May 02, 2022

Strategy Bulletin Vol.304

The irreversible ¥130/dollar, the path to the revival of high-tech industrial clusters

- The decisive factor of Japanese industrial revival, the weakening of the yen has arrived! (1)

The yen's sharp fall to 131 yen to the dollar has clearly ushered in the era of long-term yen depreciation that Musha Research has been advocating for the past decade. Underlying the yen's depreciation are two major factors: (1) the outstanding strength of the US economy to withstand high interest rates, and (2) the US-China conflict, the need to build a supply chain that eliminates China and revive Japan's industrial competitiveness as a key player in this process make the yen's depreciation as the driving force directly linked to US national interests. Without these insights, there is no point in discussing whether a weak yen is good or bad in the short term and on a superficial level. The Nikkei newspaper is campaigning for a "bad yen". It is incorrect to suggest that the Bank of Japan (BOJ), which continues to pursue ultra-easy monetary policy, is in trouble as a manifestation of the "bad yen".

Under the overwhelming strength of the US economy, and the increasingly fierce confrontation between the US and China over the war in Ukraine, the yen's depreciation will be irreversible. This would lead to improved corporate performance and greatly strengthen Japan's industrial competitiveness. A 20% weakening of the yen since the beginning of the year will lead to a 20% rise in Japanese stock prices. Both the "short-lived yen depreciation" and the "bad yen depreciation" theories will disappear sooner or later.

I would like to report on ‘The yen's depreciation, the decisive factor of Japan's industrial revival, has arrived! ’ in two issues.

Strategy Bulletin Vol. 304

Irreversible 130 yen/dollar, the path to the revival of high-tech industrial clusters

(1) The British Empire and Japan, where currency appreciation debilitated national power

(2) The root cause of Japan's disease: the strong yen is over and the weak yen has begun to heal Japan

Strategy Bulletin Vol. 305

Taiwan-Japan industrial cooperation coming into view

(3) Japanese high-tech revival with TSMC at its core, propelled by the 130-yen depreciation

(4) A weak yen is essential for building a high-tech industrial cluster in Japan

(1) The British Empire and Japan, where a strong currency weakened national power

Weakening of the yen is good from the perspective of long-term national interest

There is much discussion in the media of a 'bad yen' depreciation, where rising import prices hit households directly. Business leaders also argued for a bad yen depreciation, with Kengo Sakurada, the representative secretary of the Keizai Doyukai (Japan Association of Corporate Executives), saying, "I can't believe it is at an appropriate level" and "Exporters are not the only ones pulling the Japanese economy forward". Mr Hashimoto, Chairman of the Iron and Steel Federation, stated, "In Japan, where it is difficult to pass on import prices to prices, is a policy of accepting a weak yen a good idea?" Many economists, including Yukio Noguchi and Daisuke Karakama, also argue that the weak yen is a sign of Japan's decline and should not be left unchecked. Certainly, as BOJ Governor Kuroda has pointed out, sudden changes can be disruptive and smoothing adjustments are necessary, but we should not resist the trend of a weaker yen.

A weaker yen is good for exporters and bad for importers, and there are conflicting interests in the short-term depending on the parties involved. However, in the long term, it is infinitely preferable for Japan's national interests and the prosperity of the Japanese economy. A weakening of the yen will increase exports and decrease imports and will also cause factories relocated overseas to return to the domestic market and substitute domestic production for imported goods. This will lead to an increase in domestic investment and production in Japan and higher incomes. The opposite happened in the past when the yen was super strong. Japanese companies moved their factories overseas and domestic demand was encroached by cheap Chinese goods. Now, however, Japanese companies' costs (generated domestically) have fallen by half of what they were 30 years ago. In addition, when the coronary pandemic is over, foreign tourists should rush to Japan, where prices have become cheaper. Thus, the basis of all economic activity is to strengthen the recovery of price competitiveness. A weaker yen is essential for this.

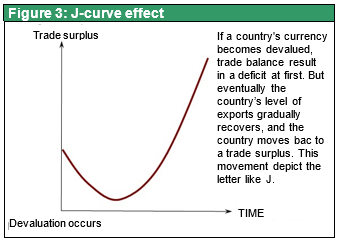

The J-curve effect will bring enormous benefits from a weaker yen

The reason why economists and the media, especially the Nikkei, which represents the interests of Japanese business, do not report such clear benefits of a weaker yen is that most economists and journalism only see short-term increases in import prices due to a weaker yen and the resulting inflation. However, any seasoned economist knows that there is a J-curve effect in the balance of trade (i.e. the contribution of trade to domestic income) when the yen weakens. In other words, at the beginning of the yen's depreciation, the unit cost of imports rises and the trade deficit increases, at which point the yen's depreciation appears to be negative, but eventually the yen's depreciation brings about a significant volume change. In the domestic market, there will be a shift from expensive imports to cheaper domestic products, and in overseas markets, cheaper Japanese products will displace foreign products and increase their market share, leading to increased production, employment and investment in Japan. Japanese companies now say they are producing overseas instead of exporting, but the profits of overseas factories are greatly inflated by the weak yen, and the profits are brought to the Japanese parent company in the form of increased financial income and services such as technical instruction fees and dividends.

