Mar 04, 2022

Strategy Bulletin Vol.300

Putin's invasion of Ukraine, the beginning of Russia's decline?

This is an English version of a Japanese report written on March 4.

Putin's stumble in the beginning of the war

A week after Russia launched its military advance against Ukraine, ceasefire talks are being held in Belarus by both delegations. Although it is dangerous to judge the ever-changing war situation, it seems that the plan to win the initial battle with a lightning attack and force the Ukrainian side to accept Russia's demands: 1) demilitarization and neutralization, and 2) transfer of sovereignty over the Crimean Peninsula, is not going well. The establishment of a puppet government is now more difficult.

Miscalculations are Ukraine's morale and Germany's policy reversal

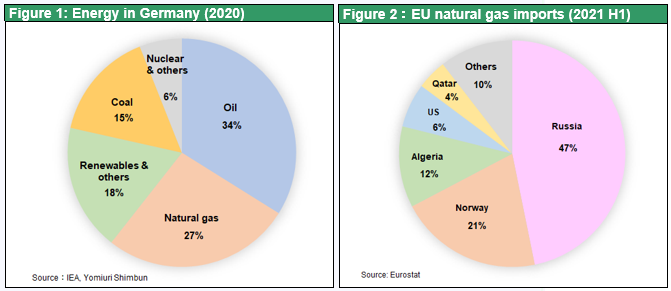

The two main reasons for the miscalculation are the high morale and strong resistance on the Ukrainian side and the growing criticism of Russia by international public opinion. president Zelensky's heroic resistance and the growing patriotism of the citizens, which are being communicated worldwide via social networking services, have inspired international public opinion, creating an atmosphere that could be called a joint front of criticism against Russia. Noteworthy among these is the major policy turn of the German Scholz administration, the leader of the EU. At a special session of the German parliament on February 28, immediately after Russia's invasion of Ukraine, a budget of 100 billion euros for military modernization and an increase in the military budget (1.5% to 2% of GDP) were announced. The shelving of the Nord Stream 2 pipeline on the North Sea route was also put forward. The Greens also agreed to the exclusion of Russia from the international payment system SWIFT, aid to Ukraine in the form of missiles and armored vehicles, the building of coal and natural gas reserves, and the construction of two LNG terminals to receive LNG from Qatar and the U.S. The extension of the operation of nuclear power plants that were scheduled to be phased out in 2022 and their abolition were also proposed. The restart of nuclear power plants may also be on the chopping block.

Four possibilities, all on Vladimir Putin

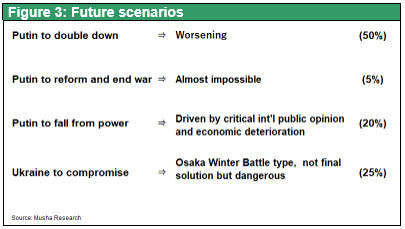

The presence of a German centrist coalition government colored by pacifism, anti-arms proliferation, and decarbonization was a great relief to the Putin administration as it sought to push back NATO. This 180-degree turnaround in policy, though self-inflicted, must have been a major misreading on the part of the Putin administration. So what scenarios can be envisioned for the future? There are four scenarios. The first and most likely scenario is that Putin will double down. He would try to break through the lull in the opening rounds with a more hard-liner approach and win the Ukrainians' acquiescence. The second likely scenario is an Osaka Winter Camp-style response (according to former US Ambassador Fujisaki's theory), using the ceasefire as bait to win concessions such as demilitarization. This would not be a final solution for Ukraine and would be dangerous, as it would be followed by the Summer Campaign. The third possibility is a scenario in which Vladimir Putin is ousted or removed from power due to mounting international criticism and a deteriorating domestic economy, but the time is not yet ripe and this is unlikely in the immediate future. The fourth scenario is that Mr. Putin will change his mind and end the aggression, but this is almost inconceivable.

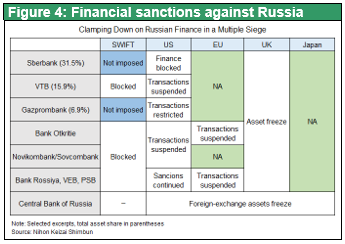

Can economic sanctions force Mr. Putin to back down?

