Sep 01, 2015

Strategy Bulletin Vol.146

China's tight foreign currency reserves may erode external financial strength and weaken CNY more

(1) China is the Achilles’ heel of global financial markets

Stock markets are volatile worldwide

At this point, no one can deny that China has become the Achilles’ heel of the global economy and financial markets. Worries about financial markets are bringing down the currencies and weakening the economies of resource-producing countries, the ASEAN countries and Asian newly industrializing economies (NIEs). There is only one cause: rapidly slowing economic growth in China. All of China’s key microeconomic indicators have either stopped increasing or started falling. Railway freight volume, crude steel output, electricity generation, and exports and imports (monetary) are a few examples. China’s officially announced economic growth rate of 7% does not reflect the actual state of the economy. People are probably correct to believe that economic growth is slowing. The second sharp downturn of the Shanghai Stock Market triggered drops of 10% to 20% across the world’s major stock markets in only one week. Sales by hedge funds to manipulate prices and generate profits added momentum to the falling prices. But investors must also realize that an economic and financial crisis may be brewing in China.

Dark clouds are not going away

A relief rally is taking place, which is a natural occurrence in the wake of a big drop. Short sellers are buying back stocks and Japanese and other investors are buying stocks as they rebalance their portfolios. For instance, at institutions like the GPIF weight of Japanese stocks has declined sharply as stock prices nosedived in Japan. They need to make new purchases of Japanese stocks in order to raise the equity weightings of their portfolios to the pre-crash levels. This buying will probably greatly improve the supply-demand dynamics for stocks and support a rebound in prices for a while. However, this rebound cannot be sustained unless (1) the Chinese economy returns to steady growth or (2) the effects of China’s economic problems do not spread to other countries. Consequently, problems in China will probably continue to hold down global financial markets until investors know if either of these conditions will be met.

The following section is my attempt to analyze the international balance of payments and net external balance, which are the key factors concerning risks involving China.

(2) Falling foreign currency reserves and net external assets are signs of the rapid growth of the flight of capital

China’s foreign currency crisis grows – Foreign currency reserves and net external assets are both plunging

The balance of external capital inflows and outflows is probably China’s Achilles’ heel. A trade surplus and positive current account balance, both backed by China’s overwhelming competitive edge, fueled economic growth until 2009. But after that, economic growth has been fueled solely by investments. China was able to make these investments because of the massive net inflows of capital. But now a big change is taking place in these inflows. This is China’s Achilles’ heel.

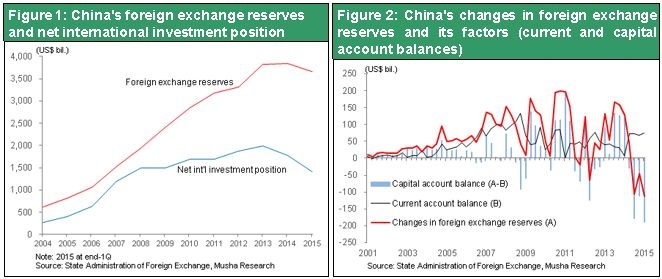

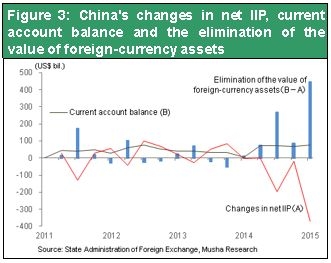

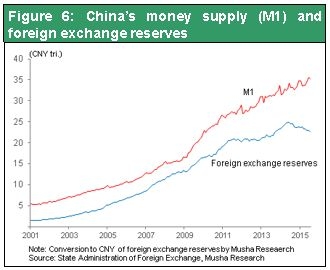

The change in net capital inflows is emerging in the form of a decline in China’s foreign currency reserves. These reserves had been rising steadily. But after peaking at $3.99 trillion in June 2014, reserves retreated to $3.84 trillion at the end of the year. The downturn has continued in 2015 with reserves falling significantly to $3.73 trillion at the end of March 2015 and $3.65 trillion at the end of July. China’s current account surplus was $214.8 billion between July 2014 and March 2015. Despite this surplus, foreign reserves fell by $263.2 billion ($3,993.2 billion - $3,730.0 billion) during the same period. That means China suffered a net capital outflow (external capital balance other than foreign currency reserves) of $478.0 billion during this nine-month period alone.

But the even bigger problem is that there are apparently off-record outflows of capital in addition to the outflows that appear in the statistics. This issue came to light in China’s international investment position statistics, which started using the IMF standard for the first time in June 2015.

