May 23, 2022

Strategy Bulletin Vol.306

Good Inflation Leads U.S. to Soft Landing

Market Sentiment Deteriorates by Degrees

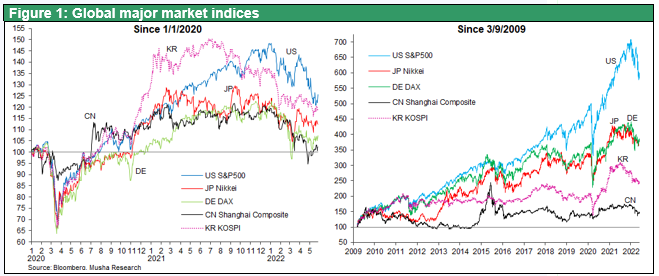

Global equities suffered their biggest plunge after sharp recovery form Covid 19 pandemic clash with the S&P 500 Index falling 20% since the beginning of the year, and pessimism prevailing. Institutional investors, representing the bearish sentiment, are now at a 6% cash ratio, the highest level since the 2001 terrorist attacks in the United States. While the majority of economists believe that a recession can be avoided, and the Fed and other US authorities have been insisting that this is the case, the stock market does not seem to have much faith.

Inflation has peaked out on all fronts

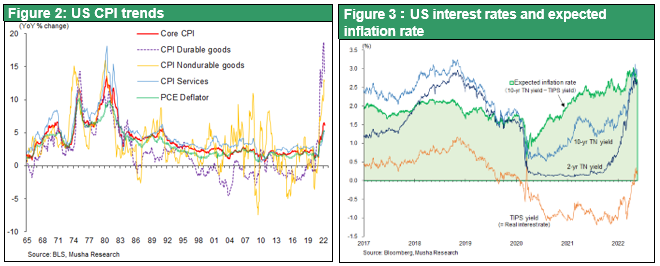

However, equities are often extremely optimistic or pessimistic, and they are not hopeless. The biggest concern is inflation, which has risen to levels not seen in 40 years but is already peaking out: the CPI was 8.3% in April (6.2% for core CPI excluding food and energy), but is expected to fall to the 5% range later in the year and enter the 2-3% range three years ahead. The long-term price expectations that financial markets are factoring in can be observed in the gap between the yield on 10-year Treasuries and the yield on 10-year inflation-protected bonds (TIPS), which peaked at 3.0% at the end of April and has fallen to 2.6% as of May 20, 2012. The reasons for the peaking out of inflation expectations are: (1) inflation caused by the supply chain is subsiding, (2) the surge in oil and resource prices will subside as demand slows in China and Europe in addition to the search for alternative sources of Russian oil, (3) selective wage increases are occurring in the US where labor supply and demand are tight, but not a general increase in wages, and (4) Rising long-term interest rates and falling stock prices have already had the effect of suppressing the economic activities such as housing purchases (the so-called "bond vigilantism" effect).

The hawkish bias in monetary policy will also weaken

If this is the case, monetary tightening and interest rate hikes are likely to subside at some point. The 2-year yield of 2.6% means that the market has factored in the fact that the FF rate will be at 2.6% in two years that is four more 0.5% rate hikes. So there will be no more hawkish statements that could surprise. The fears that a late rush to tighten monetary policy could force the Fed to raise rates too much, which could kill the economy, but the chances of that happening are small for reasons discussed below. For the reasons discussed below, the chances of this happening are small. In addition, profit growth is expected to continue due to corporate innovation and rising productivity.

