May 02, 2016

Strategy Bulletin Vol.160

The Danger of a US Beggar-thy-Neighbor Policy

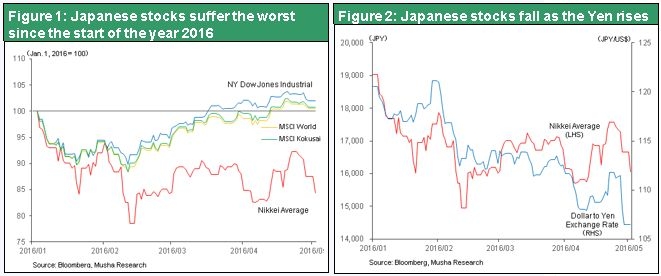

Now we can see the real reason stocks fell only in Japan

As stock markets worldwide moved up starting in early 2015, and especially since March, Japanese stocks were the only losers. Low stock prices in Japan were not justified with respect to the true value of Japanese companies. The cause of this mispricing was an endless negative cycle fueled by the yen’s strength and stock market weakness. Clearly, a plunge in stock prices in Japan would not be mispricing if a severe global economic downturn was imminent. However, an impending downturn would trigger falling stock prices worldwide rather than only in Japan.

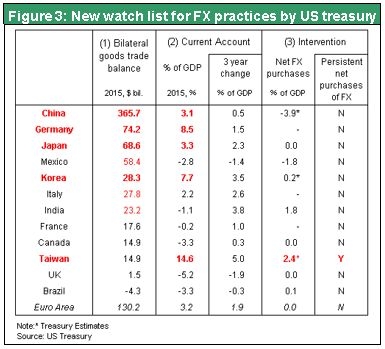

The question we need to ask is why the yen was the world’s only currency that appreciated, a move that was contrary to economic fundamentals and the policies of central banks. Today, the true cause has been revealed: the one-sided changes to the rules by the United States. The US Treasury Department released its semi-annual foreign exchange policy report on April 29. For the first time, this report includes a list of countries that require monitoring and assessments. Sanctions will be imposed if a country is recognized as a foreign exchange rate manipulator by meeting all of the following three arbitrary requirements: (1) a trade surplus with the United States of more than $20 billion, (2) a current account surplus of more than 3% of the country’s GDP, and (3) foreign exchange market interventions amounting to more than 2% of the country’s GDP.

Based on these criteria, the Treasury Department established a Monitoring List with five countries: China, Germany, Japan, Korea and Taiwan. But the problem is that the list is completely ineffective with regard to China and Germany. Only Japan was subjected to significant pressure for the appreciation of its currency. Although a stronger yen may have a big impact on international trade, this pressure is incomprehensible and unjustified. China has the biggest trade imbalance and is consistently using unfair business practices. China’s US trade surplus was $365.7 billion in 2015, more than five times higher than Japan’s surplus of $68.6 billion. The United States is critical of these surpluses because other countries are stealing US jobs.

China is currently in the midst of a crisis involving the risk of capital flight and a steep decline in the yuan’s value. Therefore, China is intervening in foreign exchange markets by selling the dollar for the purpose of artificially propping up the yuan. That means China can be viewed as a country doing the right thing because of actions aimed at making its currency stronger than is warranted by market conditions. Germany has a current account surplus of $285 billion that includes a US surplus of $74.2 billion, which is larger than Japan’s US current account surplus. Germany’s current account surplus is 8.5% of its GDP, the highest in the world and more than double Japan’s 3.3%. However, sanctions cannot be imposed on Germany because the country does not have its own currency. By using the euro, which is undervalued in relation to Germany’s competitive strengths, Germany has been constantly enjoying a virtually free lunch.

Although the United States is about to start using the newly established Monitoring List for foreign exchange rates, changes in these rates will make no contribution at all to correcting the current enormous imbalances. So why is the United States starting to use this program? The answer is probably that the Monitoring List is entirely the result of political actions rather than rational economic principles. This intensified evaluation system was created in order to obtain support for the Trans-Pacific Partnership. Free trade using the TPP will require monitoring unfair activities involving international trade and taking actions to stop these activities. The Monitoring List system was established as part of the Trade Facilitation and Trade Enforcement Act of 2015 in order to provide for these monitoring and control functions. The decision to include intensified evaluations in this act may be a reflection of the positions of people like Donald Trump and Bernie Sanders who tend to oppose free trade. This system may also be the result of lobbying activities at a time shortly before the 2016 presidential election by Ford and other companies and organizations that are critical of the yen’s depreciation.

Worries about one-sided US rules and beggar-thy-neighbor policies

The Monitoring List is contrary to the US Treasury Secretary Jack Lew’s goal of avoiding competitive currency devaluations. In fact, this intensified evaluation system can be interpreted as an attempt by the United States to reduce the dollar’s value in relation to the yen for competitive reasons. The United States has effectively restricted Japan’s ability to use foreign exchange market interventions. As a result, Japan is in an extremely difficult position with no defense against speculators. Limiting interventions to 2% of GDP restricts Japan’s foreign exchange market interventions to only about ¥10 trillion. Once speculators generate enough momentum, there may be no way to stop a rapid appreciation of the yen. If this happens, the negative cycle of a stronger yen and weaker stock prices may be reinforced in a self-fulfilling manner. In this case, stock prices would drop with no bottom in sight.

