Jun 27, 2016

Strategy Bulletin Vol.164

A key turning point – Will eliminating Brexit uncertainty cause stocks to rebound?

Containing the China crisis will be critical.

Will we see a powerful rally or the climax of the stock market’s extended downturn?

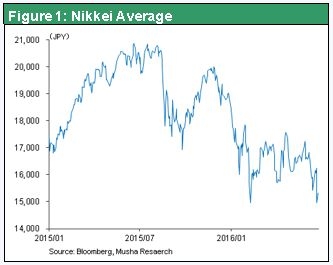

In a surprising outcome, the people of Britain decided to leave the EU. Does this mean an even more serious crisis is imminent? Or does Brexit signal the end of bad news for financial markets for the time being? Immediately after the announcement of the UK referendum result, the Nikkei Average plunged as the yen rapidly appreciated. The Nikkei closed at ¥14,952, which is precisely the same as the low point reached on February 11. I think the market is likely to move in one of two directions next. One is a powerful rally after establishing a W-shaped bottom. The other possibility is a climactic decline that ends the prolonged downturn that began in August 2015. If the first outlook is correct, then this is an excellent buying opportunity. But if the second outlook ends up being true, then this is a time for extreme caution by investors. China rather than Britain holds the key to determining which of these two scenarios will actually happen. As I explained in my previous report, the US economy is almost certain to remain healthy. As a result, the more global financial instability grows, the more China will have to be viewed as the primary cause.

The remarkable resilience of British stocks

The different reactions of the world’s stock markets to Brexit have been very interesting. On June 24, the first day of trading after the approval of Brexit, the FTSE 100 was down 3.1%, the smallest decline among stock markets of the world’s major countries. Moreover, the FTSE 100 bounced back an impressive 6% from its lowest point of the day. In the United States, the Dow Jones Industrial Average recorded the second-smallest drop with a 3.4% decline. This was followed by declines of 6.8% for the German DAX and 8.0% for the CAC 40 in France. Most significantly, there were very big drops in stock prices in southern Europe on June 24. The IBEX 35 in Spain fell 12.4%, the FTSEMIB in Italy was down 12.5% and the ASE in Greece plunged 13.4%. Furthermore, these southern European stock indexes all closed at about their lowest levels of the day.

Investors apparently believe that the EU will suffer the most damage from Brexit while the impact on Britain will be relatively small. Incidentally, in Asia, June 24 stock market downturns were 7.9% in Japan (Nikkei), 2.9% in Hong Kong (Hang Seng) and 1.3% in China (Shanghai Composite Index). The British pound dropped 8% in relation to the US dollar and 6% in relation to the euro. The weaker pound made the FTSE 100’s June 24 downturn even larger in terms of dollars and euros. Nevertheless, this index has performed surprisingly well so far in 2016 with a decline of only 2%.

No one knows the economic impact of Brexit – Less EU solidarity may boost the southern Europe risk premium

There is good reason to trust the market’s assessment of Brexit. First, Britain will remain in the EU for about two more years and no decisions have been made about a post-Brexit economic scheme. Consequently, there will be almost no effects on the British and EU economies for a while. On the other hand, there will be an immediate shift in perception of financial markets. Investors may have already started to worry about whether or not southern European countries will keep the euro now that the cohesiveness of the eurozone has been severely impacted. Anti-EU sentiment is growing in Italy and Spain. In Italy, a member of the Five Star Movement was elected mayor of Rome. In Spain, Podemos became the third most powerful political party at the end of 2015. But a departure from the EU by southern European countries would create even greater economic problems by pushing up interest rates.

Negative effects of Brexit are greater in the EU than in Britain

The second reason to trust the reaction of stock markets is the likelihood that Brexit will create more problems for the EU than for Britain. There are several key characteristics of the British economy.

