Jul 19, 2016

Strategy Bulletin Vol.165

The Mystery of Record-high US Stock Prices amid Historically Low Interest Rates

The US can avoid the liquidity trap that has snared Japan and Europe

As the unprecedented worldwide decline of long-term interest rates continues, people are becoming worried due to the emergence of a situation they have never experienced. Since the summer of 2015, interest rates and stock prices have been moving down in tandem. This gave pessimists a reason to expect another crisis on the same magnitude as the global financial crisis. However, the rise of US stock prices to a new all-time high adds another dimension to the current situation. What is the significance of the US stock market rally? Musha Research believes that this rally has made it even more likely that the standpoint of pessimists will be completely rejected.

(1) US Stocks Set a New Record as Interest Rates Fall Worldwide

The reasoning of pessimists is centered on declining long-term interest rates

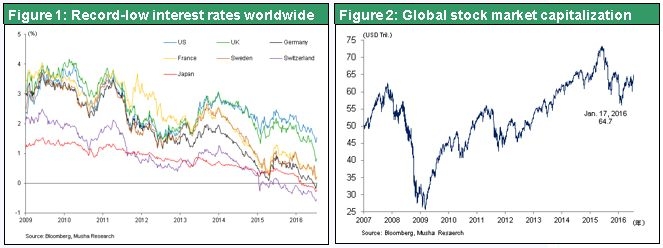

As you can see in Table 1, long-term interest rates around the world continue to fall to new record lows. Following the recent drop in British pound interest rates, the United States alone among developed countries has a decent interest rate. The majority of market participants think low interest rates are a sign of trouble in the future. There were persuasive arguments for all four reasons supporting the position of pessimists. First, weak demand for capital makes people pessimistic and therefore unwilling to take on risk. Second, excessive monetary easing by central banks is a mistake because it creates too much money. The result is more downward pressure on interest rates. Third, the global improvement in productivity is slowing down. Fourth, there is a resonance between financial system concerns and falling stock prices.

Now we can see the contradictions of pessimists’ reasoning

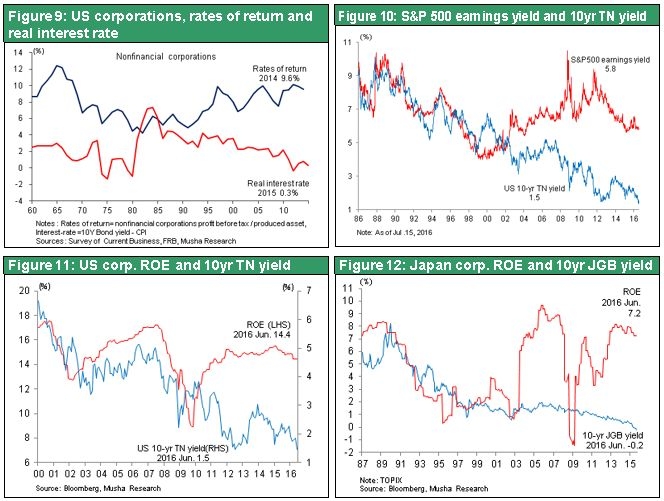

Despite these four reasons, record-high US stock prices have clearly ended financial system concerns and falling stock prices worldwide. The scenario for a global crisis, which appeared to be very convincing, has been rejected. Pessimists who used to be extremely confident about their beliefs have suddenly reached a dead end. Moreover, companies have been reporting strong earnings and the outlook is positive. US companies are giving shareholders a 5% return, the sum of a 2% dividend yield and 3% from buying back stock. That is more than three times higher than the long-term interest rate of 1.5%. Today’s high stock prices can be justified from the standpoint of both valuation and economic rationality.

Furthermore, life styles are on the verge of dramatic changes because of the enormous revolution taking place in the technology sector. In the United States, there is a strong recovery in the number of jobs and inflationary pressure is growing. The beliefs of pessimists cannot explain this upturn in jobs and inflation.