China’s out-of-sight capital flight may be growing rapidly

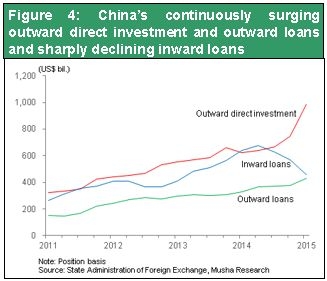

Just as with foreign currency reserves, net external assets have been declining quickly. These assets peaked at $1,996.0 billion at the end of 2013 but were down to $1,403.8 billion at the end of March 2015, a drop of $592.2 billion. Normally, external net assets should mirror the change in the current account balance. But these assets are instead moving in the opposite direction. China’s cumulative current account surplus for 2014 and the first quarter of 2015 was $295.2 billion. Adding the decrease in net assets to this surplus shows that the value of external assets has fallen by $887.4 billion. This is a remarkable figure even if we assume that part of this number is due to foreign exchange losses and other factors. There are four possible causes of this drop in external assets. First is off-record capital outflows (the flight of capital). Second is fraudulent on-the-books figures for capital inflows. Third is the occurrence of enormous losses involving external assets. Fourth is unreliable statistics. However, the flight of capital is probably the only way to explain a loss of this stunning magnitude (assuming that the statistics can be trusted). Furthermore, this decline demonstrates the severity of worries about the yuan.

(3) Falling Foreign Currency Reserves, the Flight of Capital, Reckless Overseas Investments and the Worsening Quality of Capital Inflows

Overseas investments are exceeding China’s capabilities

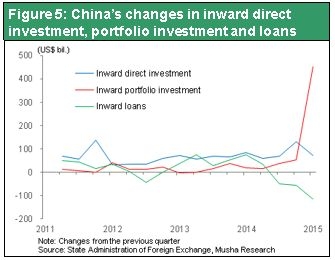

The apparent flight of capital is one cause of China’s falling foreign currency reserves. But two more factors are adding momentum to the country’s worsening foreign currency situation. One is reckless direct investments and loans in other countries. The other is the outflow of capital via the international financial system. No end is in sight to China’s huge external investments under the one region one road concept. Chinese companies are making massive overseas investments and acquiring companies. China’s outstanding balance of external direct investments has grown from $660.5 billion at the end of 2013 to $985.8 billion at the end of March 2015. This is an increase of about 50% over a period of only 15 months. Clearly, China is greatly enhancing its profile in other countries. In addition, China’s overseas loans have grown about 40% during the same period, surging from $308.9 billion to $431.9 billion.

Mounting worries about extending credit to China

This growth in external investments and loans has been accompanied by a big downturn in capital inflows via the international financial system. Loans to China peaked at $677.5 billion at the end of June 2014 and subsequently fell sharply. In March 2015, this figure was only $458.1 billion. Overseas financial institutions are becoming increasingly worried about the bursting of a bubble, falling corporate earnings and other negative events in China. As a result, these institutions are probably more wary about Chinese credit exposure. They are reducing new loans to China while stepping up measures to collect outstanding loans.

Despite these developments, aggregate capital inflows to China have continued to post strong growth through March 2015. Furthermore, China’s external debt has continued to grow rapidly even after the end of 2013 when the country’s external net assets started to decrease. During the 15-month period that ended in March 2015, external debt has grown by an astonishing $986.8 billion (24.7%). This debt was $3,990.1 billion at the end of 2013, $4,137.4 billion at the end of March 2014, $4,316.3 billion at the end of June 2014, $4,491.8 billion at the end of September 2014, $4,632.3 billion at the end of 2014 and $4,976.9 billion at the end of March 2015. At the same time, a major shift is occurring in the channels for capital inflows. Growth in external debt during the 15-month period is entirely due to a $420.3 billion increase in direct investments and a $581.1 billion increase in securities investments (mainly equities). These increases far outweighed the $106.1 billion decrease in loans. Therefore, capital inflows are no longer going through financial institutions, which perform rigorous credit investigations, as investors primarily use direct investments and stock investments. Moreover, apparently the sources of these capital inflows are shifting to mostly individuals or family assets (Chinese and overseas Chinese investors). These are investor segments that often make decisions with little or no due diligence.

Impact of worsening soundness of external debt

Direct investments of $2,751.5 billion and securities investments of $967.6 billion accounted for 75% of China’s external debt at the end of March 2015. Investments through Hong Kong are $2,000 billion of the direct investments and the remaining $700 billion is from various industrialized countries. These numbers clearly demonstrate China’s great dependence on foreign capital, an unstable and unreliable source of funds. If China’s bubble bursts, the resulting damage to the quality of assets of external investors could trigger a negative cycle that stops nearby countries and Chinese investors from taking on more risk. This process would fuel suspicion about the reliability of corporate accounting and government statistics in China, perhaps leading to revisions of various data.

