Aug 27, 2018

Strategy Bulletin Vol.206

Are Japanese stocks on the verge of a turning point?

Q) The Nikkei Average is directionless as investors adopt a wait-and-see stance regarding China. Why are Japanese stocks unable to stage a rally?

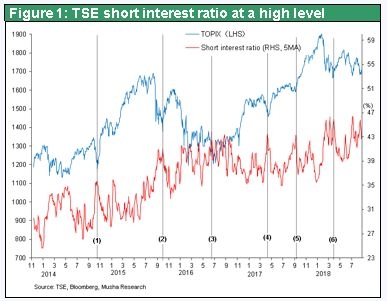

A) It all comes down to supply and demand. Sellers have the upper hand now. The short interest ratio in Japan has climbed to an all-time high. It may be the symptom of turning point of the market. There is no serious problem with fundamentals. Companies in Japan are reporting strong earnings and stocks are undervalued. The only source of concern is the US-China trade war. Investors should worry about this if the trade war is going to deal a severe blow to the global economy. However, US stock prices reached a new high end of last week, so US investors are paying no attention at all to the trade war. It is still too soon to say there are absolutely no worries. However, the trade war, although not being settled, will probably continue without any serious effects in a negative sense. Causes of concern among stock investors involving the trade war will probably disappear at some point. The result is likely to be a stock purchases on a massive scale due to short covering.

Q) Many people think the US-China trade war will have a major negative impact. But this is not necessarily true, is it?

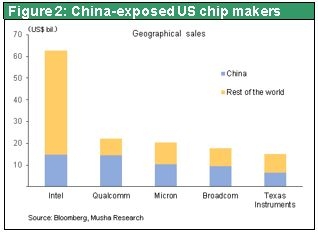

A) The short answer is that US semiconductor manufacturers rely on exports to China for more than half of their sales. Also, almost all of smartphones sold in the United States are imported from China. Therefore, the paralysis of US-China trade would cause the economies of both countries to collapse. This is inconceivable. Investors should expect the trade war to be resolved in a way that prevents a crisis. US consumption, the largest component of demand in the global economy, is very strong and showing no signs of weakening. Also, China has started taking actions to prop up its economy, as I will discuss later. As a result, demand will remain firm on a global scale. Assuming there is no change in total demand, the trade war and tariff raise will not alter the overall supply even if the trade war shifts the sources of supply to different locations. For instance, a decrease in imports from China may be replaced by imports from other countries. Or production in the United States may increase. Therefore, a downturn in the supply from China should create beneficiaries in other countries. Although the trade war may reshape the global supply chain, this would result in the reconfiguration of the global division of labor over time. So even if problems occur, investors should not expect these problems to disrupt our lives or the economy.

Q) What is your view of emerging country risk, such as the recent plunge in the value of the Turkish lira? Will emerging country currencies fall sharply as people move money out of emerging countries with problems and into the United States?

A) The United States is attracting a large volume of money. The United States is steadily taking money away from emerging countries and this shift is creating a negative impact. The biggest reason for the shift of funds to the United States is the strength of the US economy. The United States is the world’s only economic winner and this is making the dollar stronger and stronger. Therefore, the question is whether or not the vibrant US economy will become the cause of a risk-off environment that creates a worldwide bear market. Our answer is that the strength of the US economy is very likely to support the global economy and push up asset prices. Eventually, the market consensus will probably embrace the view that the relative strength of the United States will positively affect the entire world.

Negative effects on countries that rely on the dollar for debts cannot be avoided if the dollar appreciates. This explains why investors have been selling the currencies of Argentina, Turkey and other countries. The real economy (fundamentals) in Turkey is not terrible. However, Turkey has a substantial amount of foreign debt. As a result, the lira’s free fall has sparked a negative cycle that includes rising inflation. Moreover, the administration of President Erdogan has taken away the freedom of the central bank concerning monetary tightening, which is essential for slowing a currency’s decline, and other actions. The Trump administration’s decision to hike tariffs on imports from Turkey due to human rights violations has further heightened worries about the lira. Nevertheless, at some point a shift in policies or a switch from speculative sales of the lira to buying back the lira is likely to stop the currency’s free fall and end this crisis.

The dollar’s strength is basically a reflection of the country’s strength. From a global perspective, a strong dollar is therefore a reason for more risk-taking. This is why the current downturn in emerging country currencies will probably not continue for a long time.

