Jun 10, 2019

Strategy Bulletin Vol.226

The Powell Put and the Commitment to Stock Prices

- What if a powerful stock market rally is just about to begin?

(1) The Fed chairman effectively stated that stock prices are the priority

Activation of the Powell Put places stocks at a big turning point

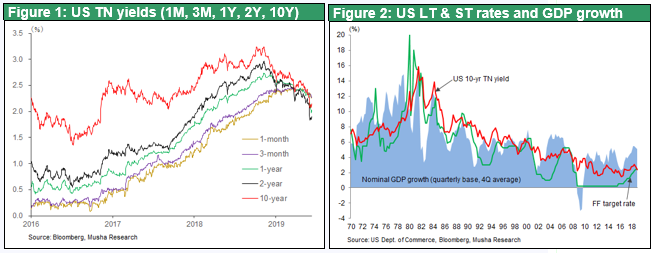

Once again, a speech by Fed Chairman Jerome Powell amid a sharp stock market downturn has sparked a dramatic turnaround. Mr. Powell talked about a flexible response to trade friction and the possibility of a preventive interest rate cut. Clearly, the chairman is the guardian angel of the stock market. Interest rates that were already moving down began to plummet. The yield curve is now completely inverted. On June 7, U.S. Treasuries were yielding 2.31% for one month, 2.28% for three months, 2.02% for one year, 1.85% for two years, 1.81% for three years and 2.08% for ten years. At these levels, interest rates have baked in three interest rate reductions within a year.

For some time now, Musha Research has been sending the same message to investors. “It is quite evident that the Fed no longer needs to hike interest rates because inflation is not a problem. Right now, the Fed is in a position where it can do anything that is needed to support economic growth and stock prices. The Fed could even go back to quantitative easing or start lowering interest rates. Taking either of these actions would immediately energize the stock market. The Fed has this flexibility because prices are under control. Some people are critical of the Fed’s excessive support of financial markets. They think this creates a moral hazard and could produce an asset bubble. However, the fact that inflation is not a problem signifies that there is still slack on the supply side. During this economic phase, monetary policies that boost demand are not a mistake. Recent events have proven that policies to increase demand are correct. We have witnessed a dramatic stock market pullback that was followed by a shift in the Fed’s stance and then a powerful stock market recovery.” (Strategy Bulletin Vol. 218 (January 22, 2019) and Vol. 219 (February 4, 2019)) Subsequent events have demonstrated that this message was precisely on target.

The Fed has started viewing QE as the new monetary regime

This most recent statement by Mr. Powell may have even more historical significance than in the past. The key point here is that quantitative easing and forward guidance, which used to be used only for a crisis, have become two of the main policy options. Mr. Powell believes that the biggest problem for a central bank is the risk of reaching the effective lower bound on interest rates (where rates can no longer be reduced) as inflation becomes lower and lower. At that point, the Fed would have to use quantitative easing and other so-called unconventional monetary actions. However, Mr. Powell believes that it may be time to retire the term “unconventional” for tools that were used only in a crisis.

The possibility of the inability to enact effective policies in response to the next economic downturn because interest rates are at the effective lower bound is one reason for the concerns of bears. But the situation is not at all this bad because quantitative easing (propping up asset prices) would still be an option. We have finally reached the point where there is no longer any need for balance sheet downsizing simply for the sake of “normalization.”

Quantitative easing was inevitable – The fundamental shift in US finance

Dramatic changes are taking place in the financial characteristics of industrialized countries. First is the emergence of an apparently permanent surplus of capital. Second is the new industrial revolution. Growth in earnings coupled with falling prices of equipment have produced a remarkable increase in the ability of companies to finance their own activities. Many companies have very large cash flows because of strong earnings, a surplus of depreciation and small requirements for investments. In the past, the financial sector functioned as an intermediary for channeling household savings to companies for funding their investments (the commercial bank business model). Now, this model has come to a complete end. Recirculating corporate earnings has become the primary role of the new financial business model. This shift is clearly visible in the following US capital flows during 2018.

- Private depository institutions in the United States recorded growth of $591.2 billion in deposits and $566.5 billion in loans during 2018. Households received many of these loans, primarily as mortgages and consumer loans.