A closer look at the four reasons for pessimism reveals that most of the pessimists’ positions were dubious from the outset. The first reason, which is weak demand for capital, is linked to the rapid pace of the current industrial revolution. Prices of equipment, systems and services have been falling rapidly because of this revolution. Consequently, we should view the smaller demand for capital as a result of the improvement in capital productivity. The second reason, which is falling long-term interest rates caused by excessive central bank monetary easing, is a one-dimensional view. Without this excessive easing, the global economy would have been even weaker, causing prices of assets to fall. Having nowhere else to go, capital would flow into government bonds, creating more downward pressure on interest rates. The third reason, slowing growth in productivity, is the most reasonable position of pessimists. However, as I explain in the following section, there is reason to be suspicious about data indicating that productivity growth is slowing. The fourth reason, which is financial system concerns along with falling stock prices, has been rejected. Overall, the fundamental errors of pessimists’ thinking are now being exposed.

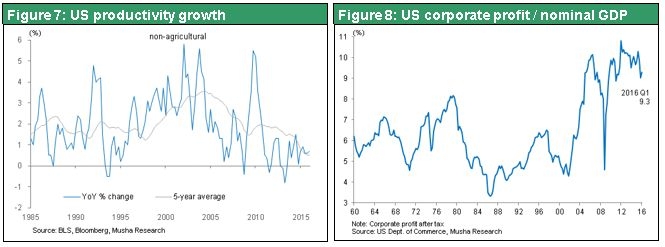

Don’t trust statistics that show productivity growth is slowing

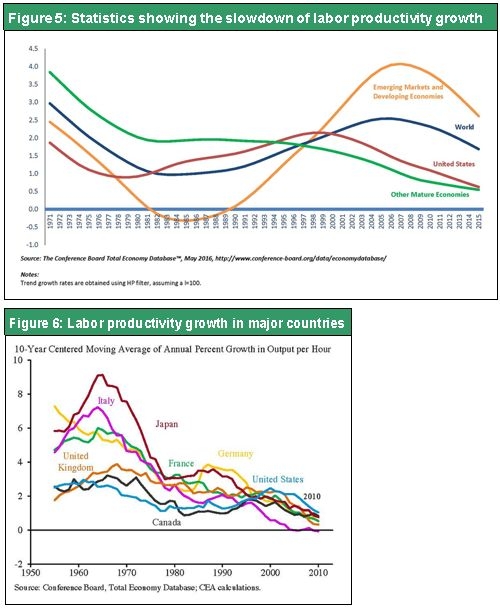

Looking at statistics alone, it is impossible to deny the fact that the pace of productivity improvements has been declining in recent years. Table 5 shows productivity improvements in a number of countries based on figures compiled by The Conference Board. Since the start of the global financial crisis in 2008, productivity advances have been slowing worldwide. The slowdown in productivity growth was particularly significant in the United States (Table 6).

This raises the question of why earnings at companies are so strong even though productivity is increasing more slowly. As you can see in Table 8, US companies are reporting the highest earnings ever in absolute terms and as a percentage of GDP. The existence of surplus capital and labor means that companies do not need as much of these two resources as in the past. In addition, if in fact the productivity growth rate is declining, then we must conclude that production volume is falling significantly. But although lower production should have a big negative impact on earnings, we are seeing earnings continue to climb. What is the explanation for this contradiction? There is no reason for the simultaneous occurrence of (a) surplus capital and labor, (b) strong earnings and (c) slower growth in productivity. Obviously a mistake exists somewhere. But surplus capital and labor and strong earnings are both undeniable facts. Consequently, the only explanation for the contradiction is that statistics showing weaker productivity are not an accurate representation of actual productivity.

Until now, pessimists have tried to explain this contradiction by assuming that earnings at companies will start declining at some point. However, companies have been reporting consistently strong earnings for the past decade, even during the darkest days of the global financial crisis. This raises serious doubts about the pessimists’ belief that productivity is decreasing.