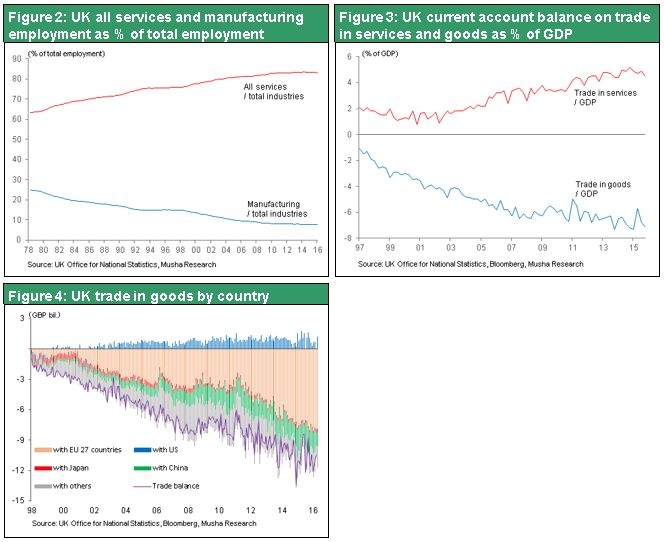

- No other country has an economy that has gone farther with the switch to services while downsizing the industrial sector. Britain accounts for less than 3% of the world’s merchandise exports but ranks second after the United States in service exports with a 7% share. Manufacturing is 8% of all jobs, the lowest among developed countries, and bank assets are 800% of the GDP, the highest in the world by far.

- No other country has an economy that is more open. Direct foreign investments in Britain are 70% of GDP, the highest in the world. This ratio is only 42% in Germany, 28% in the United States and 16% in Japan. Furthermore, foreigners own 54% of listed stocks in Britain, again the highest in the world.

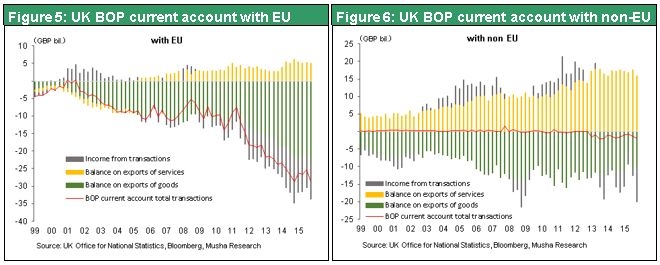

- Britain has an international payment balance structure in which service exports and huge direct investments from other countries cover the country’s massive trade deficit. Britain has a very large EU trade deficit. However, this deficit is offset by services provided to members of the Commonwealth of Nations (formerly the British Commonwealth) and income received from these countries.

To summarize, Britain is the EU’s second-largest export market after the United States and has an enormous EU trade deficit. But Britain is the European base for many Japanese and US companies and financial institutions. So Britain benefits by receiving income from EU investments. As a result, Britain and the EU are dependent on each other. Brexit and the accompanying weakness of the pound will significantly reduce Britain’s EU trade deficit. However, there will be a drop in EU-related investments in Britain. Moreover, Brexit will weaken Britain’s competitive edge as a center for international finance. So there are advantages and disadvantages for Britain.

A comparison of these advantages and disadvantages shows that the advantages are likely to be much greater. EU membership is not a major reason for the appeal of Britain concerning international finance and international service industries. Companies have been choosing Britain due to characteristics that have existed since well before the EU was created. Britain participates in the single passport system, which allows companies with a British financial business license to operate anywhere in the EU. Losing this right will have a negative impact to some extent. But there may be measures to reduce the effects of rapid changes. Britain has advantages in terms of information collection, the formation of networks and other aspects of business operations. That means Frankfurt or some other European city is unlikely to replace London as a center of international finance.

Britain’s competitive advantages as a global financial center are very well established

The United States and Britain lead the world in terms of all aspects of globalization: capitalism, a market economy, democracy, the English language, the rule of law and business protocols. In addition, these two countries are pillars of the world order and the nucleus of the world’s English-speaking countries. Furthermore, Britain and the United States play key roles in a diverse array of international relationships. Consequently, there will probably be no change in Britain’s advantageous position as a base for international finance and service industries after Brexit. After all, Switzerland has maintained sound business relationships with the EU without becoming a member.

