May 21, 2018

Strategy Bulletin Vol.199

Extreme optimism is correct

Speech Transcript – The Eighth Great East Japan Earthquake Recovery Support Seminar (May 12)

Main points

- Extreme optimism is necessary. People will live 100 years and the Nikkei Average will climb to ¥100,000. Now is an excellent time to buy stocks from both very short and long-term perspectives.

- The decisive factor regarding the investment climate is how to view President Trump. The president is demonstrating very strong leadership concerning the economy and geopolitics. I believe this is a positive factor.

- An industrial revolution and technology innovation on an unprecedented scale are taking place. If countries implement the correct policies (monetary easing and more public-sector spending to create demand), a powerful stock market rally is likely to continue.

- The outlook for a ¥100,000 Nikkei Average is based on Japan’s increasingly advantageous position in the world because of its economy and especially the international division of labor and geopolitics.

- China will continue to use stopgap measures, but the country will eventually encounter severe economic problems. No near-term problems are likely. In Europe, the economy remains lethargic.

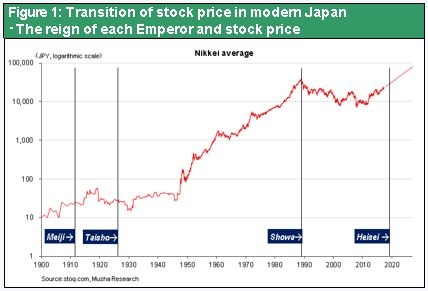

(1) A 100-year life span and Nikkei Average of ¥100,000

100 years – Making the last stage of life the best; the critical importance of building up savings

Many people expect a lifespan of 100 years to become relatively common. In Malaysia, Mahathir Mohamad became the prime minister on May 9 at the age of 92. Most of the people here today can still look forward to the best years of your lives. In the past when people lived 60 to 80 years, there were three stages of our lives: learning, earning and enjoying our final years. But now this concept of starting the final phase of life at age 60 is out of date. We are entering an era in which age 60 marks the beginning of the peak years of our lives. As a result, accumulating a sufficient amount of assets is very important. Without enough savings, it will be impossible to make a meaningful contribution to society and enjoy a fulfilling life. What should we do? Although I am using this point for my own purposes, the answer is to buy stocks.

The high probability of a ¥100,000 Nikkei Average in 2031

Now is an excellent time to buy stocks. All investors need to do is buy stocks and then do nothing. They can expect to see a ¥1 million investment quadruple to ¥4 million over the next 15 years. Between 1950 and 1990, the Nikkei Average increased by almost 400 times. The Nikkei Average was ¥30,000 in January 1989 when Japan started the Heisei Age but has yet to return to that level. But by the spring of 2019, when the emperor plans to abdicate, the Nikkei Average will probably be back to around ¥30,000. That means the stock market did not go up for a period of 30 years. Starting in 2019, if stock prices rise by 10% every year, the Nikkei Average will be ¥100,000 about 12 years later in 2031. This is quite possible. Stock prices worldwide have been climbing at an annual rate of approximately 10% for the past four decades. At this rate, the Nikkei Average can reach the ¥100,000 level. Consequently, from an extremely long-term perspective, people need to put as much money as possible in the stock market.

A good time for very short-term investments too

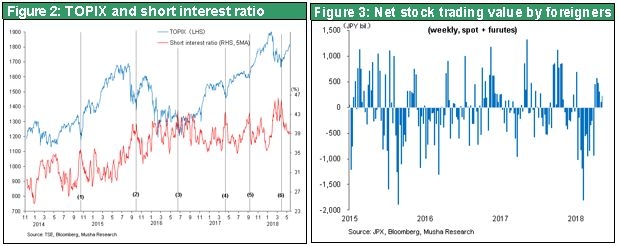

The timing is outstanding for very short-term investments. Technical factors and supply-demand dynamics were responsible for the sharp drop in stock prices in February and March. This downturn had nothing at all to do with fundamentals. Stock prices always rise rapidly immediately after a big increase in the short interest ratio on the Tokyo Stock Exchange. In March, the Tokyo Stock Exchange short interest ratio rose to a record-high 50%. We can therefore expect to see stock prices start climbing as this ratio drops quickly.

Investors are buying back speculative sales due to robust fundamentals

Net sales of Japanese stocks, mainly using futures, by foreigners reached an unprecedented level in February and March. At this point, foreigners will probably start reestablishing these positions. Foreign exchange rates are turning around too as the dollar’s decline has apparently ended at ¥105. Furthermore, no problems involving fundamentals or geopolitics are in sight. For these reasons, a big upturn in stock prices is probably about to begin in Japan.

