of Japanese companies rose to more than ¥200 trillion (40% of Japan’s GDP). Therefore, companies were able to earn profits, but these earnings did not lead to the creation of more demand. In 2015, a big change is likely to occur concerning this lack of demand creation.

This year, companies will probably start to aggressively use their ample cash reserves for capital expenditures, R&D programs and other activities. We can also expect to see growth in M&A activity. Companies in Japan are under pressure to improve how they manage their finances. Pressure comes from shareholders, who want a higher ROE, and from the expectations of the Japanese government. Boosting ROE will require the effective utilization of the capital that companies can hold. Shareholders will not support a company that puts its money in savings deposits with no return regardless of how much cash the company has. But if a company uses these funds for an acquisition or other new investment, the 0% return may become a 10% return. This is why M&A activity may increase significantly.

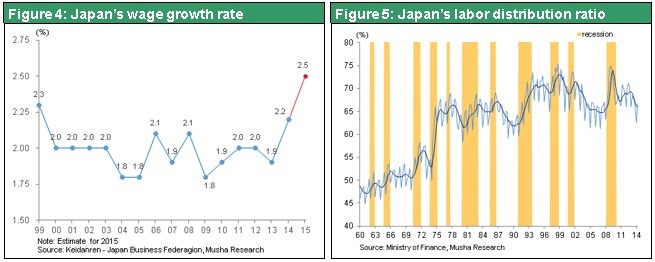

A significant increase in real wages

Rising wages will be one of the most important favorable cycles created by strong earnings. The 2015 spring wage increases will probably result in a total increase of about 2.5%, the combination of a 0.6% to 0.7% increase in base wages and a wage increase of about 1.7% for age and years of employment. After deducting inflation of slightly more than 1%, this translates into a real wage increase of approximately 1.5%. This is the largest increase in real wages since 2000 and these wages can be expected to fuel a high level of consumer spending. Even after these wage hikes, labor’s share of income at Japanese companies is still at the 61% level, almost an all-time low. That means companies can still afford to pay their employees more. As a result, we will probably see a big increase in bonuses for employees.

The big improvement in trade volume is finally starting

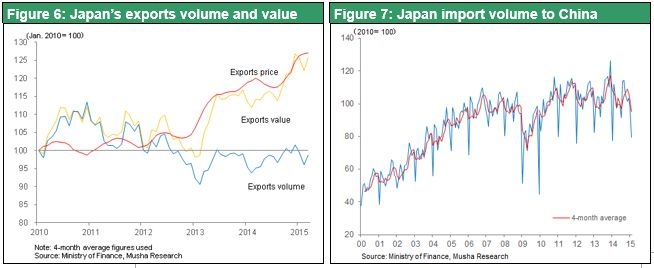

One more emerging sign of a favorable cycle is the big improvement in Japan’s trade statistics. In March, exports posted a big increase of 8.5% over one year earlier. Imports were down 14.5%, in part because of the lower cost of crude oil. The result was a trade surplus of ¥220 billion, Japan’s first surplus in three years. Most significant is growth in the volume of exports, which has been flat for many years. In March, the export volume was up 3.3% from one year earlier and the average volume for the past four months was up 4%. At the same time, import volume was down. March import volume from China was 29% smaller than one year earlier. This decline shows that Japanese companies are replacing imports from China, where costs are rising, with manufacturing in Japan. Rising export volume accompanied by falling import volume will probably lead to significant growth in manufacturing activity in Japan.

Improvements in the two key factors of corporate earnings and trade are economic fundamentals that can justify a Nikkei Average of more than ¥20,000.

(3) The reasons behind Yellen’s statement and how it should be interpreted

The real meaning of Fed chair Yellen’s statement

On May 6, Fed Chair Janet Yellen said that “equity market valuations at this point are quite high.” She also said “there are potential dangers there.” Are stocks too high? Are bonds too high? Or are both overvalued? Apparently Ms. Yellen thinks that prices are too high for both stocks and bonds. But what is the real meaning of her statement? Could this be the start of stock price correction?

Wages are rising faster as the U.S. labor market approaches full employment. The Fed has apparently decided to make the first interest rate hike in September or later this year. Therefore, Ms. Yellen most likely made this statement with this timing in order to make investors think about the proper level for stock and bond prices. The aim is to prevent an overreaction by financial markets when interest rates start rising. Ms. Yellen wants market participants to determine a suitable level of prices that factors in upcoming interest rate hikes. This statement will probably have only a negligible effect on the stock market.

Bonds are overpriced but stocks are not

Should we believe that stock and bond prices are too high, as Ms. Yellen told us? My position is that bonds are overvalued and there will be a big increase in interest rates. But I think that stocks are still undervalued.