Put in this way, if Ukraine does not change its posture toward war, the only ultimate solution is for Vladimir Putin to step down. A regime change may be difficult to achieve unless there is a growing pessimistic mood within Russia and considerable criticism of Putin, which would require EU and US economic sanctions against Russia, exclusion from SWIFT, financial sanctions, and a considerable increase in damage to the economy. How effective would economic sanctions such as the exclusion from SWIFT be? A major policy shift in Germany, the largest natural gas customer, would be a blow to Mr. Putin, but it may not cause much damage in the short term. This is because Russia's largest bellwether Sberbank, Gazprom bank, the third largest, remains exempt from the SWEFT exclusion and can continue to supply oil and gas.

Ruble Plunge, Inflation Key to the Outlook

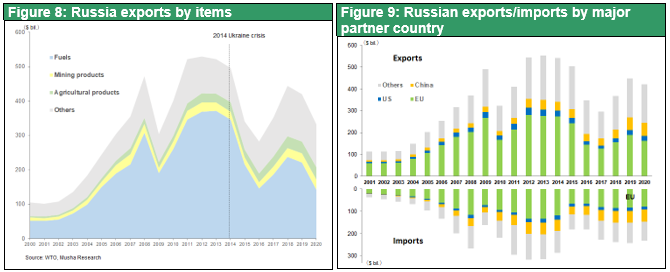

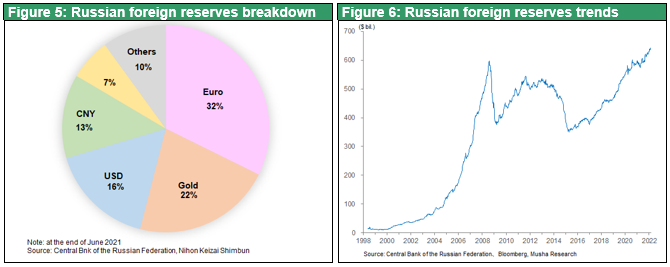

Rather, the suspension of the Central Bank of Russia's draw with the Central Banks of Japan, the U.S., and Europe, and the freezing of Russian foreign currency, which were announced at the same time, may have a greater impact. In preparation for such a situation, Russia seems to have increased its foreign currency reserves significantly and diversified their contents to prepare a system that can withstand sanctions. Just before the invasion of Ukraine, Russia held $643 billion (¥74 trillion) in foreign currency reserves, a 70% increase from the bottom in 2015. As of June of last year, they consisted of 32.3% in euros, 21.7% in gold, 16.4% in US dollars, 13.1% in yuan, 6.5% in British pounds, 5.7% in Japanese yen, 3.0% in Canadian dollars, and so on. Among these, the U.S., U.K., Canada, and EU-Japan have already frozen Russia's foreign exchange reserves, which amount to about 60% of Russia's total. They have been carefully increasing the weight of gold and yuan, but this will not be enough. The IIF (International Institute of Finance) is concerned about Russia's default is considered highly probable. Russia will have to face a decline in economic growth of more than 10%.

EU, US, and Japan, in that order, will be hit first, but a recession can be avoided

On the other hand, Europe, which is dependent on Russia for energy, will also be hit hard, but the negative impact of higher gas and oil prices will be limited. A catastrophe like the third oil shock is unlikely. Shale gas and oil production could be increased in the U.S. and converted to Qatar and Algeria. Even if there could be a CPI increase of up to 1% in the U.S. and Europe, it would not be enough to plunge them into recession. The drastic economic damage would be Russia's alone.

If this trend continues, Russia will decline into a developing poor country

It would have a limited negative impact on the global stock market because the pressure to tighten monetary policy will weaken and as seen in Germany's policy about-face, the unity of the world's democracies will strengthen, which is expected to have a positive impact on investment sentiment. However, Russia, with its weakened industrial base and resource-dependent, emerging-market-type economic structure, will face further difficulties. The decline of Russia's economic presence is inevitable, and it may eventually fall into the category of a poor developing country dependent solely on energy.