Jan 01, 2019

Strategy Bulletin Vol.217

The Age of Japanese Stocks Is Beginning under Dark Clouds

Happy New Year !

(1) A new age for Japanese stocks is beginning

Japan will be attracting considerable attention due to a number of high-profile events that include a new emperor in 2019 and the 2020 Tokyo Olympics. Expectations are high concerning the start of a new era for Japanese stocks. Most investors believe the long-term upward trend of stock prices will continue even though stock markets are still shrouded in fog. Is there a need to adopt a different view at this point? Stock markets will probably become stable once investors are confident that US monetary tightening and the US-China trade war will not stop the current period of economic expansion that has survived for many years.

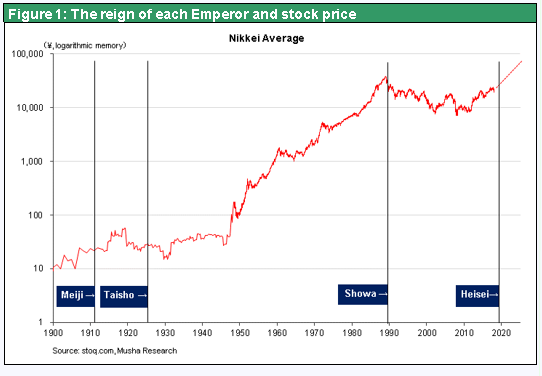

The Nikkei Average increased by approximately 400 times between 1949 and 1989, an average annual increase of 16%. In January 1989, when the Heisei Era started, the Nikkei Average was ¥30,000. Even if the Nikkei Average surges from the current ¥20,000 to ¥30,000 in 2019, it will be no higher that it was in 1989. In the United States on comparison, stock prices are about 10 times higher than in 1989. If Japanese stock prices move up an average of 10% every year during the reign of the next emperor, the Nikkei Average will reach the ¥100,000 level 15 years from now in 2034. This pace is not at all unreasonable because stock prices worldwide have generally increased at an annual rate of around 10% over the past four decades.

Japan’s foundation for future growth was created during the Heisei Era

On the surface, the Heisei Era was a period of numerous difficulties for Japan. However, this was also a time when Japan established superior positions in two areas that guarantee a bright future.

The first is superiority in the international division of labor. Japanese companies have used outstanding technologies and quality to become world’s sole suppliers in a large number of market sectors. The progression of the international division of labor has made countries increasingly dependent on each other. In this environment, acquiring skills no one else has is the key to success. As the only supplier or one of very few suppliers in a product category, a company can earn profits by charging higher prices. This invigorates a country’s living standards, economy and investments. The ability to establish these market positions is the primary reason for the very strong performance of Japanese companies nowadays.

The second is superiority involving Japan’s geopolitical position. As the US-China competition for global hegemony intensifies, it is becoming clear that the outcome will be decided by which country Japan backs. Japan is more important for the United States than traditional US allies like Britain and Israel. A strong Japanese economy that can go up against China is directly linked to the national interests of the United States. The geopolitical environment has been the decisive factor concerning Japan’s periods of prosperity and decline in her modern history. Japan’s geopolitical position has always depended on the nature of her relationship with the world’s most powerful country. This position has never been more advantageous than it is today.

The popularity of Japanese stocks is very likely to increase in 2019. One reason is the outlook for consistently strong earnings at Japanese companies, which have established a highly profitable business model. Another reason is irrefutable signs of the end of deflation, which was strongly linked to real estate prices. As a result, an enormous shift in savings will probably start to take place as people abandon bank deposits and government bonds yielding nothing and put their money in the stock market. Growing demand for Japan’s technologies and products is one more reason. As the US-China cold war continues, Japan will be attracting increasing attention due to its vital high-tech core technologies, new-energy vehicle expertise, high-quality consumer products, popular destinations for tourism and other attributes. A fourth reason for the popularity of Japanese stocks is the financial soundness of Japanese companies. This soundness will become increasingly valuable as the current environment of monetary easing changes and international liquidity becomes tighter. Financial soundness gives Japanese companies considerable flexibility concerning M&A deals, R&D expenditures, stock buybacks and other activities. Japanese companies have been criticized for the low ROEs that result from having balance sheets with the smallest leverage in the world. But now this financial soundness is likely to be a reason for investors to become more interested in Japanese stocks.

(2) It’s still too soon to be pessimistic about the economy

Only two events have a potential magnitude large enough to end the ongoing longest period of economic expansion in the postwar era: (1) the US-China trade war and (2) US monetary tightening. But it is still too soon to adopt a pessimistic view of the economy.