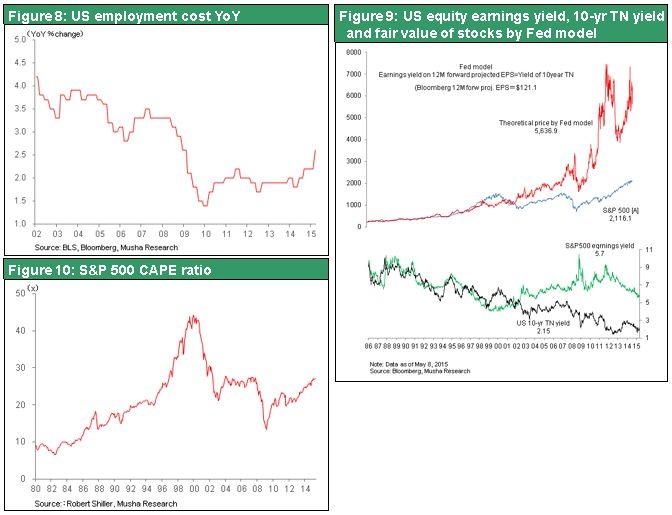

There is no doubt that stocks are not nearly as undervalued as before. Currently, U.S. stocks have a PER of 18, which is higher than the average multiple of 17.4 between 2003 and 2007 prior to the Great Recession. Furthermore, the CAPE (cyclically adjusted price-to-earnings ratio) is approximately 27. This too is high, although still below the level between the IT bubble of 1996 to 2000. However, since stocks are a financial asset, the proper prices of stocks are determined by a competition with the returns of other financial assets (bank deposits, government bonds and other investments). Consequently, due to the current level of long-term interest rates, which equates to a historically low cost of capital for companies, shouldn’t we think that the proper value of stocks (proper PER) is considerably higher?

The graph in Figure 9 shows the fair valuation of U.S. stocks using the Fed model. This is a simple model that assumes the fair value of stocks is when the income return equals the 10-year Treasury note yield. The model was almost completely accurate until 2000, except in 1999 as the IT bubble grew. If interest rates rise and bond prices fall, stock prices will also decline so that their yields become higher. There was a very close arbitrage relationship between the bond and stock markets. Investors were constantly moving fund back and forth between these two markets. Starting in 2000, there has been no arbitrage relationship between earnings and long-term interest rates for U.S. stocks. The absence of this relationship means that there has been no way to measure the fair value of stocks since 2000. Stock prices fell even as the long-term interest rate moved down. The income return on stocks increased to a level that was higher than the 10-year Treasury note yield. This imbalance continued for a number of years and consistently became even greater until 2012. The existence of this imbalance signified that bonds were far overvalued, stocks were far undervalued or that both of these valuation gaps were occurring at once.

The root cause is the gap between profit margins and interest rates

The most basic problems in the United States today are the difficulty of increasing the number of jobs and unusually low long-term interest rates caused by surplus capital. Simply put, there has been significant growth in the surplus of workers and money. Due to this situation, the United States has experienced an unprecedented rise in profitability along with a sharp drop in interest rates. Furthermore, this gap continues to widen. How can there be such a large gap between profit margins and interest rates, which should both be returns on the same capital? Moreover, the difference between the two has been increasing for more than 10 years.

The most likely reason is the big increase in productivity (big decrease in the cost of equipment) fueled by the new industrial revolution. If productivity climbs as the size of the economy remains the same, there will be endless growth in surplus labor and capital that eventually causes an economic collapse. Avoiding this problem requires creating the demand needed for the full use of labor and capital. When surplus labor and capital increased during the Great Depression, mistaken government policies created a negative cycle of shrinking demand. The economic crisis became even more severe as a result. But when the financial crisis started in 2008, then Fed Chairman Ben Bernanke immediately responded to plunging stock prices with a policy for creating demand: quantitative easing. During the Great Depression, there was a four-year absence of government initiatives. But the quick response in 2008 succeeded in limiting the economic difficulties to only a relatively small recession.

The success of the 2008 response clearly demonstrates the critical importance to the economy and financial markets of policy measures when rising productivity creates surpluses of capital and labor.

The Fed will remain the friend of financial markets

Monetary easing implemented by the Fed has established a foundation for the use of all surplus capital and labor. Fed Chair Yellen is making no changes to the stance of her predecessor Ben Bernanke with regard to making demand creation the highest priority. Obviously, the Fed has no reason for monetary tightening, which would trigger market turmoil and bring a halt to the demand creation process that would take place otherwise. In 1937, as the U.S. economy was beginning to recover, the enactment of monetary tightening caused the economy to return to a recession. As a result, there is no doubt that the Fed is wary of tightening too soon.

The Fed will not take any actions to hold down demand or go too far with interest rate hikes or other monetary tightening measures in an environment of surplus capital and labor. This is why we can expect the Fed’s policies to remain friendly for the time being. Ms. Yellen said that in May 2013, a remark by then Fed Chair Bernanke about the start of bond purchase tapering sparked volatility in financial markets. But please note that at that time as well, stock prices continued to move higher although there was a sharp but brief upturn in long-term interest rates after the remark. (Japanese stock markets, which had surged 80% in the six months prior to May 2013, suffered a major downward correction as other stock markets in the world remained healthy. However, Mr. Bernanke’s tapering statement had only a minimal impact on U.S. stock prices.)