Sep 19, 2018

Strategy Bulletin Vol.208

The secret behind the remarkable improvement in JP corp earnings & prospects for its sustainability

- International division of labor within companies is making overseas operations a profit center

(1) Investors are ignoring the remarkable improvement in earnings

How should we view this historic upturn in profitability?

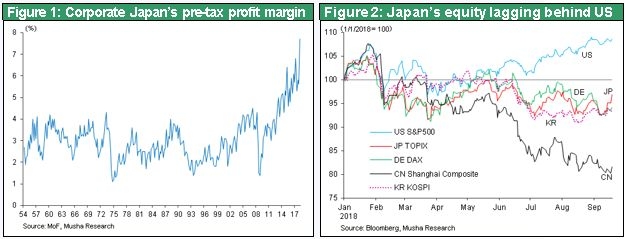

On September 3, Japan announced Corporate Statistics Report in the second quarter of 2018. The increase in profitability was a big surprise to overseas media companies. The ordinary income to sales ratio was 7.7% for all industries (excluding finance and insurance) and 10.5% for manufacturers. Both profit margins are all-time highs. As Figure 1 shows, ordinary income to sales ratio stayed between 2% and 4% during Japan’s postwar rapid growth period and all the way to the global financial crisis of 2008. Since the start of Abenomics, a period of only five years, this ratio has more than doubled. This is a spectacular improvement that is still gaining momentum.

Overseas investors and economists doubt the sustainability of this improvement

The Financial Times on September 13 and the Wall Street Journal on September 10 printed article about Japan’s rising earnings on the first pages of their business sections. But there was no single interpretation. Even as Japan’s profit margins rise to unprecedented levels, the country’s stock prices remain sluggish. Both newspapers said that concerns about the sustainability of strong earnings are the cause of the low stock prices. There are apparently two major reasons behind this thinking. First, sales at Japanese companies have not grown much in relation to the improvement in profitability. Second, many observers believe higher profit margins are primarily the result of one-time actions to boost productivity, such as restructuring, cost cutting and strengthening corporate governance. The same doubts exist in Japan. There have been almost no media reports within Japan about record-setting profitability because Japan’s media companies have little interest in a long-term perspective. As a result, the majority of economists and market participants are still urging people to be careful about Japan’s economy and financial markets.

People are overlooking the true cause of higher profitability – A new business model

Musha Research believes that people are wrong to be skeptical about Japan’s rising profitability. Global investors and many economists are probably overlooking the true cause of this sudden increase in profit margins: a major transformation in the business model of Japanese companies. Furthermore, this shift has been accompanied by strong growth in the contribution to earnings of the overseas operations of Japanese companies. These points lead to the conclusion that this upturn in earnings is both sound and sustainable.