The 'good strong yen' argument, bowing to US criticism of Japan and the narrow interests of the financial community

The most important thing in foreign exchange is to build industries and employment in favor of the home country in the international division of labor, and history has proven that it is in the national interest to weaken the home currency for this purpose. The fact that the 'beggar-thy-neighbor policy' which induces the depreciation of the national currency to strengthen the price competitiveness of the national industry and increase exports, has been criticized as evidence of this. The focus of US policy towards Japan from the 1980s to around 2000 was to deny the depreciation of the yen and force the yen to appreciate, which was the cause of Japan's free lunch. In the US, the policy of "a strong dollar is in the national interest" by Treasury Secretary Rubin during the Clinton administration was once adopted, but this was due to the unique situation of the US, which is a reserve currency nation and does not have to worry about deficits because its external debt is immediately converted into seigniorage. This does not apply to Japan at all.

In response to this pressure for a stronger currency against Japan, some commentators, such as Bank of Japan Governor Toru Hayami, stated that a stronger yen was in the national interest, but this was a self-serving argument on behalf of the financial community, which was overconfident in Japan's industrial competitiveness and wanted to take advantage of outward investment. In truth, they may have been influenced by US mind control.

The source of the downfall of the British Empire, a currency appreciation that succumbed to the narrow interests of the financial community

In 19th century Britain, the early introduction of the gold standard and the maintenance of a strong currency led to the decline of the British Empire, as its industrial competitiveness, which had been so strong, was overtaken by Germany and the USA in just a few decades. The regret is great that British monetary policy continued to acquiesce to the interests of the financial community, which wanted to channel its huge savings surpluses into overseas investment. The disfavored economist J A Hobson, the first advocate of the 'imperialist theory' followed by Lenin, argued that excess savings due to insufficient domestic demand was a problem His recommendation of expansion of consumption power = promotion of domestic demand was completely ignored by academics and politicians. Had this been made policy, the decline of British industry due to a strong currency could have been avoided. The realization of Hobson's proposal had to wait until Keynes came along 30 years later. (See my book 'The New Imperialism', 2007, Toyo Keizai Shinpo Sha).

Another good example of the negative effects of a strong currency policy is that during the Showa Depression of 1930, the austerity policy of Junnosuke Inoue, who advocated a strong currency and lifted the ban on gold at the old par value, led to the economic catastrophe. On the other hand, the Republic of Korea, where the depreciation of the currency during the Asian financial crisis and the GFC greatly boosted the competitiveness of high-tech companies such as Samsung Electronics and SK Hynix, is an example of the success brought about by a weak currency policy.

Seen in this light, the fact that we are now in an environment where we can enjoy a weak yen without being blamed for it is entirely welcome.

(2) The root cause of Japan's disease, the strong yen, has ended and the weak yen has begun to heal Japan

From a punitive appreciation of the yen to an era of beneficent yen depreciation

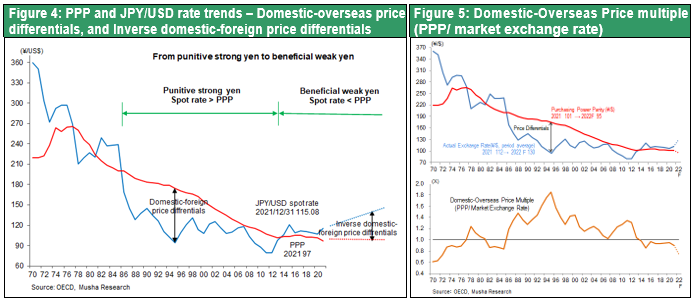

As analyzed in Strategy Bulletin No 302 (1 April), the era of punitive yen appreciation, which fundamentally destroyed Japan's competitiveness, is clearly over and the era of yen depreciation beyond its ability to benefit Japan has begun. What is punitive and what is beneficial can be observed in the ratio between the purchasing power parity (i.e. the yen's strength) and the actual exchange rate. As shown in Chart 5, from the late 1980s to 2001 and from 2009-2013, the Japanese yen experienced a punitive appreciation that exceeded its purchasing power parity by 100% at its peak and by more than 30% on average, which significantly degraded Japan's competitiveness and quickly erased its trade surplus.