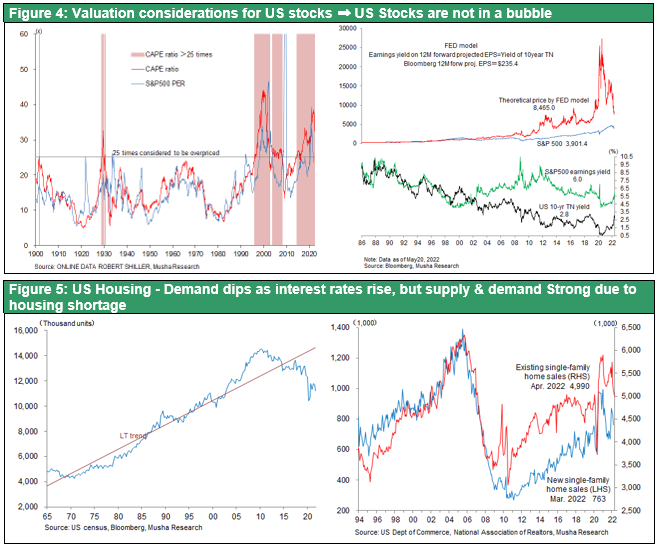

Avoiding a stock market crash is essential for a soft landing, and U.S. stock and housing prices are not in a bubble

At the risk of sounding like a tautology, the most important condition for a soft landing is the deterioration of economic sentiment caused by a stock market crash, and the Fed will absolutely avoid a freeze in economic sentiment caused by a stock market crash. As Musha Research has long argued, macroeconomic policy in the U.S. has shifted from demand creation through bank lending to demand creation through rising asset prices, and the Fed's implicit targeting of asset prices in its monetary policy cannot be changed now. And asset prices, including stocks and real estate, are hardly in a bubble state, assuming long-term interest rates of around 3%, and that there is no need for further asset price adjustments.

The PER of the S&P 500 index has fallen from less than 23x at the beginning of the year to less than 17x. As shown in Figure 4, the current S&P index of 3900 points is half of the FED model's estimate of 8465. The demand for housing, which had been rising sharply in price, has slowed down due to rising interest rates. However, as seen in the decline in the number of vacant houses, the supply-demand balance caused by the housing shortage continues to be tight, and we are not in a situation where prices should be restrained by raising interest rates, as was the case during the subprime bubble (Figure 5).