Short selling by foreigners will not continue

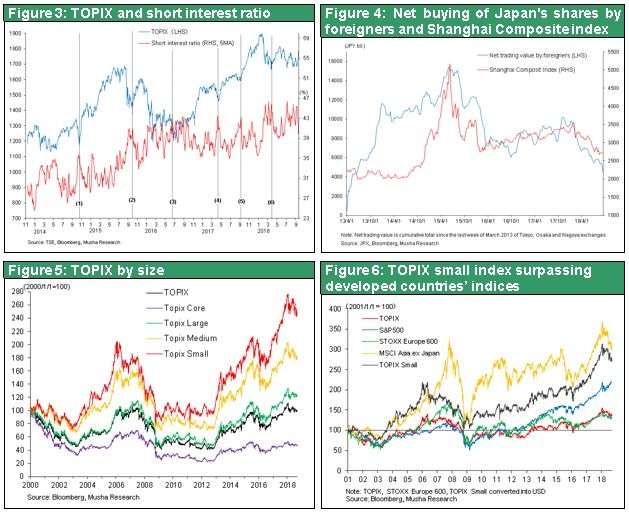

Foreigners have been selling stocks in Japan on a large scale consistently since February. Short selling of Japanese stocks by foreigners since January totaled ¥4,000 billion, the similar amount of foreigner short selling Aug. And Sept. in 2015. Moreover, due mainly to foreigners’ short selling, the Tokyo Stock Exchange short selling ratio has increased to a record high of 45%-48%. These short selling have prevented the Nikkei Average from moving above ¥23,000. Two misperceptions are probably linked to foreigners’ short selling of Japanese stocks. First is the erroneous belief that Japan will be a victim of the US-China trade war. The reasons that the trade war will not damage Japan were explained in Strategy Bulletin No. 207. Second is the error of overlooking the strong profitability of Japanese companies. Profit margins are climbing because Japanese companies have dramatically transformed their business models. This change has also enabled their overseas operations to contribute to earnings. If these are actually the reasons for higher earnings, then prospects are excellent for even more earnings growth in Japan.

No reason to expect Japanese stocks to move in tandem with Chinese stocks

Figure 4 shows the relationship between Japanese and Chinese stocks using data prepared by Shigeo Ichioka. In recent years, there has been a strong correlation between changes in foreigners’ purchases of Japanese stocks and stock prices in Shanghai. In the second half of 2015 and again in the first half of 2018, stock prices in China fell at the same time foreigners were selling Japanese stocks. The reason is that, even though Japan is benefiting from the US-China trade war, global investors who had decided that Japan would be damaged were shorting Japanese stocks as a substitute for selling Chinese stocks. When Chinese stock prices plunged during the 2015 “China shock,” stock prices in Japan fell 30%, about the same as the downturn in the Shanghai stock index. Japanese equities were one of the worst performers in the world at that time. In 2018, investors again are probably adopting a negative view of Japanese stocks because they think selling Chinese stocks means selling Japanese stocks, too. However, Musha Research is convinced that there is absolutely no legitimate reason for this action.

No end in sight to the superiority of the Nikkei Average

For the time being, the Nikkei Average will continue to lead stock prices upward. But some investors are sounding an alarm because the TOPIX has been peaking at lower and lower levels in recent months. But investors should regard the gap between the Nikkei and TOPIX as nothing more than a sign of the replacement of the most popular stocks with others as the new industrial revolution advances and relatively new companies push out older, more established ones. Just as in the United States, the gap is widening between the winners and losers of the new industrial revolution. In the TOPIX, large company stocks are performing poorly while the stocks of small companies are posting strong returns. Losers account for a large share of the TOPIX: banks, natural resources and energy, and electricity and other utilities. Key new industrial revolution sectors like information and communications, electric machinery, chemicals, pharmaceuticals and retail have a relatively small TOPIX weighting. In this environment, the superiority of the Nikkei Average, with its high weighting of growing companies that are driving the new industrial revolution, is likely to become even more pronounced.

(2) Analyzing the causes of the unprecedented profitability of Japanese companies – The shift from cutting fixed costs to boosting term of trade