Economic data in the next few quarters may be much worse than expected

The problem is that figures I have just mentioned are as of the end of March 2015. At that time, stock prices were still climbing and there was no widespread awareness of slowing economic growth in China. It is impossible to imagine what kinds of numbers we will see for the end of June (announced at the end of September), which will include the start of the stock market plunge and the yuan’s devaluation, as well as at the end of September (December announcement) and December (March 2016 announcement). Securities investments will undoubtedly fall sharply because of the stock price free fall and direct investments will probably not continue to increase. Furthermore, if we assume that off-record capital outflows (capital flight) has been hundreds of billions of dollars during the past few years, the decline in China’s external net assets and foreign currency reserves will become even more serious. This may further impact market sentiment.

(4) China’s Foreign Currency Situation and Great Reliance on External Capital

China depends on loans for its foreign currency reserves

Why have people suddenly started worrying about China’s external capital? The reason is the mistaken perception of China. The consensus was that China was the most financially powerful country in the world. China has the world’s largest trade surplus and, as a result, the world’s largest foreign currency reserves at almost $4 trillion. This is three times more than Japan, which has the second-highest reserves. But now everyone can see that this view was a mistake. China’s announcement of international balance and external asset statistics based on the new IMF standards has revealed the true situation. Foreign trade made a big contribution to China’s economic growth only until 2007. Since then, investments have been fueling growth. Enormous inflows of foreign currency and loans from other countries have been funding these investments. Growth of these loans was the reason for the rapid growth in foreign currency reserves. And the resulting increase in the money supply made possible China’s recent investments of an unprecedented scale. Foreign currency reserves are the symbol of a company’s external financial strength. But in China, the majority of these reserves may be dependent on money from other countries. If this is true, then we must conclude that China’s external financial power is very weak.

The very different nature of foreign currency reserves in China and Japan

Most people still do not realize that the nature of foreign currency reserves in China and Japan are completely different. These reserves are held by the government in order to make payments in foreign currencies and maintain stability in the foreign exchange market. Japan defines foreign currency reserves as all foreign currency funds held by the Bank of Japan and the Ministry of Finance. Most of these reserves were acquired in association with foreign exchange market interventions in the past. All reserves were funded by Japan’s current account surplus in prior years. At the end of July 2015, Japan’s foreign currency reserves totaled $1.27 trillion. Foreign securities accounted for $1.12 trillion, or 90%, of these reserves and the majority of these securities are US Treasury securities.

China defines foreign currency reserves as central government and central bank holdings of foreign currencies as well as short-term foreign currency-denominated assets of government-owned banks and the private sector. One source of these reserves is the current account surplus in prior years. But loans from overseas are probably a major source of the funding of China’s foreign currency reserves. The Chinese government strictly controls the foreign currency holdings of private-sector and foreign-owned companies. As a result, most of the foreign currency funds obtained from foreign trade, loans from other countries and other sources are deposited in banks. These deposits are most likely included in foreign currency reserves.

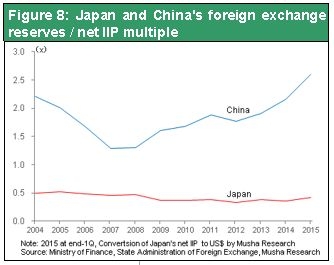

For these reasons, Japan’s foreign currency reserves are only 16% of all external assets. However, these reserves are an unusually high 59% of China’s external assets.

China’s external financial power has been greatly overestimated

Furthermore, we have learned that China’s foreign currency reserves have grown to 2.7 times the country’s net external assets. This is a peculiar situation. Only 37% of these reserves are backed by domestic funds and the remaining 63% relies on foreign capital. Incidentally, Japan’s foreign currency reserves are 41% of net external assets and are entirely backed by domestic funds.

Consequently, even though China’s foreign currency reserves are three times more than Japan’s reserves, the holdings of US Treasury securities are about the same: $1.22 trillion in Japan and $1.26 trillion in China as of the end of July 2015.

As you can see, China’s foreign currency reserves cannot be viewed at all as an indicator of external financial power or the ability to intervene in foreign exchange markets. Net external assets are the true indicator of financial strength. At the end of March 2015, these assets were $2.9 trillion (¥349 trillion) in Japan but less than half at $1.4 trillion in China. Therefore, China’s actual external financial power is only about half of Japan’s power.

There are no strings attached to Japan’s foreign currency reserves. On the other hand, the majority of these reserves in China are linked to a massive amount of debt. Since these are funds from other countries, these reserves cannot be used for foreign exchange market interventions. An enormous volume of loans and investments in China come from overseas Chinese investors and companies. If they start collecting rather than supplying these funds, China’s foreign currency reserves, which have been overstated, could eventually become inadequate.

(5) What will happen if people no longer believe that the yuan will climb forever?

China’s foreign exchange policy faces a dilemma

China’s decision to devalue the yuan despite the above concerns about its foreign currency reserves has destroyed the myth that the yuan will never stop strengthening. Due to this action, Chinese companies will face daunting challenges when attempting to procure funds in international markets. These difficulties will probably increase the pace of the flight of capital from China.