Good Inflation, Wage Increases in Progress Bringing Narrowing Inequality

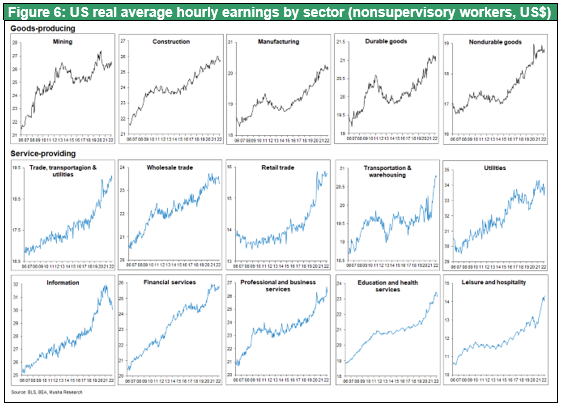

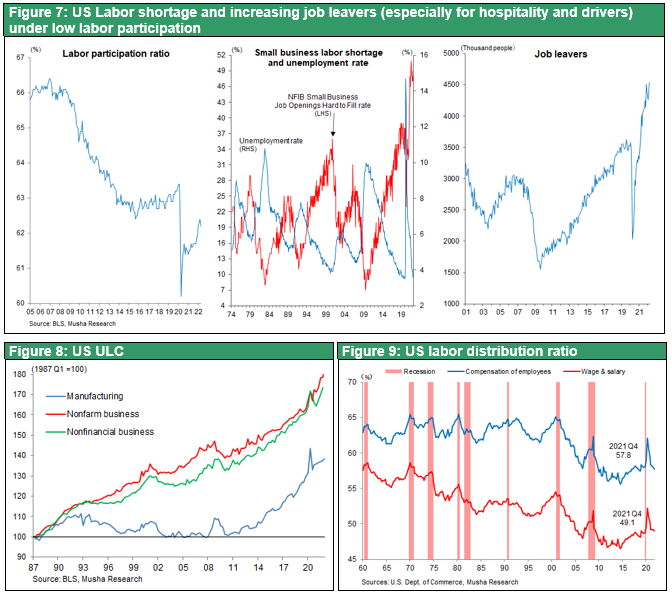

We would like to point out two trends that we believe do not warrant undue concern about the U.S. inflation situation. The first trend is that good inflation is underway. With unemployment in the 3% range and full employment, rising wages in the U.S. are certainly a matter for caution. However, I would like to emphasize that the current wage increase has a positive aspect for economic growth and is not a bad wage increase that would lead to stagflation. This can be concluded from three characteristics of the current wage increase. (1) Wages of low-wage muscle workers such as truck drivers are rising, while those of high-wage workers in the information, utility, and financial industries have fallen , narrowing the gap (see Figure 6), and (2) While companies continue to face a job shortage, the number of workers voluntarily leaving their jobs is at a record high, which indicates that workers are choosing jobs i.e. their bargaining power is increasing (See Figure 7), and (3) the companies offering jobs are those with the ability to raise prices, and as companies' excess profits are converted into higher wages, consumption is expected to rise and the growth rate will increase. As seen in Figures 8 and 9, the unit labor cost of firms has been rising since around 2016, and the labor share has bottomed out and reversed, a trend that has continued since the Corona Shock, both of which have boosted household labor income and are very positive developments for the economy as a whole. The biggest problem in the U.S. economy is the accumulation of excess profits by the corporate sector and the wealthy, which are not easily linked to real demand. (A detailed analysis will be presented in the next issue.) In 2022, the U.S. nominal economic growth rate is expected to exceed that of China at 10%, which will have a positive impact on corporate profits.

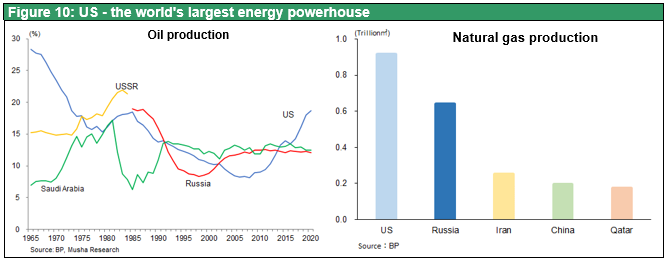

The second trend that we should not overly worrisome for inflation is the industrial strength of the U.S. and the strength of the dollar. The U.S. is the world's largest producer and net exporter of soaring crude oil and natural gas, so the surge in resource prices is positive for the country, and while higher oil prices hurt consumers, they significantly boost the earnings of energy-related companies. Similarly, the U.S. is the world's largest exporter of grain, which is not a negative factor for the country.

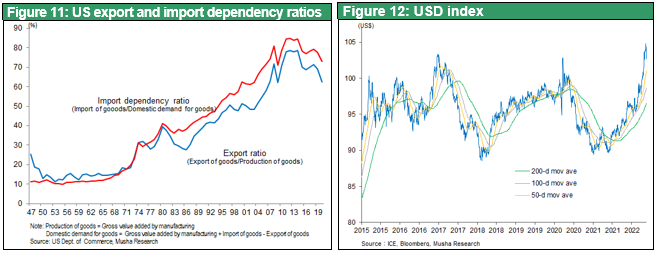

Furthermore, the strong dollar will be a major force in restraining U.S. prices. As shown in Figure 2, this inflation is characterized by the fact that it is the first goods price-driven inflation (especially for durable goods) in recent decades. Until now, inflation in the U.S. has been driven by services and asset prices, while prices of goods (manufactured goods) such as apparel and electronics have been stagnant or even declining, as in Japan, where deflation has persisted. The year-on-year CPI growth rate for April was 14.0% for durable goods, 12.8% for non-durable goods, and 5.4% for services. As shown in Figure 11, 70% of goods consumed in the U.S. are import-dependent. This suggests that the dollar's appreciation (Figure 12), which is up 14% from the previous year, could be a decisive factor in keeping down goods inflation by reducing the cost of imports. In this light, we can conclude that for the U.S. today, inflation is not malignant enough to lead to stagflation. Rather, it will reinforce U.S. dominance in the global economy.

These are the reasons why a significant decline in U.S. stocks from here is unthinkable.