Significant Growth of the marginal profit ratio is the primary cause

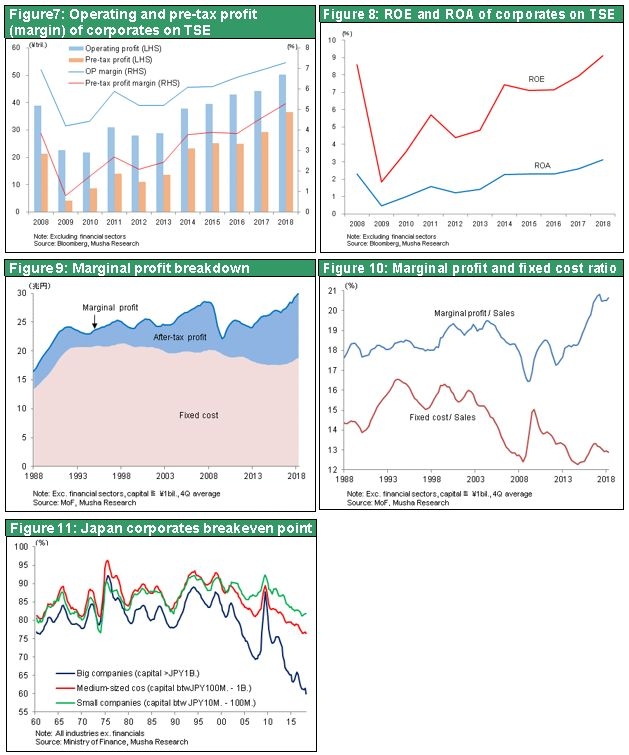

Earnings at Japanese companies are increasing on an unprecedented scale. One indication is the ordinary income to sales ratio, which was discussed earlier. The strength at companies listed on the Tokyo Stock Exchange (Figure 7 and strong profit margin in the Bank of Japan Tankan are another evidences. As earnings climb, the return on equity is moving higher as well. The ROE of all TSE-listed companies was a record-high 9.1% in fiscal 2017 (Figure 8).

What is the real force behind this improvement in profitability? Musha Research believes that the most important factor is a sudden increase in the marginal profit ratio. Higher profitability, in turn, is the result of a big shift in the business models of Japanese companies and the associated growth in earnings of their overseas operations. Changes in earnings of large companies (companies with capital of at least ¥1 billion in all industries except finance and insurance) demonstrate this point. As you can see in Figure 10, the upturn in the marginal profit ratio has been responsible for the big increase in profitability since the global financial crisis. On the other hand, restructuring and cost cutting have not been responsible for higher profitability during the past few years because fixed costs at Japanese companies stopped declining since fiscal 2013. After significantly reducing fixed costs, Japanese companies have rapidly boosted their marginal profit ratios since fiscal 2013. The result has been a dramatic drop in the break-even point. Since the 1960s, the break-even point at big companies in Japan was consistently about 80% of their current sales. But by fiscal 2017, this percentage had declined all the way to 60% (Figure 11).

Significant improvement of pricing power and boosting overseas earnings

The next question is how Japanese companies succeeded at raising their marginal profit ratios during the past few years. Two factors are primarily responsible. First is an enormous increase in the ability of Japanese companies to determine prices. Second is globalization, which helped boost earnings of operations outside Japan. As has been explained several times in Musha Research reports, increased price controlling power is the result of Japanese companies breaking away from price-based competition, a battle they could not win. Pursuing a strategy of specializing in areas where they have superior technologies and quality was a major reason. Japanese companies aimed to become the sole suppliers of products in targeted markets. Due to this strategy, Japanese companies are supplying many products and services that are available from very few other sources, if any.

Growing earnings in overseas operations is one more major reason for higher profitability. The ordinary income to sales ratio at Japanese manufacturers has improved from 5.5% in fiscal 2013 to 7.0% in fiscal 2017. During the same period, the operating margin increased from 4.1% to 5.1%. This difference shows that one-third of the increase in profit margins was the result of an improvement in non-operating income and expenses. Dividends from overseas subsidiaries were most likely the main reason. Figures in this companies earnings survey in Japan conducted by MOF they use only the performance of parent companies. As a result, the contribution to earnings of overseas operations appears in the form of dividend income from subsidiaries.

(3) Overseas operations are a huge profit center in the global business model created by Japanese companies

Activities of Japanese companies in other countries have been a major component of earnings. The following section examines the big picture created by the overseas business activity survey of the Ministry of Economy, Trade and Industry. The survey used questionnaires to collect data with excellent coverage and reliability from 6,500 companies. Unfortunately, the most recent survey results are for fiscal 2016, making it impossible to analyze directly the causes of the higher ordinary income to sales ratio in fiscal 2017 and 2018. However, the following analysis demonstrates with little doubt that overseas operations are a major cause for the recent improvement in profitability.