Britain has not become opposed to globalization

Britain has a well-established reputation as a country with an economy that is open to the world. As a result, Brexit is unlikely to make Britain a closed and xenophobic country, which is what some people fear may happen. In fact, Brexit will probably lead to stronger ties between Britain and countries and regions outside the EU. So the result is almost certain to be more progress with globalization, but in different direction. In the coming years, the EU will not be a significant source of global economic growth. Instead, the United States, India, the ASEAN region, African countries and other countries outside the EU will fuel economic growth. Britain now has the option of enlarging its international network beyond the core of the Commonwealth of Nations, a vestige of the British Empire. This network can be extended to cover countries and regions making big contributions to the global economy. If this happens, the EU will be unable to turn its back to a post-Brexit Britain. Furthermore, southern European countries like Italy, Spain and Greece are unlikely to abandon a strong and reliable currency (the euro) and its low interest rates by leaving the EU (regardless of how much the influence of populism increases in these countries). This is clearly evident from the shift in the stance of the administration of Greek Prime Minister Alexis Tsipras concerning that country’s debt crisis. Obviously, there is no basis to embrace extreme interpretations of Brexit as the beginning of the end of European unity or the failure and demise of globalization.

For these reasons, investors should expect market volatility sparked by Brexit to end after a relatively short time.

The urgent need to end the crisis in China

Despite this outlook, it will not be easy for financial markets to switch to a risk-taking environment. The reason is uncertainty about China, which is an issue far more important than Brexit. Additionally, it is impossible to predict how the crisis in China will end.

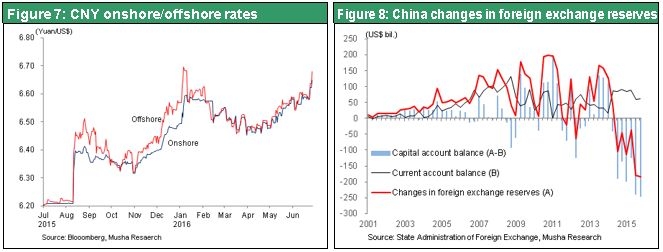

We are currently at the stage where financial markets are starting to factor in the effects of the crisis in China. There are three reasons to expect this crisis to become even worse. First, is the end of volume-based economic growth (railroad cargo, crude steel output, electricity generation, exports and imports, and other indicators). Second, the deteriorating situation involving foreign currency, which is China’s Achilles’ heel, could result in a weaker yuan triggering a financial crisis within China. Third, conflict concerning the different goals of President Xi Jinping and Premier Li Keqiang is casting doubt on ability of the Chinese government to rule the country.

There may be a decline in the absolute authority of the Chinese government, which is vital to having confidence in China itself. A loss of confidence would mean that investors could no longer remain defenseless with respect to the yuan and holdings of Chinese assets with risk exposure. At this point, there is no doubt that China has a serious crisis. In this environment, people who avoid risk have the advantage concerning all types of investment activity.

During the past six months, Japan has been the world’s only loser in terms of stock market performance. The cause is clearly the yen’s abnormal strength. Japan’s position as the only stock market loser is closely linked to the strong yen. So exactly why has the yen appreciated to this level? I suspect that the US Treasury Department offered to allow the yen to appreciate as a sacrifice in return for avoiding a devaluation of the yuan. The result was the yen’s abrupt upturn, which caused Japanese stocks alone in the world to fall. (See Strategy Bulletin Vol. 160 (May 4) http://www.musha.co.jp/attachment/57294495-1668-498d-803f-30ba85f2cfe7/bulletin_e_20160504.pdfand Vo. 162 (June 7) http://www.musha.co.jp/attachment/57561779-8aec-405b-84b8-2bc285f2cfe7/bulletin_e_20160607.pdf for more information about this subject.)

Another global financial crisis is not about to begin

Investors should focus on two scenarios for upcoming events. In the first scenario, although China’s crisis could become even worse, there is also a possibility of an upward correction in stock prices from the current excessive pessimism if the crisis is brought under control. In this case, prospects for another global financial crisis are small for three reasons. First, there was too much optimism when the financial crisis started in 2008 but no signs of excessive optimism today. This limits the magnitude of an asset bubble. Second, countries are pursuing friendly financial policies. Third, companies are reporting consistently high earnings. In terms of timing, there may be a worldwide relief rally prior to the September G20 Summit in Hangzhou. If this rally happens, investors should view the Nikkei Average’s low on June 24 as the second part of a double-bottom pattern. In the second scenario, China’s crisis continues to deepen. This scenario could be triggered by declines in the yuan’s value and China’s foreign exchange reserves, so investors should watch these two numbers closely.