Aug 01, 2018

Strategy Bulletin Vol.204

Let’s assume stock prices reflecting 2% inflationary expectation, sealed exit theory

- Should the BOJ take a guidance target for stock prices into view?

(1) Completely shutting down talk of a monetary easing exit has positive implications

No monetary easing exit until 2020 is equivalent to additional easing

Now that quickly reaching the 2% inflation target is very unlikely, patience and perseverance are what is needed at the Bank of Japan. In its forward guidance on July 31, the Bank of Japan said there is no possibility of an exit from monetary easing any time soon. We can interpret and evaluate this statement as a sign of additional monetary easing. Investors believe there will be no change in the Bank of Japan’s stance until the effects of the October 2019 consumption tax hike have been assessed. This view will probably result in more risk-taking. Japan has been mired in prolonged deflation since 2000. In addition, when the global financial crisis started in 2008, Japan started quantitative easing four years later than in the United States. Delaying quantitative easing triggered an excessive appreciation of the yen. The result was the start of deeply entrenched deflation on a scale that had never been seen before anywhere in the world. The distinctive characteristics of Japan’s deflation made it quite obvious that achieving the 2% inflation target would not be easy. Consequently, there is no need to be bothered by the static from critics of quantitative easing. The only way to regard the stance of these critics is that they truly believe that ending deflation is unnecessary.

All the talk during the past week about a possible shift in the Bank of Japan’s policies is clearly nothing more than noise. Sales by investors with short positions who were worried about an exit from monetary easing sparked a big sell-off of stocks and of the dollar in relation to the yen. But the Bank of Japan is still retaining its 2% inflation target. Accomplishing this goal will require a big increase in stock prices (higher valuations) and measures to prevent the yen from appreciating. The outlook for the enactment of policies that would make the yen stronger and stock prices weaker was clearly fabricated as an excuse to sell stocks. Once the Bank of Japan made its July 31 announcement, financial markets recovered as investors accepted the bank’s statements at face value.

Weak basis for criticizing the Bank of Japan’s policies

Nevertheless, there have been many comments during the past week insinuating that the shift in the Bank of Japan’s position has created a sense of disappointment regarding stock prices and the exchange rate. These comments come from people who are adamantly opposed to massive monetary easing based on two beliefs: (1) the 2% inflation target is unnecessary and (2) raising inflation to 2% is impossible. If this is true, then the Bank of Japan will eventually have to admit defeat. Opponents of Japan’s extreme easy-money policies have consistently opposed QQE since Haruhiko Kuroda became the governor of the Bank of Japan in 2013. Since 2013, economic growth has increased, corporate earnings have been strong, the number of jobs has increased significantly, stock prices are up and the yen is down. But people who are critical of QQE are not impressed with these accomplishments. All they look at is the failure to achieve 2% inflation. This is unfair. There is immense significance to the suppression of criticism of extreme monetary easing, which can be regarded as nothing more than noise with respect to the Bank of Japan’s policies.

(2) The Bank of Japan can – and should – correct the current unjustified stock price weakness

A commitment to asset prices is what will really end deflation

A theoretical explanation exists for how extreme monetary easing can create expectations for inflation. But this is a theory about the probability of an outcome and is very difficult to prove. This is the Bank of Japan’s problem. Inflation is a dependent variable for the money supply. The Bank of Japan and people who believe in reflationary measures think that monetary measures can stop deflation. But critics of QQE are skeptical. There is no doubt that expectations for inflation change as they go through many channels (the transmission mechanism). No direct and explicit link between these expectations and monetary policy exists.

It’s time for the Bank of Japan to establish a guidance target for stock valuation

No one can deny that stock and asset prices are dependent variables of the money supply. Moreover, the money supply determines foreign exchange rates, as long as the monetary policies of other countries remain unchanged. As a result, extreme monetary easing can directly influence exchange rates and prices of stocks and other assets. The cause-and-effect progression begins with monetary policy and advances to stock prices and exchange rates and then on to the expectation for inflation. Stock prices and exchange rates can be viewed as intermediary factors for creating an outlook for inflation as the ultimate objective of monetary policy. This leads to the conclusion that we should be able to expect the level of stock prices and exchange rates that equate to 2% inflationary expectation. Naturally, the one-sided determination of exchange rates is impossible because other countries are involved. However, stock prices are well within the reach of a country’s own monetary policies.