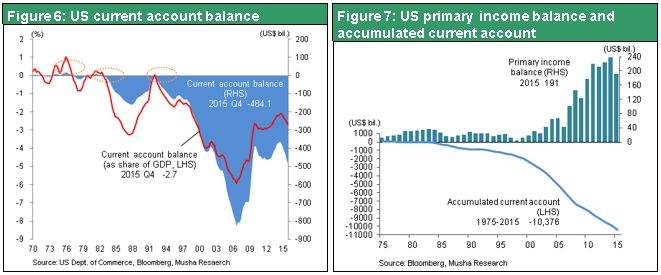

These US currency policies, arbitrary actions and rule changes (revisions to assumptions that had been tacitly accepted) are dangerous. When there is a bilateral imbalance, both countries share the responsibility. The United States has the world’s largest current account deficit, which was $484.1 billion (2.7% of GDP) in 2015.If trade imbalances are a problem, then the massive US trade deficit should be viewed as the root of the problem as well. This leads to the conclusion that the United States needs to eliminate the current account deficit by suppressing consumption in order to lower imports. A big drop in the dollar’s value would be the correct way to accomplish this goal. However, devaluating the dollar would obviously not be in the best interests of the United States.

The United States, which has the world’s largest trade deficit and debt, has probably greatly reinforced the foundation of the global economy by using a strong dollar to create an extensive business network covering the global economy and financial sector. A strong dollar gives the United States substantial external purchasing power and influence despite the country’s large volume of debt. Overlooking this benefit in order to criticize only the weaker currencies of creditor countries with trade surpluses is extremely unfair. Since the 1972 start of the dollar standard, the biggest beneficiary has been the United States, which has lived extravagantly while building up interest-free debt. So who made this possible? The obvious answer is creditor countries with trade surpluses. These countries have a bias toward weaker currencies in proportion to the size of their surpluses. On the other hand, the United States has a strong currency bias in proportion to its trade deficit and external debt. These biases were a natural occurrence under the dollar standard system. Global prosperity under this system was made possible by the supply of money worldwide resulting in the issuance of money by the United States, which had the world’s key currency, in the form of external debt.

Similarities with the global financial crisis – Failure to stop the rising yen and falling stock prices may lead to a global recession

There is a risk that constantly forcing the yen to play a sacrificial role may have detrimental effects in the United States and Europe. Japan is facing economic challenges caused by having the world’s only currency that is appreciating significantly along with deflation and increasing downward pressure on stock prices. Many people believe the Bank of Japan has become ineffective because nothing more can be done now that quantitative easing and negative interest rates have been implemented. In the past, the Bank of Japan’s actions had a very powerful positive effect on stock prices. But there was no reaction at all in the stock market to the long-awaited announcement of a negative interest rate on January 29. In fact, stocks declined and the yen appreciated after this announcement. The result was a flood of media reports about the ineffectiveness of Bank of Japan policies. Furthermore, the absence of additional easing by the Bank of Japan reinforced the view that the bank has become ineffective. Investors who had taken on risk in line with the Bank of Japan’s policies no longer had anything to stand on.

If we accept the view that quantitative easing and negative interest rates are ineffective, then we should be skeptical about the crisis response capabilities of the Fed and ECB. Both central banks have been consistently using these two measures. Doubting quantitative easing and negative interest rates also points to a global downturn in stock prices and a rapid increase in international financial instability. Speculators were successful for digging the global bear market that started with the financial crisis in China. Now these speculators are about to increase their destructive power by selling Japan. Investors should also be aware that the next target of speculators might be US stocks, which are now at an all-time high. The global financial crisis occurred because the destructive power of sellers grew as a cycle of plunging prices swept through the world’s financial markets. Market prices of stocks and corporate bonds dropped to levels far below their intrinsic values. The resulting loss of capital and negative cycle caused markets to collapse. Investors should not forget that there was a risk of an enormous market collapse if nothing had been done at that time to correct mispricing.

There are three scenarios for the yen and Japanese stocks. First is a big reversal of the yen’s strength and low stock prices, both of which have gone too far on their own momentum. The dollar will start to appreciate as interest rates rise due to the US economy’s consistent strength. Upturns of the dollar and stock prices in the United States will push Japanese stock prices up. Second is a switch to a weaker yen and higher stock prices because of large-scale actions by the Japanese government and Bank of Japan (a new direction for monetary easing that surprises financial markets, postponement of the next consumption tax hike, additional government spending, and foreign exchange market intervention). Third is a deepening global financial crisis. In this frightening scenario, a declining dollar caused by US economic weakness causes stock prices to fall worldwide. The crisis in China reemerges and a financial crisis even more severe than the one that began in August 2015 creates a global recession. The recent rapid appreciation of the yen and sharp drop in Japanese stock prices mean that the possibility of the frightening third scenario, which had been virtually zero, cannot be ignored. This is why investors must closely monitor the US and Chinese economies and watch for any changes in Japan’s policies.