This can be called the productivity paradox. A clear gap exists between the actual state of the economy and statistics showing that productivity growth is slowing. On March 28, 2016, the Bank of Japan released a research paper titled The Slowing Labor Productivity Growth Rate in Developed Countries with analysis of this issue. This paper identified three causes for slower productivity improvements: (a) the misallocation of capital, (b) the mismatching of labor, and (c) measurement problems. But the Bank of Japan refrained from making any conclusions. However, the first two causes are not persuasive because they are merely different ways of saying almost the same thing. In other words, if we believe that a surplus of capital and labor exists even though productivity is falling, then it goes without saying that the cause is the misallocation of resources.

The position of people who believe productivity statistics are wrong

The time has come to make it clear that statistics are wrong. More than a few economists have adopted this stance. In a Nikkei Shimbun article on September 7, 2015, Martin Feldstein, a professor at Harvard, noted that US GDP per capita increased at an annual rate of 2.2% between 1891 and 1972 and then slowed to a growth rate of 1.5%, according to official statistics. But he believes that the actual growth rate is more than 3%. Mr. Feldman says the reason is that economic statistics overlook the majority of improvements in living standards that are derived from new products and services. Examples range from air conditioning and drugs to fight cancer to new forms of entertainment and services like Google and Facebook.

In their book The Second Machine Age, Erik Brynjolfsson and Andrew McAfee, both of MIT, say that the first age of machines replaced physical labor while the second age is replacing mental work with computers. They believe that Moore’s Law (computing power doubles about every two years) is still viable and that the productivity growth rate is not declining. Their position is that the productivity gains are being underestimated mainly for the following reasons. First is an underestimation of the productivity of computing power because the price of MPUs is no longer decreasing. Second is the failure to include new services. Third is the consumer surplus, which is the value obtained by consumers from goods and services in excess of their market prices. Fourth is the underestimation of benefits of investments in intangible assets. This stance is consistent with the view of Amazon founder Jeff Bezos that “we are near a golden age of artificial intelligence.”

(2) Our View – Unprecedented Excess Earnings Produced Surplus Capital and Finding Ways to Use this Capital Will Be Critical

Why profit margins and interest rates are moving in opposite directions

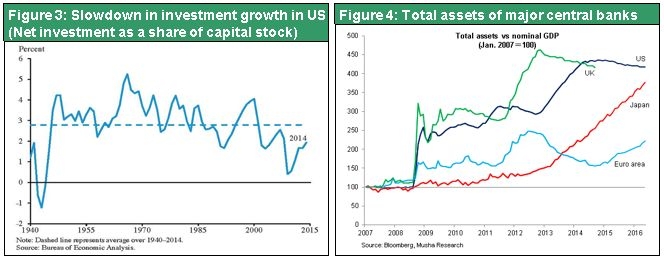

Normally, strong earnings and historically low interest rates should not occur at the same time. The fundamental cause is most likely the ability of companies to generate substantial excess earnings from higher productivity resulting from the new industrial revolution. However, companies are unable to invest the money they accumulate from these strong earnings. As a result, capital sits idle and interest rates fall. This is why the big downturn in developed country interest rates demonstrates the existence of surplus capital. Furthermore, the lack of growth in jobs (rising unemployment, low labor participation rate, sluggish wage growth) demonstrates the existence of surplus labor. Why have surplus capital and labor increased to the point where they are problems? The cause is probably the remarkable improvement in capital and labor productivity at companies. The new industrial revolution, driven by IT, smartphones, cloud computing and other advances, has converged with globalization to produce a remarkable upturn in productivity. Companies require much less capital and labor as a result. Higher productivity has immediately sparked a big increase in earnings while simultaneously producing capital and labor market slack. In the United States, Japan and Europe, companies for the first time in many years no longer need to make reinvestments equal to depreciation. Due to smaller capital expenditures, Apple, Google and many other prominent companies are constantly holding massive amounts of excess capital.

