Apr 19, 2023

Strategy Bulletin Vol.330

Fundamental Contradictions and Inflation in the U.S. Economy

- The "Too Good to Be True" (Mystery) of the U.S. Economy and its Basic Contradiction (2)

In times of turmoil, the basic view of risk is undergoing a major shift. From deflationary measures to inflationary measures, from liberalism to protectionism, from small government to big government, from globalization to anti-globalization (from promoting to restraining the international division of labor), how should we view the changes in economic views that have become apparent at once? There seems to be a 180% divergence in the advice on policy and the outlook for the future. Even regarding the immediate market outlook, there is a mixture of optimism and pessimism that cannot be settled by logic.

However, a closer look at the U.S. economy over the past few months suggests that it is premature to assume that a new regime of rising inflation and interest rates has begun (Note). The existence of a jobs boom and ample liquidity under tight monetary conditions, and the peaking out of wage growth under a booming jobs market, are " too convenient truth " compared to common knowledge. It is even possible that this could lead to the next virtuous cycle of economic expansion. It may be necessary to assess that the AI Net revolution, innovation, and further efficiency gains in the U.S. labor and capital markets are making the U.S. economy more resilient.

(Note) The IMF published in its WEO released on April 10, 2023, its analysis that the rise in real interest rates from the second half of 2021 will be temporary.

(1) Conflicting Policy Goal Setting, Deflation or Inflation as the Enemy

The risk of deflation and Japanification that covered the world just two years ago has disappeared, and the global economy now faces a sudden surge in prices due to supply chain disruptions caused by the Corona pandemic and rising energy prices from the war in Ukraine. Central banks of major economies have turned to rapid monetary tightening policies, and it is becoming accepted that the long-term trend of disinflation and falling interest rates, which had been in place for 40 years since the 1980s, has reversed itself. Has there been a major shift from deflation to inflation as the enemy that the commanders of the world's economies must fight?

At the same time, the U.S.-China confrontation and the war in Ukraine have brought geopolitical upheaval to the international division of labor. Through endless globalization and the lowering of border barriers, China has gained half share of world major manufacturing products. However, the international division of labor now has undergone a significant shift due to decoupling from China. In the high-tech sector, there is an urgent need to build a de-China supply chain, and there are fears that international trade, which had been expanding, will recede, which will accelerate its impact on inflation.

In response to the energy crisis and environmental changes, countries have begun to reevaluate the role of government and public finance. In the U.S., the enactment of the CHIPS Act, which provides massive public spending on the semiconductor industry, and the IRA, which promotes spending on clean energy and EVs (Inflation Reduction Act: funded by a 15% minimum corporate tax rate and increased tax revenues from drug price reform), have brought fiscal support for industry to the forefront. Faced with international competition in the high-tech and green industry sectors, the trend toward greater public support for industry was irreversible in Europe and Japan too. In addition, the creation and increase of carbon taxes and emission credits to generate funds for green investments, which are underway in many countries, are also raising energy costs, along with the tightening supply and demand for crude oil and natural gas. Thus, the disinflationary pressures brought about by deregulation and the promotion of competition through small government that have been continued for the past 40 years or so have turned around dramatically.

This trend toward big government is also thought to be a source of upward pressure on interest rates because of the deterioration in the fiscal balance. Fed Chairman Jerome Powell, who until a year ago had maintained an easy monetary policy on the grounds that inflation was transitory, has changed his stance and raised interest rates nine times in one year, for a cumulative 4.75% hike, and is now taking a more hawkish stance, suggesting that he will raise rates before the end of the year.

(2) Basic Contradiction in an Era of Deflationary Risk

First, let us look at deflation and Japanification, which were considered to be the greatest risk for the developed world until the outbreak of the war in Ukraine. The risk that has crept into the world since Japan's deflation have started around 2000 is that the excess profits of the corporate sector have been stored away, causing interest rates to fall and growth to slow, a chronic disease, so to speak, in the U.S. and other advanced economies. The chronic disease progressed most strongly in Japan.

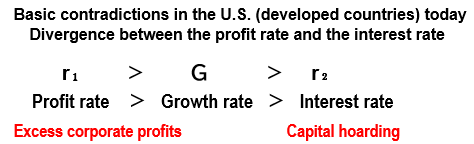

Divergence between the profit rate and the interest rate

Two inequalities exist in the current advanced economies that jeopardize the system. The first inequality is that the profit rate (r₁)>economic growth rate (g). The inequality "r>g," where "r₁=return on capital" is greater than "g=growth," is an argument made by Thomas Piketty that has gone viral. In his best-selling book, "Capital in the 21st Century," Thomas Piketty pointed out that the significantly higher return on capital and lower growth leads to widening inequality. He stated that correcting this widening inequality would require the international introduction of progressive taxation on capital, but more recently he has argued that a socialist approach is needed ("Come, New Socialism: Reading the World," Misuzu Shobo, 2022). Immediately after the collapse of Lehman Brothers, a movement called "Occupy Wall Street" also emerged in New York, as only 1% of the population controlled the overwhelming wealth of the city. Indeed, the current era of unprecedentedly high corporate profits, coupled with the resulting rise in asset prices, has led to widening inequality. This has caused the downfall and fragmentation of the middle class in developed countries, leading to political instability.