Dollar pessimism is mistake; an extended upturn of the dollar has started

Many investors watch the dollar more closely than anything else. A large number of market observers believe the dollar is in the midst of an extended decline and will continue to weaken. But I think this is a mistake. Looking at fundamentals, there is no reason for a weaker dollar. Interest rate differences, economic strength and central bank monetary policies all point to a stronger dollar. Why do so many people expect the dollar to depreciate? The only possible explanation is the use of circular reasoning. As you can see in Figure 4, the dollar’s real effective exchange rate has repeated cycles of six years of strength and 10 years of weakness. Today, many people think that the dollar has started to decline because a period of a stronger dollar that began in 2011 reached its end in 2017. However, the key point here is that the dollar’s period of strength did not really start in 2011. The actual beginning was 2014. Between 2011 and 2014, the dollar hit an all-time low in response to quantitative easing on a massive scale by the Fed. Therefore, this period of a stronger dollar began only a few years ago. Both technical factors and the long-term trend tell us that the dollar has not reached the point where it will reverse direction and depreciate.

Above all, President Trump’s policy mix of monetary tightening and substantial growth in government spending is creating an environment conducive to a stronger dollar. As the dollar appreciated, there have recently been concerns about emerging country currencies. The world may be about to enter an era in which the dollar is one of the most important economic resources. In other words, we are now in era where procuring dollars will become essential for making international payments. Problems exist in China, North Korea and many other places in the world. The final weapon for suppressing these problems for the United States is freezing dollar-denominated assets. The dollar is so overwhelmingly powerful that freezing these assets gives other countries no option other than to do what the United States wants.

The US economy is declining as a share of the global economy. The United States was about half of the global economy at one point but is now accounts for only about 22%. Despite this decline, the dollar’s share of international payments and the share of dollar-denominated assets used for investments have increased during the past few years. According to The Wall Street Journal, dollars were more than 40% of cross-border loans in 2009 and more than 60% in 2016. This indicates that the age of the dollar is about to start. In addition, President Trump’s stance of reinforcing US hegemony by using coercive power globally is consistent with a stronger dollar. Another significant point is the big ongoing improvement in the US current account balance backed by the country’s very competitive high-tech industry. A reduction in the current account deficit would result in the beginning within a few years of an era in which the global supply of dollars declines. Simply put, this would be a dollar shortage era. This is why I think the dollar’s decline last year was nothing more than a deceptive move and a springboard for the dollar’s upcoming strength.

For these reasons, I think people have good reason for short-term and long-term optimism, including a 100-year life span and a ¥100,000 Nikkei Average.

(2) How should we view the policies of President Trump?

Business people are strong supporters of President Trump

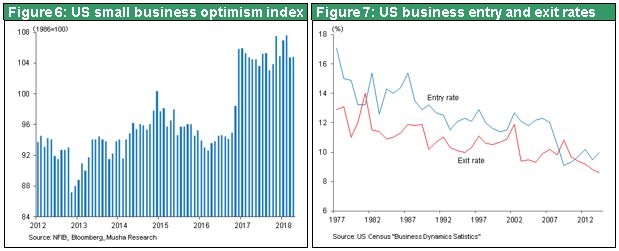

Determining how to evaluate President Trump, a president like no other before, is the key to analyzing current events. I think we can give the president a good grade from the standpoint of investments. I believe that many economists and members of the media are not properly evaluating the president’s economic policies. As Figure 6 shows, sentiment about the economy among US business people has become very optimistic after the 2016 election. According to a CNBC survey, President Trump has an approval rating of about 50% on Wall Street, far above the disapproval rating of just below 20%. This demonstrates that, unlike the assessments of the media, the US business community gives the president high marks. The reason is that the president’s economic policies are intended to raise stock prices and corporate earnings. Some people criticize these policies because of negative implications for the future. However, the president’s policies are having primarily positive effects from a short-term perspective.

Deregulation succeeded at stimulating entrepreneurial spirit

Economic initiatives during President Trump’s first year generally fall into two categories. One is deregulation. Idealism was a major characteristic of the Obama administration. But President Obama adopted policies that seemed to treat the economy as an enemy. As a result, the number of new businesses in the United States fell significantly and remained low. The Obama administration built a wall between the business community and Washington with the main goal of eliminating collusion between companies and the government. Taking these actions had the benefits of reducing the financial sector moral hazard and protecting the environment. On the other hand, economic vitality decreased. If we adopt a negative view, we can say that President Trump’s policies are strengthening collusion between companies and the government. But these policies are improving business sentiment and are likely to start raising the new company establishment rate. Increasing the activity of entrepreneurs is a major objective of the president’s commitment to deregulation.