The switch from a defensive to an offensive posture for overseas strategy

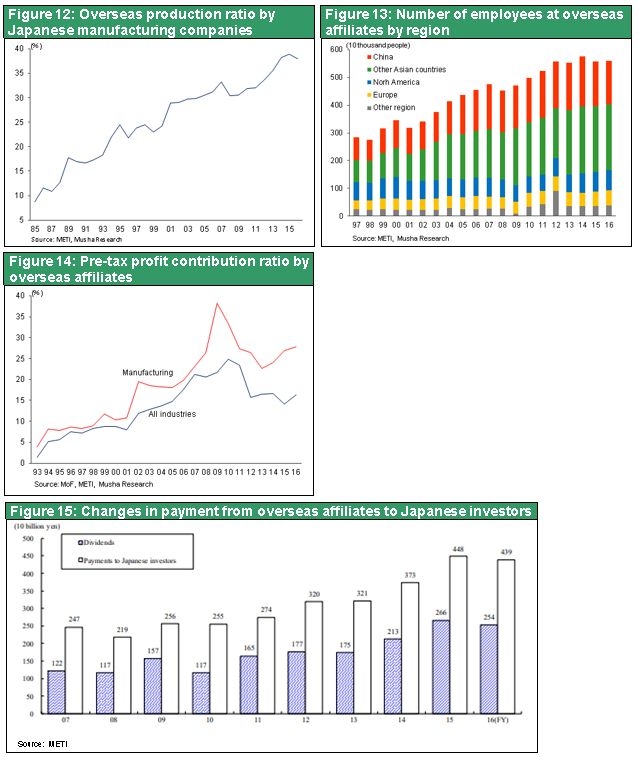

Manufacturers in Japan began to build overseas factories in the 1980s in response to trade friction and the yen’s strength. First was the start of operations in North America and Asia by manufacturers of electric machinery and automobiles. In Asia, Japanese companies wanted most of all to benefit from an inexpensive, high-quality workforce. All of these overseas investments were for defensive reasons. But the desire for low wages fell from 32% in 2007 to only 16% in 2016 as a reason for operating outside Japan. Instead, companies invested in other countries to capture market share and manufacture goods in the most suitable locations, which are both offensive reasons. As Figure 12 shows, Japan’s overseas production ratio (at companies with operations in other countries) has increased from the 10% level in the 1980s to the 20% level in the 1990s and is now approximately 40%. Furthermore, the overseas workforce of Japanese companies has been level during the current decade at around 5.5 million (Figure 13). Apparently, Japanese companies have largely finished measures to establish global supply chains.

Positioning overseas operations as a powerful sources of earnings

Avoiding risk, such as trade friction and a strong yen, was what first prompted Japanese companies to set up operations in other countries. Now, these operations are enormous profit centers. As Figure 14 shows, ordinary income outside Japan has increased significantly as a percentage of total ordinary income at Japanese manufacturers. This percentage has increased from only 3.8% for the manufacturing sector (and 1.4% for all industries) in 1993 to 10.3% (8.8%) in 2000, 18.1% (14.7%) in 2005, 27.4% (23.4%) in 2010 and 27.9% (16.2%) in 2016. Moreover, earnings within Japan include dividends, royalties and other payments received from overseas subsidiaries. In fiscal 2016, Japanese manufacturers received about ¥5,000 billion from overseas subsidiaries, including royalties of ¥2,200 billion and dividends of ¥2,600 billion. Since manufacturers in Japan had total ordinary income of ¥24,400 billion that year, their actual ordinary income within Japan was ¥19,500 billion after deducting this overseas income. In that year, the ordinary income of overseas subsidiaries of manufacturers was ¥6,700 billion. But this increases to ¥8,900 billion after adding back the royalties of ¥2,200 billion these subsidiaries paid to their parent companies in Japan. Consequently, for manufacturers, earnings at overseas subsidiaries are about half of parent company earnings in Japan. In addition, parent companies are obviously earning a margin on their sales to their subsidiaries. After taking these items into consideration, it is not an exaggeration to say that overseas operations account for about half of all earnings at manufacturers in Japan.

