Oct 03, 2017

Strategy Bulletin Vol.187

The global economic boom and outlook for a big Abe win point to a powerful stock market rally

(1) The North Korea crisis may deepen after Trump’s November trip to Asia

Many events are influencing stock prices today. North Korea, Japan’s general election, Trump’s tax cut plan, and the Fed’s interest rate hikes and balance sheet downsizing are some of the major developments. But almost all of these events appear to be pushing stock prices up. The possibility of a military conflict with North Korea is the only reason for concern that is impossible to predict. However, North Korea is unlikely to attack first because that would be suicidal. Only a US first strike is possible. But this could probably happen only after President Trump completes preparations for an attack with his November trip to Asian countries. Prime Minister Abe’s abrupt decision to dissolve Parliament’s lower house on September 28 appears to be aimed at unifying Japan prior to the outbreak of hostilities in North Korea. If these views are valid, then the Korean crisis should remain calm for the next month or so.

(2) The worldwide economic upturn is reaching its climax

All developments other than the North Korea crisis are fueling a big upturn in stock prices. Figures in the Bank of Japan Tankan that was released on October 2 as well as the US manufacturing ISM index provided more evidence that the world is in the midst of an unprecedented economic boom.

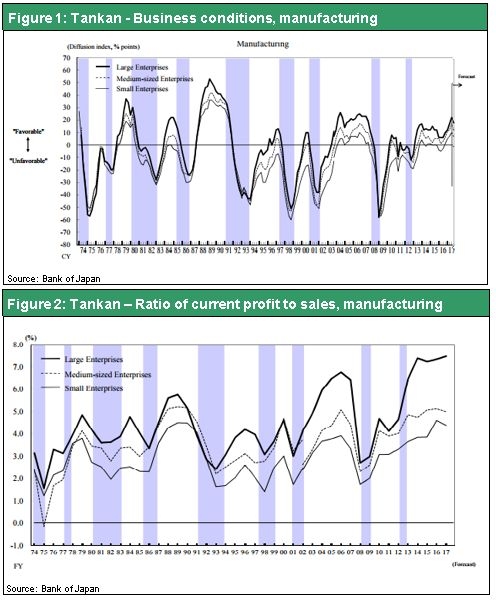

Business sentiment and earnings in Japan are the strongest since the asset bubble

According to the Tankan, business sentiment among large manufacturers in Japan is now the highest since the global financial crisis. Sentiment is particularly strong in the chemical, electrical machinery, production machinery and business machinery sectors, all of which are linked to global capital expenditures. Earnings and jobs are even stronger than business sentiment. Ordinary income at Japan’s large manufacturers was up 33.1% from one year earlier in the second half of 2016 and posted another big increase of 23.1% (a 13.8% upward revision of the original forecast) in the first half of 2017. This level of earnings is unprecedented.

The earnings forecast for the second half of 2017 calls for an 8.9% decline, a cautious outlook that assumes a dollar/yen exchange rate of ¥109.12. But this prediction will almost certainly be raised significantly. Furthermore, Japanese companies are planning on an ordinary income margin of 7.47% in fiscal 2017. This is well above the 6.76% margin in fiscal 2006 shortly before the collapse of Lehman Brothers and the 5.75% margin in 1989 at the peak of the asset bubble. High margins demonstrate that Japanese companies have shifted emphasis to adding value and earning large profit margins. Years ago, Japanese companies lost the price competition war to companies in other Asian countries. But now companies in Japan have used outstanding technologies and quality to establish an overwhelming lead in market sectors where competition is not based on prices. Growth in China’s imports of Japanese goods is one indication. In 2016, China’s imports from Japan were up 1.6% while imports from Korea decreased 8.9% and imports from Taiwan decreased 2.8%. During the first eight months of 2017, China’s imports from Japan were up 14.3% compared with increases of 9.5% for Korea and 10.2% for Taiwan. These figures are most likely indications that Japan is becoming increasingly competitive involving the supply of intermediate goods.