The price-earnings ratio (PER) is a key indicator of a stock’s valuation (in effect, its popularity). How much do stock prices have to increase to make people anticipate 2% inflation? Based on the current earnings of companies in Japan, a multiple of 13 times earnings per share results in a Nikkei Average of ¥22,500. If the PER climbs to 20, the Nikkei Average will increase to ¥34,000 and a PER of 26 would boost the Nikkei Average to ¥45,000.

Since there is a clear cause-and-effect progression as I explained earlier, the Bank of Japan should have a guidance target for stock prices. In more accurate terms, the target would be for increasing the PER (valuation). Stock prices (valuations) equivalent to 2% inflationary expectations would certainly be much higher than they are now. Discussion of the commitment to this valuation level is more important as the Bank of Japan demonstrated its resolve to boost inflation to 2% and sated that there were large number of policy measures at the bank’s disposal for accomplishing this goal.

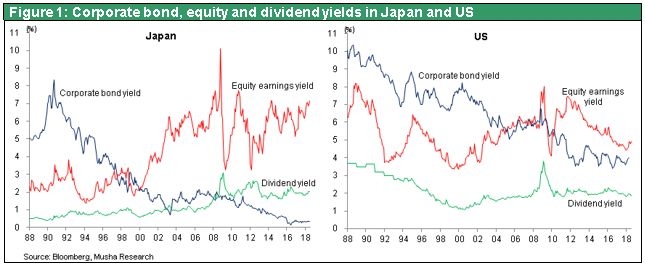

As you can see in Figure 1, the return on stocks in Japan is currently far higher than the return on bonds. The historically low valuations of Japanese stocks are undeniable proof of the existence of significant mispricing.

US quantitative easing succeeded as a commitment to asset prices

Many people are critical of a central bank commitment to asset prices because it appears that the bank is participating in the creation of an asset bubble. But the success of US quantitative easing tells a different story. At times, central bank interventions in asset prices are correct and even essential. Quantitative easing under the leadership of former Fed chairman Ben Bernanke restored the health of financial markets that were on the brink of collapse. This revised risk-taking and the animal spirits of investors, which had both been nearly non-existent. Taking these actions returned the economy to a normal trajectory.

The defining characteristics of this monetary easing were the rapid quadrupling of the Fed’s balance sheet and a rebound in prices of securities that had plunged to abnormal lows. The Fed had abandoned its neutral position in financial markets and instead become a consistent buyer. Purchasing assets at low prices to boost their values restored an orderly financial system. As a result, the risk premium, which had increased to more than during the Great Depression, fell back to its original level. Stock prices had plummeted 60% over a period of one and a half years, about the same as during the Great Depression. But once the Fed acted, stock prices doubled over the next two years to return to where they were before the global financial crisis.

Central banks have an obligation to correct mispricing

Can a country raise securities prices by simply printing money faster? This action would spark intense criticism as the ultimate dubious money-making scheme. Nevertheless, there is no doubt that printing money like this prevented the global economy from falling into a deep recession. The conclusion is clear. The Fed’s decision to take forbidden actions that went beyond its conventional boundaries was vital to achieving a turnaround of the US economy. Despite this success, some aspects of this unprecedented monetary easing did not go well. The obvious criticism that “there is no reason for something like this to be entirely successful” is persuasive. One position is that everything will go well with extreme monetary easing if it simply succeeds at altering the public’s expectations. However, it is doubtful that this statement can withstand straightforward criticism like “this is a fantasy of someone on drugs” and “there is no reason to expect a change involving problems of the real world.”

Market interventions as part of extreme monetary easing will fail unless interventions reflect actual market conditions. For instance, a central bank may briefly lower the risk premium by purchasing bonds. But if a recession subsequently deepens and produces many bankruptcies, the risk premium will surge again. Bonds will become worthless and the central bank will hold a large volume of non-performing assets.

Operations overseen by Ben Bernanke were successful precisely because markets had become even more distorted than the actual situation warranted. Corporate bonds factored in an unprecedented number of bankruptcies and stock prices factored in the elimination of earnings at all companies. But the actual health of the economy had not declined to these levels. As a result, Mr. Bernanke’s bold decision produced the desired results.

The Bank of Japan’s stock commitment is correct – Don’t be distracted by static

Stocks are the origin of mispricing in Japan’s financial markets today. Prices of stocks are clearly too low. As Figure 1 shows, the gaps between the returns of stocks and bonds・bank deposits have widened dramatically. Stocks in Japan have an earning return of 7% and a dividend return of 2%. In comparison, Japanese government bonds yield nothing and bank deposits yield almost nothing. Never during the past four decades has a return gap of this magnitude existed. Gaps of this size do not exist in other countries either.