(4) No other country has achieved a business model shift on the same scale as in Japan

The internal division of international labor model created by Japan

No other country has achieved a transformation in its framework for creating value (business model) of the magnitude of the change that took place in Japan during the past two decades. Accomplishing this feat required a decisive shift involving the international division of labor. Until 2000, Japanese companies relied mainly on exports and competitive prices. But trade friction and a stronger yen destroyed the foundation for this business model. Around 2000, companies in Japan had to deal with the collapse of their value creation models, which was equivalent to a national crisis. Eventually, they achieved a comeback. The first reason was the decision to specialize in products with outstanding technologies and quality. Japanese companies became the sole suppliers of products, making them largely immune to price-based competition. The second reason was the establishment of global supply chains, including overseas factories that these companies assembled. Production processes were divided among countries in order to locate each activity in the best possible place. In this division of labor, parent companies in Japan served as organizers of these global activities. This business model advanced to a higher level in Japan than anywhere else.

There is ample evidence of the success of this business model.

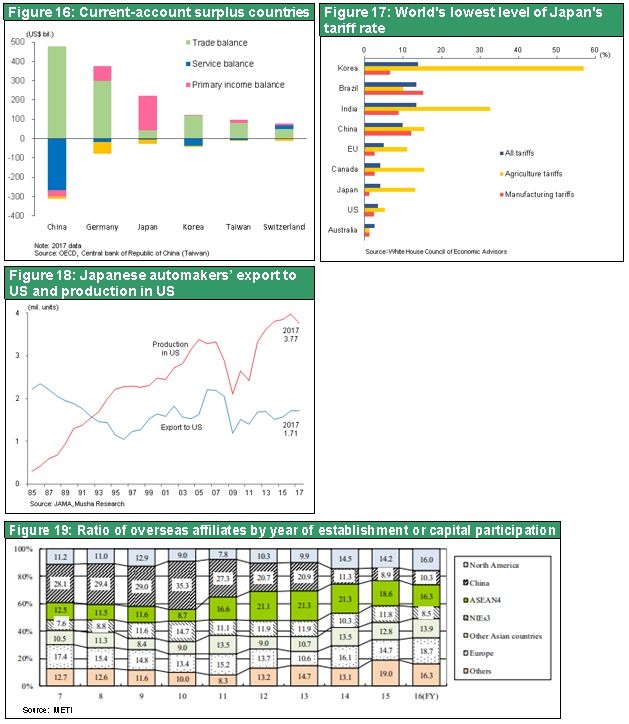

1) An enormous primary income surplus ➡ Japan has a very small trade surplus. Moreover, the positive primary income balance is responsible for the majority of the country’s current account surplus. Japan’s primary income surplus should be viewed favorably by other countries because it is the result of investments, jobs and other business activities outside Japan. On the other hand, a trade surplus is criticized as a sign that a country is stealing jobs from other countries. Japan’s huge primary income surplus therefore is proof that Japan is far ahead of other countries in terms of the high level of globalization of its companies and the strength of global supply chains. Eastern Asia has become a global base for the production of PCs, TVs, semiconductors, LCDs and other high-tech products. The internal division of international labor model of Japanese companies has played a critical role in the creation of these high-tech manufacturing bases in eastern Asia (Figure 16).

2) Japan has the world’s lowest manufacturing sector tariffs (Figure 17) ➡ President Trump says that his ultimate goal is no tariffs and no barriers. If this happens, Japan would probably be the world’s biggest beneficiary.

3) A complementary relationship with US industries ➡ At one time, Japan was a threat to the US manufacturing infrastructure in the semiconductor and electronics categories and other areas. This threat sparked US-Japan trade friction. But now, Japan has almost no competition with US companies regarding semiconductors, smartphones, internet infrastructure and platforms, aircraft, and other products in core industrial sectors. Instead, Japanese companies have established strong positions in the United States in market sectors where these companies have competitive advantages. Prime examples are automobiles, machinery, and high-tech materials and parts. Furthermore, Japanese automakers have greatly raised US production (Figure 18), creating a US automobile manufacturing cluster. Toyota has shared its manufacturing technology with GM (such as by establishing NUMMI) and provided considerable support to the US Big 3 automakers. As a result, US-Japan trade friction is inconceivable.