Unprecedented corporate tax cut, fast growth of capital expenditures and stock repurchases will keep the stock rally going

Tax reform is the second category. In 2017, the United States enacted tax reforms that were the first since the Reagan administration and the largest in the country’s history. Some people view these changes as reckless. But there is no doubt that these reforms have positioned the United States for stronger economic growth. So I think we can say that there were major accomplishments during President Trump’s first year.

Shifting the focus from the economy to US hegemony in the second year

In his second year, President Trump is turning his attention to geopolitics now that economic measures are largely in place. Reestablishing US hegemony is the goal. The president is working on ways to hold back China, which is getting in the way of US hegemony. In association with this shift from the economy to geopolitics, President Trump has made several changes in his cabinet. Mike Pompeo replaced Rex Tillerson as Secretary of State and John Bolton replaced H.R. McMaster as national security adviser. The president also replaced Gary Cohn, making Larry Kudlow and Peter Navarro his top economic advisers. Appointing these hawkish and solidly conservative people demonstrates the president’s intention of containing China. Many people believe that global hegemony will shift from the United States to China if no changes are made. But the United States would never allow that to happen.

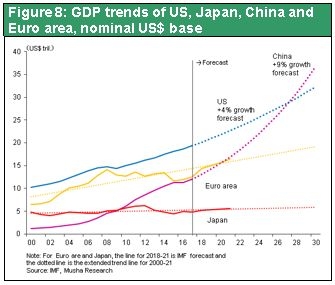

The United States and China obviously have an adversarial relationship. Looking at GDP trends in four major economic zones of the world, China overtook Japan in 2008 and surpassed the eurozone in 2016. At this pace, China will pass the United States in 2026 to become the world’s largest economy. If this happens, China would become the world’s most powerful country, surpassing the United States in both economic and military terms. This prospect is clearly creating rapidly increasing alarm in the United States. To stop this reversal of roles, the United States must contain the growing strength of China’s economy.

Starting a trade war shows US determination to stop China’s increasing clout

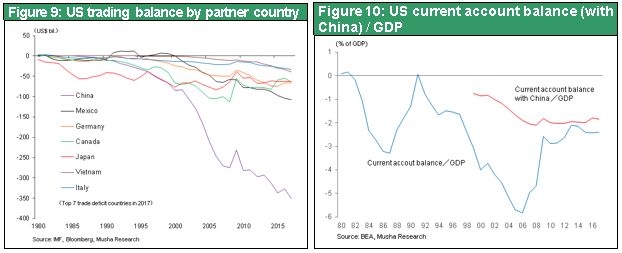

The United States has played a role over many years in the growth of China’s economy. It’s as if the United States had been supplying China with milk. In 2017, The United States had a trade deficit of $375.7 billion with China, which was about half of the total US trade deficit. This deficit is much more than the US trade deficit of $50-$60 billion with Japan during the US-Japan trade friction that happened around 20 years ago. In addition, the US current account deficit with China has been consistently just below 2% of the US GDP for the past decade. The total US current account deficit is 2.4% of GDP, so China accounts for almost all of this deficit. Another way to express this deficit is that the United States is sending 2% of the income of the entire population to China as an income transfer to pay for the trade deficit. Naturally, this contributed to the growth of the China’s economy.

Stopping this situation is the biggest objective of US-China trade friction. China’s enormous US trade surplus equates to a free ride because China has been using a variety of unfair trade practices and industry protection policy. The United States will make this stop. US Trade Representative Robert Lighthizer played a key role in lowering Japan’s trade surplus during the period of US-Japan trade friction. Now he intends to use this experience to pry open China’s markets. We can expect upcoming events to resemble somewhat the outcome of US-Japan trade friction. There will probably be numerous negotiations covering a broad range of categories that continue for five to 10 years. The United States will show its strength by exerting pressure and imposing sanctions in many business sectors.

The current US-China relationship is one-sided. Since China is the only one earning profits from this relationship, US demands will probably be accepted. China does not want to shut down its trade with the United States no matter what sanctions the United States threatens to impose. Consequently, China’s stance is that putting up with US demands is the best course of action. For at least the next several years, we will probably see China carefully evade US demands while continuing to negotiate for reaching an agreement that the United States can accept.