This situation shows that people who own stocks can receive a very large surplus return (risk premium). In other words, investors have become extremely afraid to take on the risk associated with stock ownership. The reason is doubts many years ago about the sustainability of corporate earnings. But now there is no uncertainty at all. Perhaps an excessive aversion to risk is responsible for a variety of problems. To solve these problems, the Bank of Japan should take actions needed to correct the stock risk premium, just as the Fed chairman Ben Bernanke did in 2009.

When the Bank of Japan started buying ETFs, many people thought this would distort markets because the public sector should not be exposed to the risk of falling stock prices. However, this criticism is wrong and should not influence the Bank of Japan. Investors who do not have information about individual stocks have access to a variety of index funds. As a result, public and private-sector investments in ETFs have an effect on the performance of financial markets worldwide. Furthermore, the Bank of Japan can buy Japanese government bonds, which have no return and virtually risk of a downturn in prices, or stocks with a 2% dividend yield and substantial upside potential. Which asset category is better in terms of soundness? Shouldn’t the Bank of Japan take the lead in starting an intrinsic value war regarding asset prices?

(3) US quantitative easing resulted in higher prices of assets

At what level would stock prices produce expectations of 2% inflation? Japan can learn from the United States, which is the world’s only developed country that escaped from a liquidity trap.

The United States escaped by using the following steps: Quantitative easing → Higher asset and stock prices → Growth in household assets and household income from assets → Growth in consumer spending → Rising expectations for inflation.

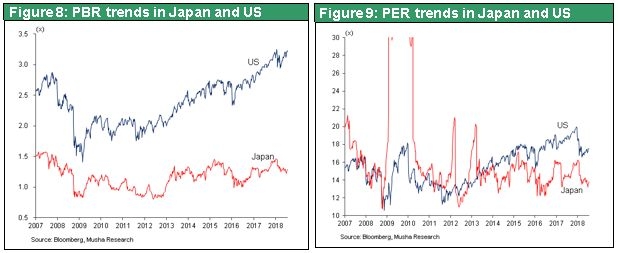

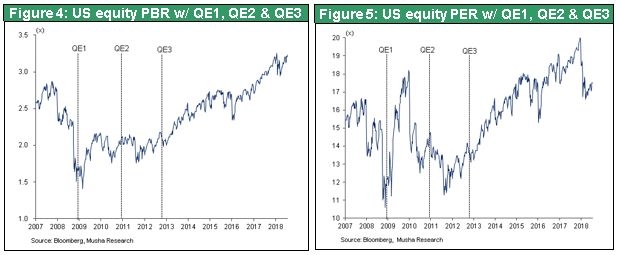

In the United States, stock valuations (S&P 500) doubled in terms of the PBR, which increased from 1.6 in February 2009 to 3.2 in July 2018, and increased 61% in terms of the PER, which increased from 10.9 in September 2011 to 17.5 in July 2018. In comparison, the PBR of Japanese stocks (TOPIX) increased 44% from 0.9 in February 2009 to 1.3 in July 2018 and the PER increased only 28% from 10.7 in July 2012 to 13.7 in July 2018. Since the United States has largely achieved 2% inflation, Japan probably needs a similar improvement in stock valuations after the financial crisis in the US. Consequently, Japan needs a 39% increase in the PBR and a 26% increase in the PER in order to raise stock prices to a level equivalent to a 2% inflationary expectation.

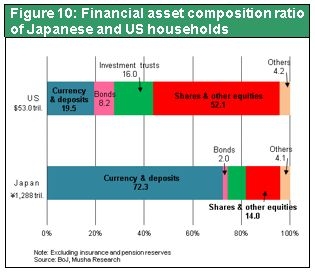

Figure 10 shows the ratio of stocks and mutual funds to cash and deposits in the financial assets of US and Japanese households (excluding pension reserves and insurance). In Japan, cash and deposits are 70% of these assets and stocks and mutual funds are 20%. This ratio is reversed in the United States, where the share of cash and deposits is only 20% and stocks and mutual funds are 70%. These numbers clearly show the Japanese public’s unusually high aversion to risk.

All these points lead to the conclusion that it is probably time for the Bank of Japan to make stock valuations a key indicator for achieving the goals of the bank’s policies.