Q) In the United States, news reports have been full of stories concerning President Trump about scandals and involvement with Russia. There is news on the talks of falling president’s approval rating and impeachment. What is your view of these events?

A) Many people think that President Trump is a vulgar person and do not have a favorable view of him. However, has the president committed a crime serious enough to warrant impeachment and removal from office? We need to divide this issue into two parts to examine the likelihood of this happening. But the most critical point is if any of the so-called Russiagate allegations can be proven.

Former Trump campaign chairman Paul Manafort has been convicted of several crimes. Now Michael Cohen, the president’s former general counsel, has agreed to plea deal with federal prosecutors while admitting the charges of prosecution. Illegal activity involving Russiagate is not the reason. Mr. Cohen took this action because of personal crimes such as tax evasion and bank fraud. Special Prosecutor Robert Mueller and others are searching for some sort of evidence as they use numerous plea bargains in an effort to get to the bottom of Russiagate. But no evidence has been discovered yet. Due to this situation, financial markets have not reacted to these events. The Wall Street Journal clearly stated that Russiagate allegations are unlikely to increase the possibility of an impeachment.

Q) Another source of concern is statistics in China that indicate economic growth is slowing. Commodity markets are signaling this slowdown, and the price of coppers, for example, is showing big drop.

A) The outbreak of the trade war prompted China to quickly reverse its monetary policy that was aimed at preventing an asset bubble and start monetary easing. Real estate prices in some parts of China have already started to climb. Furthermore, China has announced massive infrastructure investments, mostly for resumption of high-speed railway and subway projects, to stimulate the economy. All of these measures to back up the economy will probably start appearing in the real economy within a few months, resulting in improving economic statistics. Current economic weakness in China is nothing more than the remaining effects of policies that started in 2018 for preventing an asset bubble and holding down infrastructure investments. The biggest risk for China is the considerable likelihood that the trade war prompts global companies to stop building factories in China and take other actions that sharply reduce their investments in China. This risk will continue to exist regardless of how much China attempts to prop up its economy. In fact, there are worries about a temporary slowdown in high-tech investments in China.

Q) In your recent Strategy Bulletin, you said that signs of China’s decline are emerging. You said that foreign currencies and foreign exchange rates would be the key factors.

A) The United States is exerting pressure on China in many ways. Most of all, the United States is probably demanding that China never allow the yuan to depreciate. Consequently, although the yuan is weak right now, I think a further significant decline will not happen. China too does not want the yuan to decline. A drop in the yuan’s value would increase fears about financial stability that could subsequently spiral into worries that cause stock prices to fall and other events. After all, a drop in the yuan triggered the 2015 China shock. For these reasons, a devaluation of the yuan is probably not an option for China’s financial authorities. That means the cost of labor in China, which is already higher than in any ASEAN country, will remain high.

China’s ability to compete in export markets will continue to decline. At the same time, China’s large volume of high-tech investments has produced rapid growth in imports of high-tech machinery, materials, components and other products. China’s trade surplus has been falling 20% to 30% every year and will become a deficit in a few more years. This will probably result in a big drop in China’s foreign exchange reserves. If this happens, China will no longer be able to continue monetary easing in order to restore its strong domestic demand. The country will be forced to adopt tight-money policies to defend the yuan. Switching to this stance would destroy the asset bubble and start a cycle of negative events. A few years after that, having exhausted all possible economic initiatives, China could start heading for a financial crisis.

However, all these events are expected to occur after several years rather than now. Investors should start making preparations due to the possibility of a severe crisis, although this will not happen in the near future. The ongoing shift taking place in China signals the impending end of the China era. The country became the world’s primary manufacturer as companies around the world built factories there. But China has passed its peak and we are now advancing to an era when companies start moving their factories to other countries.

Q) Returning to stock prices in Japan, please explain what area in Japanese stocks, you think, is appealing

A) Japanese companies have established an extremely powerful position within the global division of labor. But many investors are still not aware of this advantage. Rather than this, global investors’ concern is that Japanese companies will be sacrificed by the trade war. However, the outstanding technologies and high quality of services of Japanese companies are starting to attract an enormous volume of business on a global scale. Investors should buy Japanese companies that have no peers in the world. There is no need to focus on any particular industries.