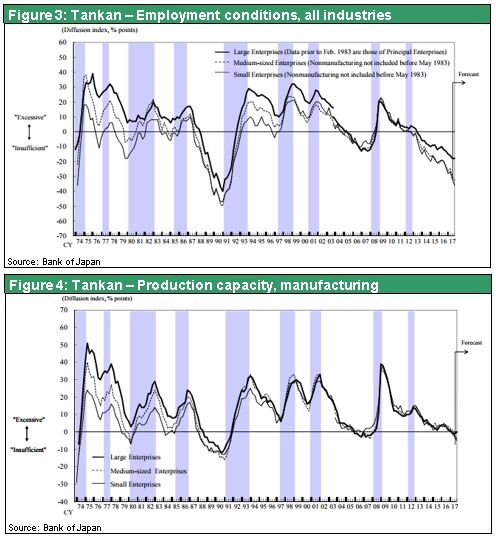

Japan’s vibrant economy and strong earnings are making the labor shortage even worse. Small to middle-market companies are having even more difficulty recruiting people than large companies are. Economic strength has also eliminated Japan’s surplus of production capacity. In fact, shortages are emerging. This situation should obviously produce a big increase in capital expenditures. Planned capital expenditures (excluding land but including software and R&D) in fiscal 2017 are up 7.5% at large companies compared with a 0.7% increase in fiscal 2016. The growth rates are 14.0% for middle-market companies compared with 8.8% in fiscal 2016 and 4.7% at small companies compared with a 7.4% decrease in fiscal 2016.

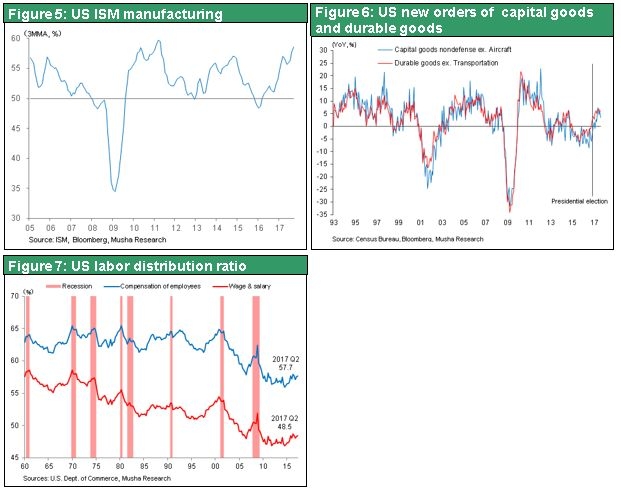

Japan’s economic growth is gaining momentum as growth in production, jobs and earnings is finally starting to yield higher investments. The economic boom is even stronger in the United States. The manufacturing ISM index surged to 60.8 in September. Most noteworthy was the rise in the new orders index to 64.6, the highest level since the global financial crisis. In both Japan and the United States, the driving force for economic growth, particularly for increasing orders for durable goods and capital goods, is shifting to rising capital expenditures linked to a labor shortage. Apparently the global economy is about to finally reach the stage of full-throttle growth. If so, then there should be no doubt that inflationary pressure is quietly but steadily climbing. The start of an upturn in labor’s share of income in the United States, which had dropped to an all-time low during the past year, is a clear indication of this inflationary pressure. As a result, investors should expect the Fed to continue raising interest rates regardless of who becomes the next chairman. However, long-term rates will probably rise faster as the Fed downsizes its balance sheet.

(3) The Trump administration has announced its tax cut plan

Progress regarding tax cuts and tax reform is more good news for the stock market. At one point, most people had given up hope for any action. If the proposed cut in the corporate federal income tax rate from 35% to 20% is enacted, earnings per share at US companies will rise by a minimum of about 10% and the PER will drop from the current 18 to 16. Furthermore, if the repatriation tax cut is enacted, a massive volume of overseas retained earnings will be moved to the United States where it could fund enormous stock buybacks. President Trump is also proposing a reduction in the individual income tax along with a big increase in the standard deduction from $12,700 to $24,000. If this happens, consumer spending would probably increase.

But some are critical because they view the proposal as nothing more than a spending policy with no source of funding. And there are doubts about whether or not the Democratic Party will support these changes. Because a reduction in the individual income tax will benefit wealthy people. The Financial Times also stated its concerns about the Trump tax proposals on October 2 in an article titled “Trickle down myths, Trump tax cut will help investors not workers.” No one can deny that these tax reforms will directly benefit companies and investors. Determining if these reforms will also subsequently produce benefits involving jobs and consumers (I believe they will) is definitely a problem. But for the time being, there is no doubt that these proposed tax cuts and reforms will significantly boost stock prices and the dollar.