Measures to contain China will be successful

Most of all, China and the United States are focusing on their high-tech industries. In particular, progress with the development of next-generation 5G telecommunication technology will determine which country becomes the leader of the global high-tech industry of the future. Work on this technology has reached the most critical stage. The United States is probably determined to prevent China from becoming the leader. In fact, the United States is even asking China to abandon Made in China 2025, a blueprint for establishing a dominant position in the high-tech sector. But does the United States have the means to force China to change direction? The answer is prohibiting the use of the dollar. Taking this step would destroy the Chinese economy. However, this is very unlikely to happen because it would be equivalent to a declaration of war.

One action that the United States has taken is prohibiting ZTE Corporation from doing business with US companies for seven years because ZTE illegally exported goods to Iran. ZTE buys smartphone semiconductors from the US company Qualcomm. Terminating ties with Qualcomm will prevent ZTE from making smartphones and the company will no longer be able to continue operating. Similar measures are also being considered for the world’s largest telecommunications equipment maker, Huawei Technologies. This is the bitter medicine that the United States forced China to swallow. In the US - China trade friction, the United States is apparently trying to use a big stick to force China to succumb to its demands. The Trump administration is using this method with China just as it does to deal with North Korea and Iran. Until now the United States was like a gentleman. But now the Trump administration is using money and coercion to create a world order that reflects US interests. I believe this approach is very likely to succeed. The reason is that the competitive edge of US industries has already improved dramatically.

Highly competitive industries and a falling current account deficit are behind President Trump’s big-stick negotiations

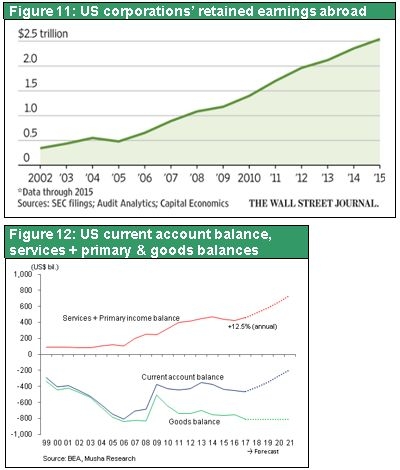

US companies rule the internet domain. These companies have generated massive profits overseas. In 2015, US companies had $2,500 billion of overseas cash from profits and this figure is believed to be more than $3,000 billion now. Keeping this huge volume of accumulated earnings in other countries exerts considerable upward pressure on the dollar. The US annual current account deficit has dropped from a peak of $800 billion to the $400 billion level. The reason is big increases in service exports and the surplus of primary income balance as the trade deficit remained level.

Services and primary income consist primarily of global earnings generated by innovative US technologies. This category of income was almost nothing only a little more than 10 years ago. Today, this income offsets about half of the total US trade deficit. This explains why the US current account deficit is only half what it used to be. If this deficit continues to fall at this pace for seven or eight more years, there will be a dramatic drop in the US current account deficit. The result will be a global shortage of dollars. Since this would strengthen the dollar, the currency of the world’s superpower, the United States would have virtually an imperial influence over the world.

People have many different views of President Trump’s policies. But it is clear that the United States is becoming much more powerful with respect to economic innovation and the competitive superiority of US industries. The Trump administration’s policy of using money and a big stick to apply pressure worldwide is highly effective and likely to be successful for the time being. Therefore, the world stock price rally will still continue.

Refusing to allow the yuan to fall is the highest priority concerning China

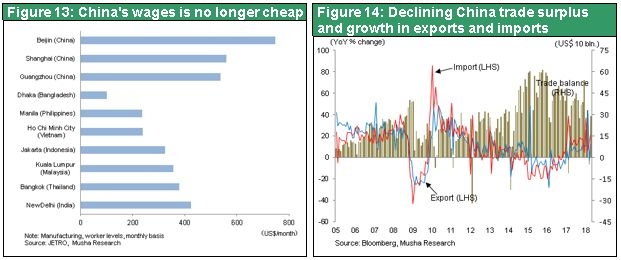

There are three US demands to China. First is stopping the free ride and convincing the country to give up on its goal of high-tech global leadership. Second is opening up markets within China. Third is absolutely refusing to allow the yuan to depreciate. The third demand is the most important from the standpoint of markets. China’s trade deficit will plummet if the yuan does not lose its value. Wages in coastal regions of China are now significantly higher than in all of the ASEAN countries. Salaries in China are so high that some of the engineers in the country’s high-tech sector are believed to be earning more than similar engineers in Japan do. The high cost of labor means that not allowing the yuan to depreciate will make China’s exports much less competitive.