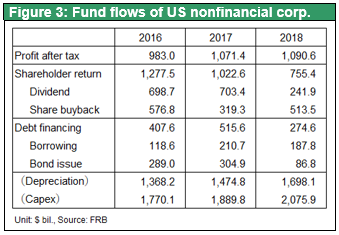

- In the non-financial corporate sector, after tax income in 2018 was $1,090.6 billion, dividends payments were $241.9 billion, and stock repurchases were $513.5 billion. Earnings returned to shareholders totaled $755.4 billion, which was 69% of after tax income. Companies added debt of only $274.6 billion, consisting of $187.8 billion of loans and $86.8 billion of bonds. Consequently, debt was just one-third of shareholder distributions. Additional debt was 31.9% of shareholder distributions in 2016 ($407.6 billion vs. $1,277.5 billion) and 50.4% in 2017 ($515.6 billion vs. $1,022.6 billion). These numbers show that bank loans are no longer a meaningful part of corporate finance.

- Personal savings in the United States totaled $1,043.4 billion in 2018. During the year, there were increases of $702.2 billion in deposits and money market funds, $684.5 billion in bonds (mainly Treasuries), $127.0 billion in stocks and equity mutual funds, and $312.6 billion in pension fund assets. Household debt increased $488.2 billion during 2018, including increases of $284.8 billion in mortgages and $187.0 billion in consumer credit.

A dramatic shift in monetary adjustment methods, too

When companies and individuals relied primarily on bank loans for financing, the Fed could hold down credit creation by altering interest rates on its loans to banks. Today, this monetary adjustment method is no longer valid. This is particularly true in Japan, where banks are having difficulty finding borrowers.

The goal of monetary policy as well as the mission of the Fed is to maintain a proper level of prices while maximizing employment. This is often called the dual mandate. Basically, the objective is achieving the highest possible growth rate within the range where this growth is sustainable. Controlling the total amount of credit (purchasing power) is how this can be accomplished. In prior years, the Fed controlled credit by using interest rates to influence the volume of bank loans. But the days when the banking system created credit have come to an end. Credit is generated today mainly by rising prices of assets (especially stocks). This is why policies that directly affect asset prices and quantitative easing through enormous money supply growth have become vital monetary policy tools. All of these points lead to the conclusion that quantitative easing is a monetary regime with the goal of achieving the most suitable level of asset prices (the level where the highest prices can be maintained).

The transformation of the mechanism for creating money

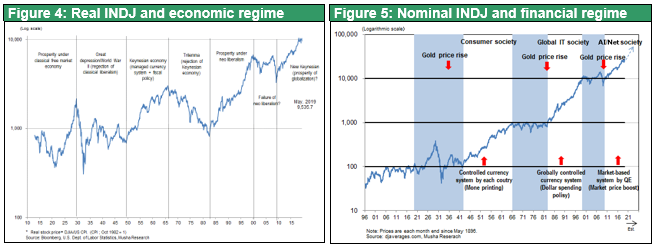

Quantitative easing is the new monetary regime because it is an entirely new scheme for increasing the money supply. Figures 4 and 5, which cover the past 100 years, clearly show how changes in the monetary regime (the mechanism for increasing the money supply) are linked to the health of the US economy and the Dow Jones Industrial Average. Figure 4 shows the real (inflation adjusted) DJIA, which allows using the value of stocks as an indicator of purchasing power. During the past century, there were three major upswings of the real DJIA and we are now in the midst of the fourth. The previous three are:

- 1910 to 1920s (bull market during a classical free economy under the gold standard)

- 1950 to 1960s (bull market during a Keynesian economic environment in which the management of currencies by individual countries resulted in each country printing more money

- 1980 to 1990s (bull market during the period of neoliberalism (laissez-faire economics) as a global currency management infrastructure resulted in the growth of dollar holdings worldwide)

- The current real DJIA bull market started in 2010. This can be viewed as a period of a market-driven economy in which quantitative easing, a new framework for increasing the money supply, and other measures are used to print more money up to the maximum level that stock and other financial markets can tolerate. Perhaps this will become a “new global Keynesian regime” in which economies are fueled by demand creation by governments. The world is moving toward an era where demand creation using monetary easing and fiscal measures will be both essential and appropriate. This will be a period that requires policies like Japan’s Abenomics and President Trump’s macroeconomic initiatives and justifies the validity of these policies. On the other hand, Europe (the EU) is experiencing difficulties because of the stubborn insistence on fiscally responsible budgets.