The dollar appreciated significantly late in 2016 in response to expectations about more government spending and monetary tightening under Trumponomics. But the dollar then quickly weakened because of disappointment concerning President Trump’s policies. Now that the Trump administration has renewed these expectations by announcing a policy mix of more spending accompanied by monetary tightening, investors have reason to expect the dollar to start appreciating again.

(4) Japan’s election is likely to be an LDP landslide

The biggest positive surprise of all for Japanese stocks will probably be a big victory for the Liberal Democratic Party (LDP) in the October 22 lower house election. This would greatly enhance the unity of the Abe administration. Public support for Prime Minister Abe has plunged because of problems involving Moritomo Gakuen and Kake Gakuen. Many people have criticized this snap election because it was not called for any major issue. Moreover, immediately after the election was announced, Tokyo Governor Yuriko Koike revealed plans to create a political party called the Party of Hope as a center of opposition parties with the goal of becoming the ruling party. Soon after the Party of Hope was launched, Democratic Party President Seiji Maehara in effect disbanded the party and moved its parliament members to the Party of Hope. The Democratic Party parliament members approved this step and the party then ended all activities.

Former Democratic Party parliament members who want to become Party of Hope candidates must promise to support the National Security Act and the associated amendment to Japan’s constitution. All others will be excluded from the new Party of Hope. DP parliament members who do not make this promise are likely to join the new Constitutional Democratic Party of Japan that Democratic Party leader Yukio Edano has said he will form. What is the outcome of this completely unexpected situation likely to be?

The most probably outcome of the election will be a victory for Prime Minister Abe and the LDP that will heighten the solidarity of the Abe administration.

1) A unified fight by opposition parties is impossible – A change of political control will be impossible unless the opposition parties unite behind a single slate of candidates. But a number of events have made this type of unity impossible. An alliance combining the conservative Party of Hope and Japan Restoration Party with the left-leaning parties (Edano’s Constitutional Democratic Party, Social Democratic Party and Communist Party) is inconceivable.

2) The Party of Hope and Governor Koike will reveal their true intentions – Many people expect Governor Koike and her new party to be very successful. But the popularity of the governor and her party will probably drop quickly. Over the weekend, there were negative media reports about Governor Koike and events following the formation of the new party. Even the Asahi Shimbun, which had consistently been a supporter of a new ruling party in Japan, ran a three-day series of articles analyzing Governor Koike. The articles were titled (1) Koike-style itinerant transmigration and personal connections with the powers that are creating speculation, (2) The gap between support for diversity and actual policies, and (3) More emphasis on her own decisions rather than consensus, no explanation of the process. All three articles discussed Governor Koike’s accomplishments and her highly distinctive approach to politics and the associated problems. LDP parliament member Shinjiro Koizumi made the following remark about the governor: “Governor Koike is irresponsible whether she steps down as governor of Tokyo or remains governor in order to avoid the responsibility of being the Party of Hope leader and a candidate for prime minister to oppose Prime Minister Abe.” This statement targets the serious dilemma that the governor is facing. The Party of Hope boom is very likely to fade away and the party will probably fail to capture as many parliament seats as expected. If this happens, the Party of Hope will simply become a supplementary element of the LDP. This was the gate of the Japan Restoration Party. The result would probably be even greater political stability.

3) The decline of liberals will be in full view – The Democratic Party has effectively been forced to disband. The reason is that it is no longer possible to deny that the postwar liberal policies backed by the Democratic Party of Japan and subsequent Democratic Party were a failure. The liberals said that the former Communist countries were peace-loving governments, private-sector companies were evil, and governments should distribute generous benefits to people in need. But voters have abandoned this thinking. This mindset is still embraced only by a few media companies and people in the academic community. Liberals who are left out of the Party of Hope will be unable to win a meaningful number of seats in the next parliament.

For the reasons I have just explained, I believe that prices of Japanese stocks will increase dramatically as the end of 2017 approaches.