4) Quick measures to distance Japan from China ➡ Following the 2012 Senkaku Islands tension, Japan moved quickly to distance itself from China. Japanese companies established a division of manufacturing processes across many Asian countries. As of 2012, Japan accounted for 18% of all direct investments in China, ranking first in the world (excluding Hong Kong). Subsequently, Japan has significantly held back on investments in China as other countries increased their China investments. By 2017, direct investments in China had dropped by 50% and Japan ranked fourth with a 10% share . The speed of Japan’s reduction in its reliance on China is clearly evident in the steep downturn in China’s share of newly established overseas subsidiaries of Japanese companies (Figure 19).

Japanese companies survived the yen’s extreme appreciation

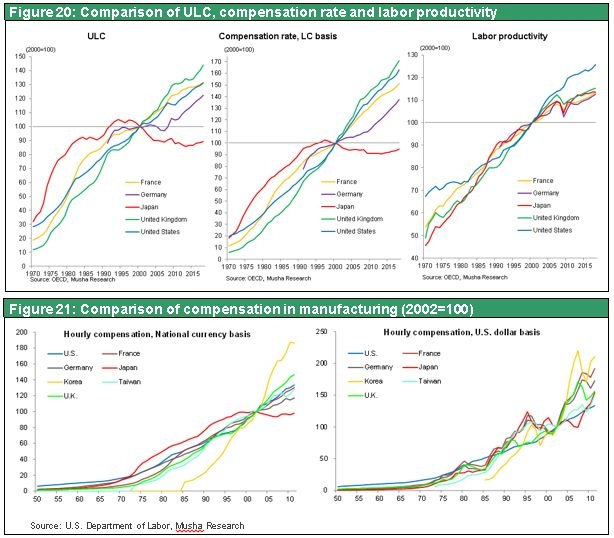

Figure 20 shows a comparison of the labor productivity, wages and unit labor cost in several major countries. Although Japan is about the same in terms of productivity, its unit labor cost has been held down greatly by the prolonged stagnation of wages. These numbers demonstrate that companies in Japan have slimmed down more than companies have anywhere else in the world. Surplus earnings produced by these efforts made it possible for Japanese companies to invest in their business model transformations even as they struggled with constantly decreasing prices of their products due to the yen’s strength and deflation. But this situation produced the negative side-effect of prolonged deflation.

But we still need to answer the question of why wages in Japan were beaten down for such a long time. Were workers in Japan forced to accept lower wages as a sacrifice? The cause is the yen’s strength. Figure 21 shows dollar-based wages in the manufacturing sectors of major countries. In Japan, yen-denominated wages were flat but, because of the yen’s appreciation, increased along with wages of other countries when converted into dollars. To remain price competitive, Japanese companies had no option other than to hold down wages. But keeping wages low alone was not enough to succeed, so Japanese companies were also forced to expand their overseas operations.

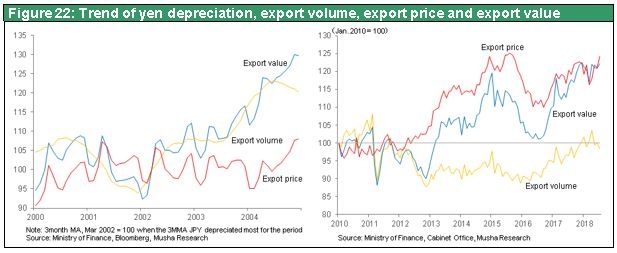

The business model transformation has changed the behavior of Japanese companies

Having accomplished a dramatic business model shift, Japanese companies are now exporting their products in a very different manner. When the yen started to weaken around 2000, companies responded by lowering their dollar-denominated prices. The result was growth in export volume but absolutely no increase in yen-denominated export prices. However, when the yen weakened starting in 2013, Japanese companies held their dollar-denominated export prices steady. This time, the result was a big increase in yen-denominated prices but no increase in dollar-denominated prices. As a result, the volume of exports increased only slightly because there was no change in the ability of Japanese companies to offer competitive prices. In the past, Japanese companies were skillful at using a weaker yen to increase exports. But now, Japanese companies have abandoned this type of behavior.