The critical need for policies that can put surplus capital to work

If the idle money that companies are hoarding due to their high earnings is in fact exerting downward pressure on long-term interest rates, something must be done to end this problem. First, this accumulation of money is creating more social instability by widening the gap between rich and poor. This is because of the relative decline in the income of workers while the higher allocation of capital for the benefit of shareholders gives large investors the advantage. Hoarding money also creates the problems of a larger income gap caused by differences in workers’ skills and knowledge and of a larger gap between rich and poor caused by the international division of labor. Second, there is the more fundamental problem concerning whether or not the accumulation of unused capital signifies the death of capitalism. If governments do not have the resolve to enact policies aimed at altering the current situation, capitalism could collapse.

The scenario leading to catastrophe – No policies and fiscal and monetary tightening

There are two possible outcomes. The first is that countries enact no policies at all or implement fiscal and monetary tightening that would encourage companies to hoard idle capital. Going down this path would cause the economy to collapse and stock prices to plummet. Companies today are not reinvesting or returning in other ways to the real economy their substantial profits. This is like an evil merchant who simply buries his earnings, resulting in a drop in the amount of circulating money, which restricts economic activity. In fact, this business practice was frequently criticized during the Edo Period. According to Marx, the essence of capitalism is the conversion of capital into other forms in order to create an unlimited chain for generating more value. Hoarding capital violates this principle, too.

In a sound economy, money capital, which is the initial form of capital, should be converted into materials, labor, machinery and other forms of commodity capital. The result should be growth in money capital. But today, there is no conversion at all because money capital is simply creating more money capital. Capital is used in a manner that produces no growth in value. Most companies believe that “cash is king.” Even though companies are extremely profitable, actions are needed to end the current environment in which capitalism is not functioning. Otherwise, the world would probably enter a prolonged period of economic stagnation that has a catastrophic ending.

The scenario leading to a better future – Three policy initiatives for creating demand

In the second possible outcome, governments enact policies aimed at bringing profit margins and interest rates in line with each other. In this scenario, the recycling of surplus capital back to the real economy would speed up economic growth, which would in turn push up interest rates. Accomplishing this would lead to a brighter future. There are three basic options for policies that encourage the recycling of capital: monetary policy, fiscal policy, and income/social policy.

1) Monetary policy = Boost stock prices so that profit margins (earnings yields) based on market value decline; stock repurchases are an effective way to do this.

2) Fiscal policy = Keynesian measures and revisions to institutions (such as private finance initiatives and issuing revenue bonds) for stimulating private-sector investments

3) Income (social) policy = Wage hikes and a higher allocation of income to labor to increase consumer spending and basic income and other social policies for increasing personal income

Enacting these policy initiatives would raise the economic growth rate by enabling benefits of the technology industrial revolution to contribute to economic growth and a better standard of living. In the United States, where the spirit of individualism reigns supreme, the preferred order of priority is monetary policy, then fiscal policy and finally income/social policy. Income and social policies, which are a resource allocation method that does not use the market mechanism, are not popular in the United States. In Europe, on the other hand, countries probably prefer to use income and social policies first. Japan is somewhere between the United States and Europe. The emergence of signs that the optimistic second scenario is starting to take place may explain why U.S. stock prices are now at an all-time high.

(3) The United States Can Avoid the Liquidity Trap That Happened in Japan and Europe

The U.S. shows the world how to succeed

The United States is the only developed country with a decent long-term interest rate, a positive bank net interest margin and consistent annual credit growth of about 5%. In other words, the United States has not become mired in a liquidity trap. This is why the world is closely watching the United States, which will probably succeed at avoiding this trap. Japan and Europe can then learn lessons from US policies in order to extricate themselves from their own liquidity traps.

The outlook for the US economy is bright: Growth is expected to continue for several more years. There are four sound drivers of this growth: (1) a positive cycle originating with consumer spending for services; (2) much upside potential for the housing market; (3) preparations for the start of substantial public-sector demand; and (4) robust growth in credit.

