Nov 06, 2020

Strategy Bulletin Vol.264

Speculation strengthens in New York; Japanese stocks relatively more stable

- Will next year be the year that Japanese stocks take center stage?

US stocks are increasingly volatile

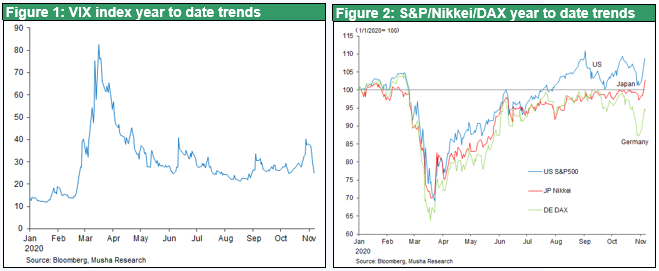

Stocks have fluctuated wildly around the time of the US election. Market volatility has increased on the back of uncertainty such as the indefinite outcome of the election, with Trump refusing to readily admit defeat and plans to take the dispute to court.

However, it is important to note that volatility in US stocks has increased since the COVID-19 crisis and the market has become more speculative irrespective of the election. As Figure 1 shows, volatility has remained high even though US stocks (S&P 500) have risen more than 60% to an all-time high after bottoming out on March 23.

Why is volatility so high? In addition to the huge surplus of funds, high volatility can be attributed to the increase in speculative fever under the ultra-easy monetary policy and low interest rate policy. Specifically, excess returns on stocks (i.e., the risk premium) have increased due to the decline in US long-term interest rates and zero short-term interest rates, which has heightened the desire to raise funds at zero interest rates to invest in stocks.

Increase in excess returns on stocks due to the persistence of zero interest rates ➡ increase in volatility cost

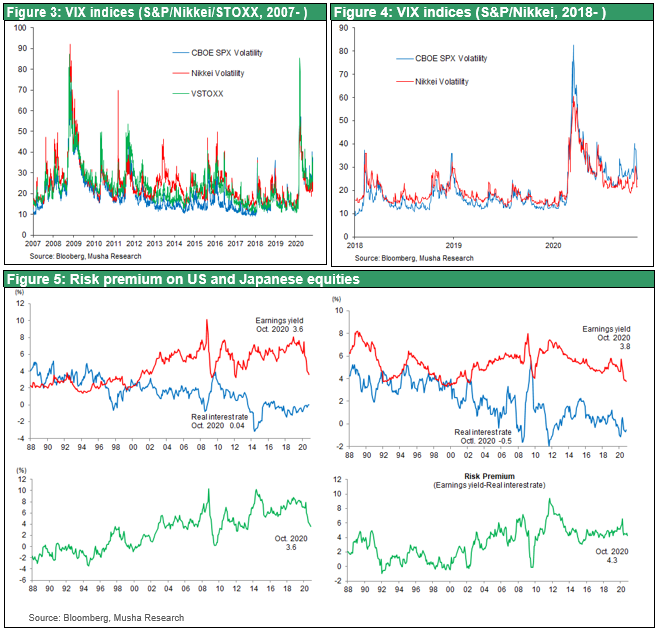

In 2019, the excess return on US stocks relative to US treasuries was 3.0%. However, the average excess returns jumped to 3.9% for March-October 2020 due to the sharp drop in interest rates, making leveraged investments more attractive.

2019 Average US stock returns (5.2%) > Treasury yields (2.2%) Excess return ER=3.0%

Mar-Octr 2020 US stock returns (4.6%) > Treasury yields (0.7%) ER=3.9%

This excess return on stocks relative to bonds is offset by the volatility costs for stocks. If interest rates are low and excess returns are high, investors will increase their leverage to pursue greater investment outcomes. The high returns of such highly leveraged portfolios are lost by the occasional market surge. A mechanism exists whereby the excess returns present in stocks are redistributed to various market participants, financial institutions, and investors through this volatility cost. The rough price movements in US stocks can be attributed to these substantially higher excess returns.