The "Shirakawa Bank of Japan" gave a death sentence to the high-tech industry

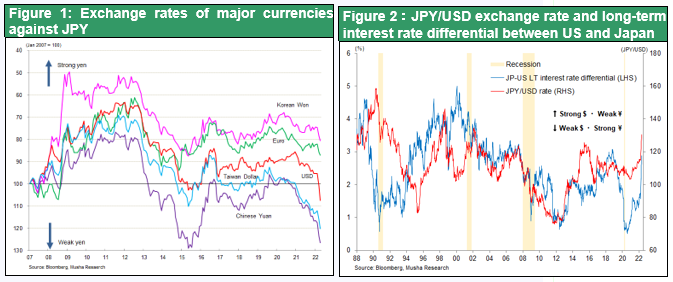

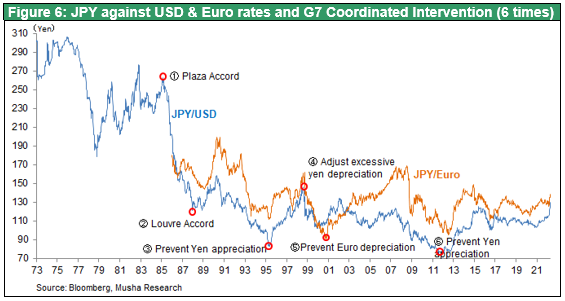

The super-strong yen in 2008-2012, especially after the GFC, drove the already struggling high-tech industries (semiconductors, LCDs, TVs, mobile phones, PCs, etc.) into bankruptcy, and despite the first coordinated G7 intervention in 10 years when the yen hit 80 against the dollar at the time of the Great East Japan Earthquake in March 2011, a leading-edge semiconductor company Elpida Memory went bankrupt and was acquired by Micron Technology in March 2012.. Sharp's last-ditch investment in an LCD plant also failed. As can be seen in Figure 6, the last six G7 coordinated interventions have all resulted in an immediate major turnaround in the exchange rate from extreme levels, but only in 2011 did this not happen because of strict monetary policy by BOJ. The damage caused to Japanese industry and national interests by the BOJ's misguided monetary policy was enormous. At the time, the Korean won had depreciated by 30% compared to the pre-GFC level, while the Japanese yen appreciated by 30%, and the Korean won depreciated by nearly 50% against the Japanese yen between 2008 and 2012 (see Figure 1). Japanese firms were knocked out by South Korean firms, which already had a well-developed industrial base and competitiveness, partly due to government support. With the exception of semiconductor production equipment, semiconductor materials and electronic components, which South Korea had not yet entered, the core of Japan's high-tech industries collapsed.

High-tech industry clusters that were destroyed by the strong yen will be revived by the weak yen, and the key to this revival will be cooperation between Japan and Taiwan

However, now that Japan has fallen into a trade deficit country, it is likely to enter an era of beneficial yen depreciation. The punitive appreciation of the yen has already been resolved since around 2014, and the revival of Japanese industry and business is underway. Corporate profits are at an all-time high and overseas production has already peaked and begun to decline. Reforms and new business models of Japanese companies are emerging in the high-tech peripheral industries that have survived. (See Strategy Bulletin No. 297 (1 Jan 2022) 'Outlook for 2022 - Focus on the business models of Japanese companies that will lead the NEXT GAFAM').

An era of beneficial yen depreciation is one in which an exchange rate that is considerably (more than 30%) lower than purchasing power parity is established and Japan's price competitiveness is given a benefit from a foreign exchange perspective. As in the era of the punitive appreciation of the yen, the national interest of the hegemonic US will be key this time as well as economic rationality. The US is concentrating on building a supply chain away from China, and as part of this, it will be necessary to rebuild the world's high-tech production clusters in Japan, which are concentrated in China, South Korea and Taiwan. A gratuitous depreciation of the yen will be essential for this.

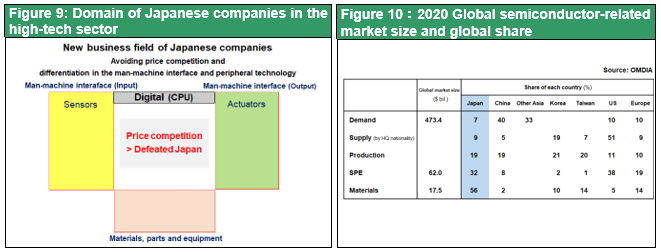

Fortunately, Japan has lost ground in core and final high-tech products such as semiconductors, LCDs, TVs, mobile phones and PCs, but has differentiated itself in digital peripheral fields (sensors, actuators, components, materials and equipment) and gained a high market share. Although each of these products is niche and the market size is not necessarily large, it can be said that they are holding back the bottlenecks in the global high-tech supply chain. Is it not clear that Japan is the key to building a high-tech supply chain outside China?

As will be developed in the next issue, the US should be faced with the need to rebuild high-tech industry clusters in safe territory Japan in Asia. The already lost digital hub will be supplemented by cooperation with Taiwan, and the resuscitation of Japan's high-tech industry will proceed. A reverse cycle of what happened with the punitive appreciation of the yen is expected. The biggest beneficiaries of the weak yen will probably be the high-tech industries, which were the biggest victims of the strong yen.