A US-China compromise will be achieved eventually

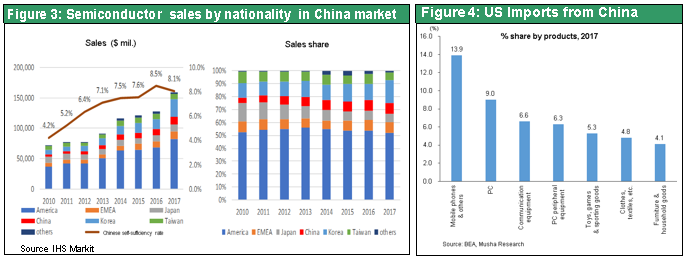

All five US demands to China involve unfair activities. Most people believe additional US tariffs can be avoided because China’s only option is to accede to these demands. China meets only 8% of its semiconductor demand with domestic production and buys most of its semiconductors from US companies. In turn, the United States relies on China for the majority of its imports of smartphones, PCs and other high-tech products. Neither country can destroy this relationship of mutual dependence. To exert pressure on China, the United States has no choice other than to use the high-tech sector in a selective manner. Consequently, a full-scale confrontation will probably be avoided.

Investments in China by multinational corporations are falling quickly. From a political standpoint, the administration of President Xi Jinping needs to stop this decline and concentrate on propping up the economy. Debt at private-sector companies in China is climbing, procuring dollars has become difficult and there are other challenges. Nevertheless, China still has considerable leeway for more public-sector spending and monetary easing.

For these reasons, the US-China trade war is very unlikely to trigger a global recession for the time being. However, in a worst-case scenario as we will discuss later, the United States may use various measures such as the 2019 National Defense Authorization Act to prohibit dollar-denominated transactions at Huawei and other Chinese companies that are viewed as targets. This step could cause the immediate collapse of these Chinese companies and start a global financial crisis. But the Trump administration is not very likely to threaten China to this extent.

No worries about liquidity – The Fed has enormous discretionary power

Rising US interest rates and monetary tightening by the Fed are another source of concern. But the Fed has considerable freedom to determine its own actions, so there is no need to worry about Fed doing anything that would harm the economy. A speech by Fed chairman Jerome Powell in early December made it clear that the end of this cycle of interest rate hikes is not far away. The reason is the lack of any acceleration of inflation. Although wages continue to climb at an annual rate of almost 3%, rising productivity means that there is very little pressure on companies to boost prices. The current US environment of economic strength, low inflation and low interest rates is too good to true and even difficult to believe. However, this situation is precisely what has increased the Fed’s discretionary power so dramatically.

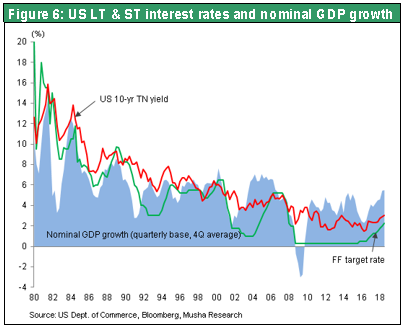

Stock prices fell sharply following the December interest rate hike because investors had expected a monetary policy shift. Falling stock prices caused downturns in interest rates and the dollar. The Wall Street Journal has been a consistent critic of quantitative easing. But in an editorial immediately before the December FOMC meeting, this newspaper reversed its position by publishing an editorial advocating a switch to a dovish monetary stance. In a sense, this was like creating a problem in order to receive credit for the solution. Mr. Powell instead betrayed these dovish expectations by demonstrating his confidence in the economy. But this is not significant. With inflation under control, the Fed can take any action that is needed anyway. For example, the Fed can stop raising interest rates, start lowering interest rates, suspend quantitative tightening (downsizing its balance sheet), or even restart quantitative easing (return to balance sheet growth). Even though interest rates have come up, the long-term interest rate of about 3% is still only half of the US nominal economic growth rate of 6%. This is well below the level where interest rates would start weighing on economic growth. Therefore, the conditions do not exist for a deterioration of the credit cycle, which is a possibility that worries investors. If you look at Chart 6 the level of interest rates are very low compare with nominal GDP now. In the past recessions in 1990-1991, 2001 and 2007-2009, short term interest rates were always above the level of nominal GDP growth rates.

Stock markets will once again test the upside in 2019

Early in 2019, stock prices will probably settle down and the dollar will slowly strengthen as uncertainty about the US-China trade war dissipates. Signs of weakness in US economic indicators are starting to appear, in part because of the drop in stock prices. To stimulate animal spirits, the Fed may temporarily stop interest rate hikes, balance sheet downsizing and other monetary tightening measures. Taking these actions may briefly cause the dollar to weaken. However, the dollar would probably start appreciating again as stock investors interpret the Fed’s actions as a signal to increase risk exposure.

Signs pointing to a long-term strengthening of the dollar are becoming even more pronounced

Investors should pay attention to two forces behind the dollar’s long-term appreciation. First, the dollar’s position as a vital currency for global business transactions is increasing steadily. Iran, North Korea and eventually China are likely to encounter serious problems involving the dollar. If a country confronts the United States and ends up being prohibited from using the dollar, its economy will quickly shrink. The entire world is aware of this situation and the Trump administration is making frequent use of the dollar’s clout in its relations with other countries. Second, the dollar is becoming stronger in practical terms as well because of highly competitive US industries and the improving US current account balance. Demand for the dollar is backed by the currency’s growing share of international credit and investments. Consequently, upward pressure on US interest rates from the growing budget deficit will probably not be significant.