However, the risk of inflation is increasing because the United States is in the second half of this economic cycle. As the number of jobs grows and the supply of labor becomes tighter, there is more upward pressure on wages. This is raising labor’s share of income and the growth rate of the consumer price index. At this point, the United States has largely accomplished its quantitative easing goals of full employment and inflation of 2%. Japan and Europe are still working on reaching these goals.

Policy initiatives and market efficiency saved the United States from the liquidity trap

Why was the United States alone among developed countries able to avoid the liquidity trap? There are two main reasons. First is the quick and accurate selection of actions by former Fed chairman Ben Bernanke. Second is the efficiency and flexibility of US labor and capital markets. Policy initiatives and market efficiency are characteristics where the United States is well ahead of all other countries. Figure 16 shows the relationship between changes in the unemployment rate and GDP for a number of countries. The United States is the steepest, which means there is considerable flexibility, while Japan ranks last. Furthermore, in US capital markets, the allocation of capital is proper due to arbitrage investments that take advantage of falling interest rates.

Growth of corporate loans and consumer loans are behind the growth of US debt. Both of these loans contribute to economically rational financial activity. Funding for stock repurchases accounts for half of the growth in loans at companies, which are increasing at a 7% annual rate. Obviously, companies are improving their financial efficiency by using today’s low interest rates to replace equity with debt. In addition, the recovery in the job market is making households better able to take on risk. This explains why the US consumer loan growth rate has returned to about 7% (home loan growth is only at the 1% level).

Nevertheless, there is still a risk of the United States falling into the liquidity trap. This could happen if US long-term interest rates are overwhelmed by the global downturn in interest rates. As the global economy declines while the US economy alone remains healthy, the dollar would appreciate and surplus funds from around the world would flow into the United States. This would create an environment in which dollar cash is king, resulting in enormous demand to hold dollars in the form of cash. These events could occur because of the undeniable superiority of the US economy’s performance. If US long-term interest rates plunge as they have in Japan and Europe, the interest rate spread would disappear and financial markets would no longer be able to function. In this environment, the government would have to implement policies for correcting this unprecedented long-term interest rate downturn. And Keynesian policies would be vital to achieving this correction.

Trump or Clinton will lead us to a new age of Keynes

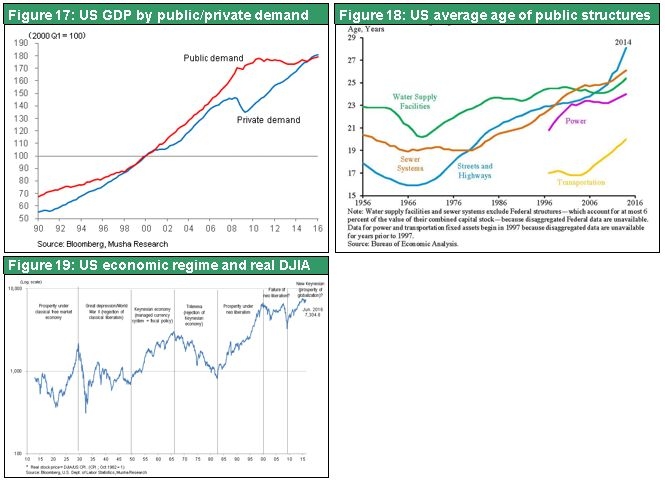

If in fact interest rates have dropped to historic lows because of a large volume of capital, then the US government will probably enact Keynesian policies. What should this spending target? Both presidential candidates, Donald Trump and Hillary Clinton, plan on making large expenditures for infrastructure, defense, new technologies and, perhaps, protecting the environment. The US infrastructure is aging. Now that the deficit has fallen from 10% of GDP (2010) to the 2% level (2015) and long-term interest rates are at an unprecedented low, this is an excellent opportunity for infrastructure expenditures. The US economy is in good health. The country has ample capital but is looking for ways to use these funds. There is no reason not to expect that people will come up with ways to transform this unprecedented situation into a positive outcome.