China’s trade surplus is already declining rapidly, falling at an annual rate of about 20% during the past few years. A few more years from now, China may have a much smaller trade surplus and a current account deficit. This would increase pressure on foreign companies and investors to start moving their enormous volume of investments out of China. The resulting resurgence of worries about foreign currency reserve would probably cause the yuan to plunge at some point. I think this would happen at the same time as the bursting of China’s asset bubble and the start of a financial crisis. Moreover, I expect these events to occur about three to five years from now. Until that time, I believe the United States will resolutely oppose any decline in the yuan’s value. As a last resort, the United States would threaten to freeze the use of dollars or stop the supply of semiconductors used in high-tech applications or the supply of other products. Before that happens, China is likely to self-destruct. The United States will absolutely not allow China to have the world’s largest economy. I believe that President Trump’s policy of using money and a big stick to prevent this from happening will succeed.

(3) New industrial revolution, appropriate policy triggers large stock boom

Increase in profits due to dramatic increase in productivity, low inflation · low interest rates

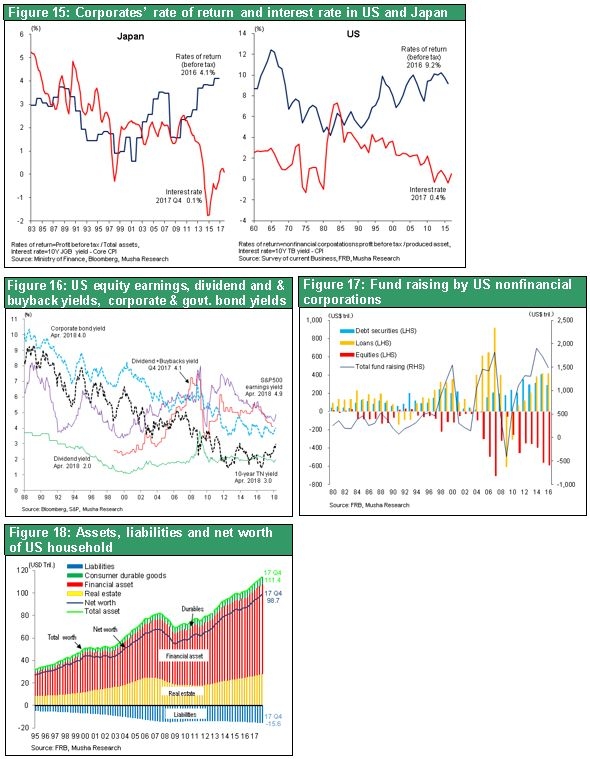

The New Industrial Revolution is dramatically boosting productivity. As a result, companies are making profits with less investment and employees, and so the corporate earnings are on the rise. On the other hand, because there is no way of putting profits to good use, interest rates are not rising, or there is an excess of people left over, so neither wages nor prices go up. That is to say, we find ourselves in a strange situation in which prices and interest rates are not rising even though companies are profitable and operating in a booming economy. What this problem requires is recognition that it is necessary for this surplus money and people to be used to create effective demand. Musha Research believes that the stock market will rise dramatically when such a policy is launched. The market is responding positively because both Abenomics and the major tax cuts of the Trump regime are such effective demand policies.

Correct economic policy is essential and the stock market is becoming a place for returning corporate profits

In this situation the role of the stock market is changing dramatically. A while ago the role of the stock market was to be the place of procurement of funds for industry. But now the role of the American stock market has become to be the place in which to return corporate profits to shareholders. Companies capture the earning yield of 5% (earning a 5% profit on the stock price), pay 2% in dividends to shareholders and return to the market some 3% to 4% by buying back their own stock (= stock price will rise, shareholder value will increase, household wealth will increase). In other words, the stock market is the place through which 100% of the profits are returned. As the stock market fulfills its proper function corporate profits are flowing back into society. It is precisely because the American economy is revolving through this cycle that households are able to consume. The New Industrial Revolution is a social phenomenon that is boosting stock prices significantly.