(3) Key issues are US-China cold war-related risk and China’s dollar procurement difficulties

Vice President Mike Pence’s October 4th speech signaled the start of a new cold war between the United States and China. This war is probably irreversible. The 2019 National Defense Authorization Act that became law in August 2018 is the primary US weapon. The United States has made clear its intention to contain and shut down Chinese flag ship companies. In particular, investors should keep in mind the possibility that this new law will make it difficult for Chinese companies to procure dollars.

Enormous potential for sanctions

The 2019 National Defense Authorization Act is significant in two respects. One is the unification of restrictions on foreign investments (Foreign Investment Risk Review Modernization Act) and restrictions on exports (Export Control Act). The other is the ability to prohibit designated companies (the five “problem” Chinese companies and companies that are believed to be owned, controlled or affiliated with the Chinese government) from engaging in transactions (providing substantial goods and services) with US government agencies. Investors are most concerned about the enormous scale of the authority granted by prohibiting these transactions. First, the US government has complete discretion to impose sanctions on companies and the number of sanctioned companies could continue to increase. Second, companies that do business with sanctioned companies will be subject to secondary sanctions. Third, there is no limit on expansion of the breadth of these sanctions. Companies that are sanctioned will ultimately be cut off from the global business community.

*Designated companies

(1) Huawei (2) ZTE (3) Hytera Communications (communications equipment) (4) Hangzhou Hikvision Digital Technology (world’s largest surveillance camera manufacturer, partially government owned) (5) Zhejiang Dahua Technology (private-sector manufacturer of surveillance cameras) (6) Companies determined to be owned/controlled by or affiliated with the Chinese government (Ministry of National Defense, etc.)

Secondary sanctions imposed for doing business with a designated company like Huawei also result in being shut out of transactions (providing substantial goods and services) with US government agencies. Consequently, US sanctions on Chinese companies prevent even companies in other countries from doing business with a sanctioned company.

The final step: No dollar-denominated payments

Sanctions make it impossible to have a relationship with a broad range of US government agencies. In some cases, a sanctioned company may even be blocked from transactions with US banks and other financial institutions. This would make it impossible to submit or receive payments in dollars. The Specially Designated Nationals and Blocked Persons List (SDN List) is published by the US Treasury Department to designate individuals and other entities that are prohibited from dealing with US individuals and other entities. Restrictions include transactions with US and international financial institutions, foreign exchange transactions (including sending and receiving dollars), and the freezing of assets in the United States. In a worst case scenario companies designated by the 2019 National Defense Authorization Act could be subject to the same sanctions that are imposed on those designated on the SDN List.

The 2019 National Defense Authorization Act will be enacted in two stages. Blocking designated companies from US government agency transactions starts on August 13, 2019. Blocking companies that do business with a designated company from US government agency transactions starts on August 13, 2020.

Banks are cutting off ties with Huawei

HSBC ended its relationship with Huawei and this move was followed by the decision of Standard Chartered to stop doing business with Huawei. Only Citigroup is still serving Huawei. But the Wall Street Journal reported on December 21 that Citigroup is closely monitoring the actions of regulatory authorities.

Fund procurement activity is high at Chinese companies due to expectations for increasing difficulty involving the procurement of dollars. One result is a big upturn in IPOs in the United States. In 2018, there were 33 IPOs by Chinese companies in the United States that procured a total of $9 billion, according to the Financial Times (December 27), well above the 17 IPOs in 2017. Furthermore, sales of real estate and other US assets by Chinese investors are increasing. According to the Wall Street Journal (December 5), in the third quarter of 2018, sales of US real estate by Chinese investors totaled $1,050 million, far more than purchases of $230 million. Chinese companies appear to have started procuring dollars in anticipation of upcoming problems. As the US-China trade war rages on, increasing worries about procuring dollars may be one reason for President Trump’s criticism of Fed chairman Jerome Powell’s decision to hike interest rates.

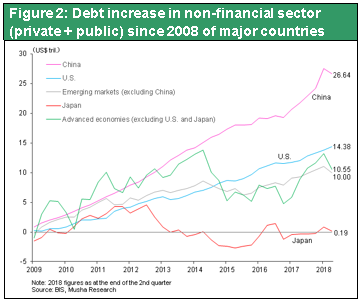

Many people are worried about the possibility that the growth of debt worldwide will be the cause of the next downturn of the credit cycle. As you can see in Figure 2, China is responsible for a large share of the increase in debt. This creates the risk of a global recession triggered by the collapse of a Chinese credit bubble. Investors need to keep an eye on upcoming events in China to see if dollar procurement problems become even more serious.