Figure 19 shows changes in the US economic regime and real stock prices. Over the years, the United States has gone from (1) prosperity fueled by a classic free economy and its subsequent demise to (2) prosperity fueled by a Keynesian economy and its subsequent demise and (3) prosperity fueled by a new free economy and its subsequent demise. Today, the United States appears to be on the verge of advancing to an age of New Keynesianism. Donald Trump’s abandonment of the traditional Republican economic stance of a smaller government is a key sign of this impending shift to a new age.

(4) Implications for the Japanese Stock Market

There is a more urgent need for policy initiatives in Japan than the U. S. – (1), (2) and (3) are all necessary

Policies that take full advantage of low interest rates must be implemented. This is true in Japan even more than in the United States. Countries need to create an environment in which governments, companies and individuals all borrow more money and receive more benefits by borrowing. But many people disagree. The reason is that these measures are viewed as being contrary to common sense and public order. Consequently, there is a need for economic reasoning that can eliminate this ideological opposition. Enacting policies to create this environment will probably spark a powerful stock market rally in Japan. The Nikkei Average may rise to ¥30,000 or even ¥40,000. Moreover, high stock prices would be easily justified by the high level of corporate earnings in relation to low interest rates.

Prime Minister Abe calls Japan’s current economic initiatives “investments in the future.” Expenditures are not limited to public-works projects with dubious benefits, such as the new magnetic levitation train line. Japan is also reexamining a variety of institutions with the aim of creating a virtuous cycle that improves life styles and encourages innovative thinking. Government spending that contributes to achieving these goals will receive priority. The Bank of Japan will provide financial support. As a result, there is reason to expect benefits from these Japanese-style initiatives.

The beginning of a summer rally for Japanese stocks

A number of significant events are shaping the current economic environment. Among them are record-high US stock prices, the prevention of a global financial crisis, US economic growth and the end of the decline in US long-term interest rates, US interest rate hikes, and a rewind of Abenomics. This environment is increasing prospects for an upturn in Japan’s stock markets in the second half of 2016.

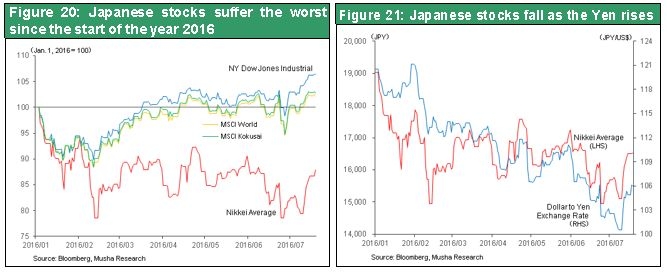

Among the world’s major stock markets, Japan was the only loser thus far in 2016. During the past few months, Musha Research has stated that there are three probably scenarios for what will happen next.

Scenario 1 – Japan remains the world’s only loser. The probability of this scenario is zero because there are no signs at all that the Japanese economy will be the world’s only loser.

Scenario 2 – A rapid catch-up stock market rally. There is a 70% probability because the yen is very likely to reverse direction after being the world’s only appreciating currency while Japanese stocks were the only losers in the world. A weaker yen will require a healthy US economy and a respite from economic and financial problems in China. From a short-term perspective, both of these conditions will probably be fulfilled.

Scenario 3 – A steep drop in stock prices worldwide – There is a 30% probability. This would happen if stocks in other countries follow Japanese stocks downward and a financial crisis occurs in China. But these events are very unlikely to happen in the near future.

For the time being, the third scenario calling for a global stock market plunge will not happen. Consequently, there is a possibility of an unexpectedly strong rally. In terms of timing, there may be a global relief rally prior to the September G20 Summit in Hangzhou. However, investors should closely follow any changes in the yuan’s value and in China’s foreign exchange reserves because these movements are widely viewed as potential triggers for a global financial crisis.