(2) What happens if President Trump’s policies are successful?

Tariff pressure on Mexico had a good outcome

Apparently, stock price movements worldwide have assumed that President Trump’s policies will fail. We must therefore also think about what would happen if instead these policies are successful. Tariff hikes are like bullying. But this threat had a good ending due to Mexico’s commitment to help lower the number of people trying to enter the United States illegally. Trade talks with China are also likely to have a similar outcome. As stated in the previous Strategy Bulletin, the cost of a continuation of trade friction will be enormous for China because China has been enjoying almost all of the benefits of its trade relations with the United States. Eventually, China will no longer be able to bear the cost of trade friction. Giving in to US demands and reaching an agreement are probably China’s only options.

Excellent prospects for a US-China agreement due to Chinese concessions

When he visited the starting point of the Long March on May 20, President Xi Jinping told the people of China that they must embark on a new Long March. Chinese media reports interpreted this statement as the president’s resolve to resist US pressure. In fact, the statement had the opposite meaning. The Great March was a temporary retreat in response to extreme adversity followed by a switch to a war of attrition and the resumption of attacks. The president probably recalled the Long March in order to prepare for the justification of a temporary retreat. At the China-Russia summit meeting, President Putin was extremely critical of the United States while President Xi Jinping stated that President Trump is a friend and indicated that trade talks will continue. On the US side, Treasury Secretary Mnuchin has hinted that sanctions on Huawei may be eased if there is progress with trade talks. These developments should be regarded as signs that the United States and China are both seeking a middle ground for an agreement.

At this time, the best scenario from the standpoint of the global economy concerning US-China trade friction is still for an agreement to be reached when the US and Chinese presidents meet at the G20 Osaka Summit at the end of June.

The next economic upturn is on the horizon

Concessions by China will probably be followed by an economic upturn. An agreement could have the effect of increasing demand. Capital expenditures in China came to a halt late in 2018 because the trade war made it impossible to determine a reliable economic outlook. But now there is almost no possibility of declines in US and Chinese final demand, which has been a source of concern. As a result, there is an increasing likelihood of tight supplies of goods in the future because of sluggish supply side growth caused by this temporary suspension of capital expenditures.

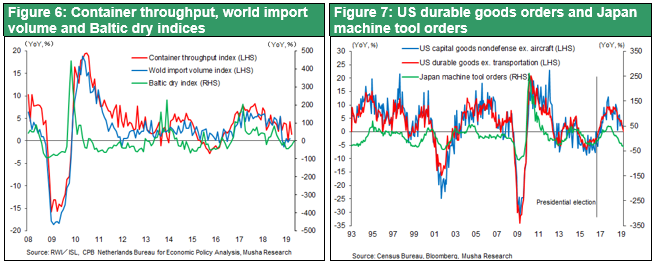

Stock prices of US semiconductor companies (PHLX Semiconductor Index), which have a reliance of more than 50% on China, have increased rapidly in recent years. Prices have remained high even after this index reached its historical peak at April 2019 probably because of the likelihood of tight supplies of semiconductors. If the US and Chinese economies start to improve, the economies of countries like Japan, Germany and Korea that export goods to these two countries will also become stronger. US-China trade tensions have severely impacted Japanese manufacturers of electronic components. Nevertheless, according to a survey by the Electronic Device Industry News, the capital expenditures of Japan’s 30 primary electronic component companies increased from ¥895.8 billion in 2017 to ¥939.4 billion in 2018 (+4.9%). Furthermore, these companies plan on raising these expenditures by an even higher 7.1% in 2019 to ¥1,006 billion, a clear indication of the strength of market conditions. Consequently, in terms of the economic mini cycle, the first bottom was in early 2016 and the first peak was in early 2018, which means there is good reason to expect the next bottom to occur in the middle of 2019 followed by an upturn toward the next peak.

Even a hard Brexit would have only a small negative impact

When President Trump visited the UK shortly after Prime Minister May announced her resignation, he made a statement supporting former Foreign Minister Boris Johnson and other backers of a hard Brexit. But at this point, financial markets have generally factored in the possibility of the no-deal Brexit that everyone fears. As a result, this would no longer be a negative surprise. In fact, leaving the EU with no deal would instead create visibility regarding Britain’s post-EU strategy and may create even bigger expectations among investors.