(4) Japan’s Two Distinctive Advantages: Geopolitics and International Division of Labor

Japan has become the only one in a number of domains in terms of international division of labor and the quality of its technology

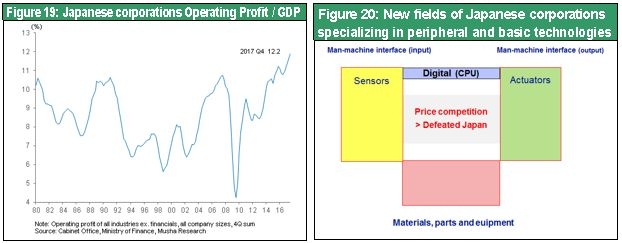

Musha Research believes that the time has now come when the dominance of Japan is strongly on the increase. Corporate profits are at their highest. The core of profitable high-tech business (semiconductors, liquid crystals, personal computers, smartphones, TVs, etc) has now been largely snatched away from Korea, China, and Taiwan. Moreover, America dominates the high-tech cyberspace and the Internet platform. At first glance, Japan might seem to be on the losing side, but the reason why it is generating the all-time highs in profits is that Japanese companies have created monopolies by carving out lots of exclusive businesses in producing things that cannot be made by any other country in the world. With the core hi-tech sector now a ferociously fierce battlefield, and China, Korea and Taiwan investing in semiconductors and liquid crystals, prices will most probably crash. The peripherals, however, are not made by these countries. Therefore, Japan is in a favorable position.

Advantage in scarcity, foreign-exchange-free, friction-free

The intensity of competition between Korea - China, Taiwan - China, Germany - China is currently escalating in high-tech. China's Alibaba Group and Tencent Holdings are also clashing in the challenge to become China's Internet platform for US companies. But, leaving this aside, there is almost no competition for China-Japan and US-Japan. This is because to try to make China high-tech, Japanese equipment, parts and materials are needed. Japan occupies a remarkably advantageous position in terms of the international division of labor. The superiority in the international division of labor is supporting the massive increase in Japanese corporate earnings. Meanwhile, Japanese economy is going to be more free from foreign exchange, and trade friction issues. For example, Japan is subject to the steel and aluminum tariffs implemented by the current Trump regime. Japanese companies are not panicking however because the steel and aluminum sold by Japan are not marketed on price so much as on the quality that only Japan can deliver. Even if the yen strengthens, even if the tariff rises, it is the counterparty's customers who will bear the cost because the counterparty has to buy from Japan. This trend is spreading to cover all businesses in Japan. There are no industries in Japan that are surviving by competing on price. Non-price Competitiveness, Technology and Quality Advantage. The Japanese economy has now reached a stage where its value-creation mechanism has attained a historic peak and has the best contents in the world.

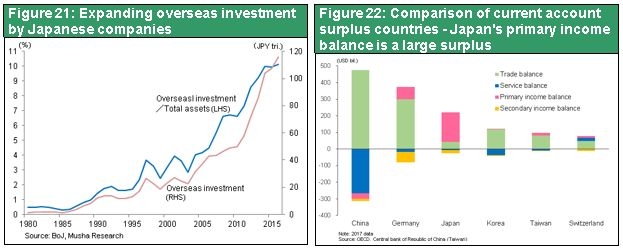

Establishment of overwhelming powerful global supply chain – against the backdrop of massive primary income balance

Looking at the breakdown of the current account balance of the major countries, we can see that the balance (figure) in the black in the current account surpluses of the countries other than Japan is the trade surplus. In China, Germany, South Korea, Taiwan, and Switzerland, they are making profits by depriving their partner countries of employment. For Japan alone, most of the surplus is provided by the primary income balance. In other words, it is a surplus earned by manufacturing in factories abroad. Therefore, the surplus in Japan is a surplus born as a result of hiring overseas. With the establishment of what is such an extremely rare global supply chain in global terms, Japan has created a mechanism free of foreign exchange and trade friction, and its background lies in its overwhelming advantages in skills and quality. This will become the major driving force in boosting Japan's economy and stock prices massively in the era that follows Heisei.

US-China confrontation advantageous to the geopolitical position of Japan

The confrontation between the US and China over world hegemony is getting really serious. In this situation, the position of Japan is becoming remarkably advantageous. The direction of the trend in supremacy between the United States and China will be decided on whether Japan leans towards the US or China. For the United States, Japan is now becoming more important than any of its traditional allies, such as the UK and Israel. A strong Japanese economy, that is to say a strong Japanese economy that can compete with China, is directly linked to the national interest of the United States. Yen appreciation, trade friction, and similar forms of Japan bashing would not occur. This would no doubt further strengthen Japan's competitive advantage in terms of the international division of labor.

Viewed in this way, perhaps we can see that the prospects for human lifespans of 100 years and the Nikkei average at 100,000 yen are not so much hopeful observations, but rather the most likely future figures.