As I explained in my previous report, guiding the yuan downward between August 11 and 13 was a legitimate course of action in response to the weakening of the Chinese economy. China’s exports during the first seven months of 2015 were 0.3% less than the same period of 2014. But exports in July alone were down 8.3% from one year earlier. Unlike in the past, exports have become a drag on economic growth. China’s large cities have the highest wages among the emerging countries of Asia. The erosion of China’s price competitive is becoming even more evident. The strong yuan was detrimental to China’s ability to compete. Furthermore, China must allow the yuan to weaken in order to ensure the effectiveness of its ongoing monetary easing measures. So there is a cause-and-effect relationship. Preserving the value of the yuan as it is subjected to downward pressure from monetary easing will require buying the yuan and selling dollars. However, this market intervention would negate the benefits of China’s monetary easing. The conclusion is clear: a weak economy requires a weaker currency.

However, now that the ever-rising-yuan myth has been destroyed, China’s fundraising activities, which have relied on massive inflows of foreign capital, will face even greater challenges. This will undoubtedly lead to more expectations for the yuan to decline even more. The yuan must depreciate in order to bolster China’s economy. But a weaker yuan will trigger capital outflows in China, where inflows are critical to the economy’s health. Therefore, the Chinese government must deal with dilemma.

(6) Additional anxiety, power struggles and geopolitics.

Internal power struggles and overseas criticism of the Xi regime are fueling anxiety

President Xi Jinping has vowed to crack down on “flies and tigers” (powerful leaders and lowly bureaucrats) in order to fight corruption. But this initiative will inevitably rob the economy of its vitality and make people more averse to risk. In addition, the Xi regime has been prosecuting rivals one after another. The result is the emergence of a personal dictatorship instead of collective leadership of the Communist Party as in the past. This shift may seriously erode the Chinese government’s ability to control the country as well as to manage the current economic crisis.

Geopolitical risk cannot be ignored

Popular opinion about China is hardening in the United States and other liberal democracies. Recently, there was an inflammatory cover story in The Economist titled “Xi’s History Lessons.” The cover page shows President Xi holding a rifle that becomes a pen at the tip of the barrel. The Economist claims that China harbors ambitions of becoming a leading military power and is justifying this goal by rewriting the past to control the future.

China’s Xi regime has the following goals for rewriting history. First, it was the Kuomintang (Taiwanese Nationalist Party) led by Chiang Kai-shek that did much of the fighting against the Japanese. But President Xi wants the Communist Party, led by Mao Zedong, to receive all of the credit for this successful fight. Second, the Xi regime wants to make Japan a villain that invades other countries. In fact, Japan is a peaceful country that has not fired a single shot in anger during the past 70 years. The Xi regime is using these two excuses to justify its military ambitions. The Economist says that China continues to insist that Japan makes light of its past invasions and is exaggerating any threat that China poses. This criticism is aimed at Japan’s conservatives and Prime Minister Abe. Adopting this viewpoint demonstrates that a rapid change is taking place in the stance of The Economist. The article is also evidence of a big shift in the world’s liberal democracies to wariness about China.

The United States is very likely to strongly oppose China’s reclamation and runway and military base construction activities on the Spratly reefs. China has already crossed the red line. How will the Xi regime react? A confrontation over this issue will probably occur when President Xi goes to the United States in September. A method is needed to prevent China from accomplishing its goal. If we assume that direct military action is not possible, then weakening the Chinese economy is the only way to stop China. The top priority of the US government has switched from the economy to geopolitics. People should probably view this switch as a constraint for global stock markets for the time being.

(7) What is the correct short-term view concerning financial markets?

In this report, I have explained why hidden risks involving problems in China are actually quite substantial. But these risk factors will not come to the surface immediately. Also, these risk factors will have only a limited impact on the United States, Japan and Western Europe. China has become a country where overseas Chinese capital, that holds large portion of China’s debt, has gained significant influence. The negative impact will be restricted to countries that rely significantly on overseas Chinese capital.

Furthermore, a global recession is unlikely because economic growth is still continuing in the United States, Japan and Western Europe. In addition, countries are responding to the increase in China-related risk factors and drop in stock prices in many ways. Examples include additional economic stimulus measures, more quantitative easing and more spending. These initiatives should revive stock prices. But China has started enacting extreme measures to prop up the economy, restrictions on capital transactions, foreign exchange controls, and the manipulation of market prices. Most people expect these measures to restore growth and quiet down markets to some extent. For the time being, there is almost no likelihood of a spiraling negative cycle like the one that occurred after the collapse of Lehman Brothers. The stock market will not become a one-way street to lower prices. For the time being, investors should expect to see markets repeatedly make big upward and downward swings.