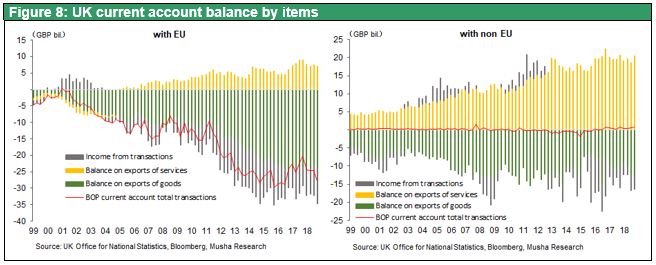

Brexit has always posed a greater problem for the EU than for Britain. As you can see in Figures 8, Britain has an enormous current account deficit with the EU because of a very large trade deficit. But excluding the EU, Britain has no current account deficit because of a huge trade surplus in the service sector. Britain is one of the EU’s best customers. Moreover, Britain’s economy is the world’s most advanced regarding the shift from industry to services. Britain accounts for slightly less than 3% of the world’s exports of goods but 7% of service exports, second only to the United States. Furthermore, manufacturing accounts for only 8% of all jobs in Britain, the lowest ratio among all affluent countries. Also significant is that bank assets in Britain are 800% of GDP, by far the highest in the world. There is also reason to say that Britain has the world’s most open economy because direct foreign investments are 70% of GDP, the highest in the world. This percentage is 42% in Germany, 28% in the United States and 16% in Japan. Another sign of this openness is that foreign ownership of companies listed in Britain is 54%, again the highest in the world.

Britain, along with the United States, is home to key components of globalization: capitalism, the market economy, democracy, the English language, the rule of law and business protocols. In sum, Britain, with the United States, is a pillar of the world order, the leader of the Commonwealth of Nations and a critical element of a multitude of international relationships. Brexit is unlikely to alter Britain’s position as a global center for international finance and the service sector. There may even be a positive effect as leaving the EU gives Britain the freedom to forge new ties, such as an EPA with Japan.

For these reasons, investors should probably expect any market turmoil associated with Brexit to end quickly.

The biggest upswing is likely to happen in Japan

Japanese stocks have not done well in 2018 and 2019. Investors have sold off stocks in Japan more than in any other country amid concerns about the US-China trade war and the possibility of a global recession. The United States and China appear to be implementing financial policies that target stock prices. But Japan is unable to enact such policies, as is demonstrated by the continuation of consumption tax hikes. This policy deadlock situation has caused global investors to shun investments in Japan. However, if the global economy starts to stage an upturn, the biggest stock movement in the world is likely to take place in Japan. This is because Japanese stocks have the world’s highest volatility. One reason is the big fluctuations in the earnings of Japanese companies due to the large share of specialization in capital goods and producers’ goods that have very high price volatility. Another reason is the close link between Japanese stock prices and foreign exchange rates as the yen weakens when times are good and appreciates when the economy is weak. A third reason for high volatility is that foreigners account for 70% of stock market trading volume in Japan. Stock prices are significantly influenced by speculative transactions involving futures.

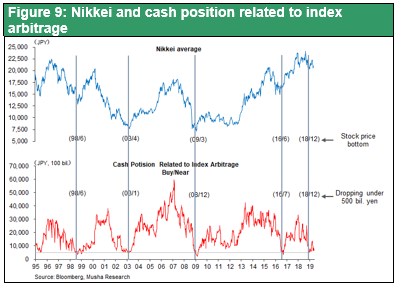

On the other hand, precisely because of this volatility, Japanese stocks have the potential of staging a powerful rally once investors switch to a risk-on stance. Stock prices in Japan are also backed up by the current global stock market rally and the new mood in Japan created by the start of the Reiwa Era. All these factors point to the imminent start of a big upswing in Japanese stock prices. The level of unsettled long arbitrage positions (Figure 9) shows that supply-demand dynamics for Japanese stocks should remain favorable. The conclusion is that Japan may very well witness a stock market rally toward 2020 that goes far beyond the consensus outlook.