Volatility in Japanese stocks has fallen

In contrast to US stocks, volatility in Japanese stocks has fallen significantly, making Japan a low-risk market. Movement in Japanese stocks were stuck at 3% in September-October 2020, compared to the 10% movement in US stocks. The Japanese market was the most speculative market throughout the 2010s, with volatility so high that investors such as individuals found it difficult to approach. Foreign investors, who accounted for 70% of Japanese stock trading, were mainly speculative (trading) players. This high volatility in Japanese stocks was due to the extremely high excess returns for Japanese stocks because of the abnormally low interest rates from the 2000s. The speculative appeal was very high.

However, a sense of calm appears to have been restored to the Japanese market as these speculators migrated to the New York markets. Figure 3 shows the trend of the trilateral VIX indices (S&P, NKY, STOXX) and highlights how the Japanese market has calmed down.

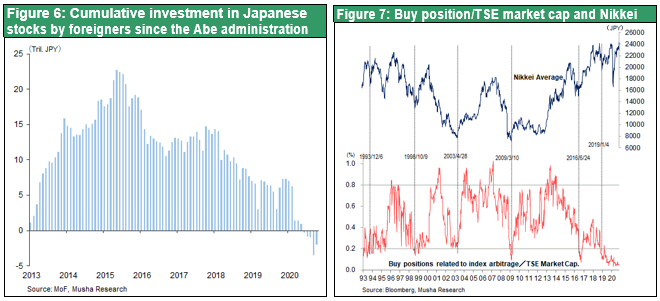

Contrary to the migration of short-term speculators from Japanese stocks to US stocks, long-term investors have started to buy Japanese stocks. Foreign investors bought more than 23 trillion yen in Japanese stocks since 2013 due to their assessment of Abenomics, selling everything at the beginning of 2020, but becoming net buyers from October. This is attributed to factors such as (1) the small number of COVID-19 cases and the expectations that normalization of the economy will be accelerated, (2) the expectations that the recovery in China will benefit the results of global companies, (3) the assessment of the impact of the Suga reform minded administration, and (4) the inspiration provided by Warren Buffett's investment in trading company stocks. As shown in Figure 7, the supply-demand balance for Japanese stocks is extremely favorable from a speculative standpoint.

2021, the year of the Olympic Games, is likely to be a year of accelerated economic growth in Japan. There are several reasons for this, including (1) pent-up demand (liberating desire and money), (2) accelerated innovation, and (3) policy support (fiscal stimulus and monetary easing). As the global economy expands, investment funds will be further concentrated in Japanese stocks, which have a high weighting of economically sensitive sectors.

The impact of the US presidential election and the feelings about the US economy and market uncertainty may not ease

The US economy and stocks, on the other hand, may need to be on alert for the next few months. There are a number of issues to be overcome such as (1) Trump's refusal to admit defeat, (2) even if Biden is confirmed as president, the government being too weak to find a direction; and (3) concerns about the implementation of anti-Wall Street policies such as corporate tax hikes and a capital gains tax. There are also concerns that the government may be delayed in passing a fiscal package to deal with the spread of the COVID-19 pandemic. However, a major correction is likely after his inauguration speech on January 20.

Biden is a moderate, and I think he will be able to cut his teeth on market-friendly policies. The Senate is also forecast to have a Republican majority, so anti-Wall Street policies such as corporate tax hikes and a capital gains tax are likely to be shelved.

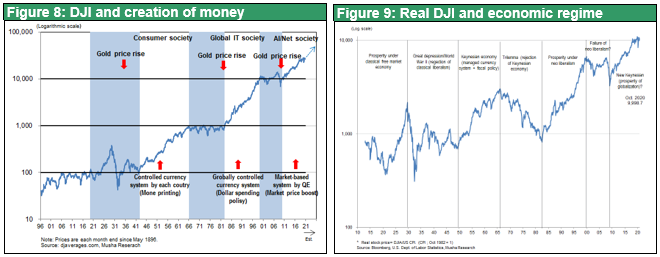

We could see a change in the policy regime towards big government under Biden. He could put forward a very different growth agenda than Trump, including environmental, tax and significant spending, changes in forms of employment, and international cooperation. Many of these are also due to the demands of the times and would be positive for stock prices over the long term, but the market will be wary of game changing from Mr. Trump and will most likely look at specific measures. However, the long-term upward trend in US stocks, as shown in Figures 8 and 9, is likely to remain intact.