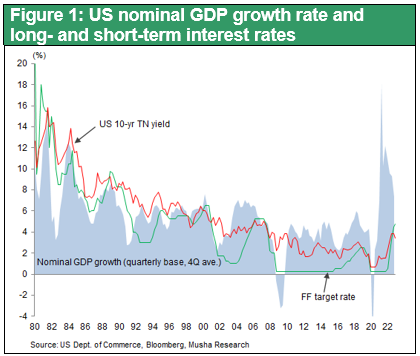

Even if this is the case, then it is not enough to understand the economic situation of this period. That is only half of what is happening. The other reality is that the return on capital is lower than growth. There are two indicators to measure the return on capital, the rate of profit (return on invested capital = r₁) and the rate of interest (r₂), and the other return on capital, the rate of interest, was, on the contrary, much lower than the growth rate of the economy. Behind this unprecedentedly low interest rate, there is unprecedented saving (= capital surplus). The inequality g>r₂ (economic growth > long-term interest rates), the fact that former Fed Chairman Greenspan called as a "conundrum," and baffled him since the tightening of monetary policy that began in 2004, was totally ineffective. The tightening of monetary policy was not followed through, and ample liquidity, accelerated speculative residential investment by individuals (see Figure 1).

In other words, companies and investors are enjoying excess profits, but these profits are stored as excess savings in the financial markets, depressing the growth rate and widening the contradiction. This indicates that although the returns on capital are the same, the profits of corporations (profit rate = return on invested capital) have risen while the profits of savers (interest rate = long-term interest rate) have declined, and the gap between the two has widened endlessly. Although we are in a favorable environment in which corporate investment with low interest rates can yield large investment profits, if the divergence between the two continues to widen, there is a risk that an asset bubble will form at some point and cause a Great Depression-type economic crisis, or even the collapse of the system.

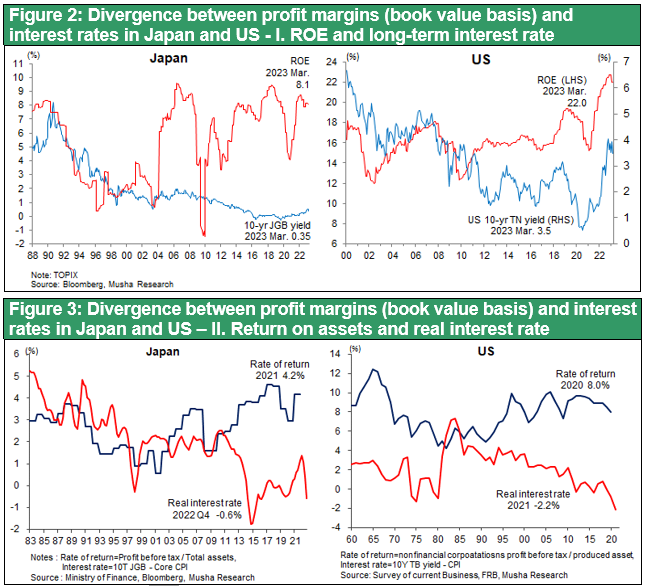

In my 2007 book "New Imperialism" (Published by Toyo Keizai Shinposha, Inc.), I pointed out that the divergence between the profit rate and the interest rate in the U.S. and Japan started to occur around 2000, creating the conditions for stock market appreciation (p. 108). Figure 2 tracks the profit rate and interest rate in Japan and the U.S. over time, and the divergence between the two has grown since around 2000 in both Japan and the U.S. The divergence became even larger after GFC.

The increase in labor and capital productivity due to the new industrial revolution is causing surpluses

The root cause of this unusual reality of high corporate profits and unprecedentedly low interest rates is thought to be the remarkable excess profits that corporations are earning due to the productivity gains brought about by the new industrial revolution (and the benefit of low-wage labor brought about by globalization). In other words, companies are making a lot of money. However, they are unable to reinvest the money they have made, so they are letting it sit idle, and interest rates are falling. The decline in interest rates, which is becoming more pronounced in developed countries, suggests that there is a "slack" of capital. In addition, stagnant employment and wages (high unemployment, low labor participation, and weak wage growth) indicate the existence of a labor surplus "slack”.

The new industrial revolution involving IT, smart phones, cloud computing, AI, etc., is engulfing globalization, bringing unprecedented productivity gains and significantly lowering the need for labor input. This has immediately led to a remarkable increase in corporate profits while at the same time creating a "slack" (surplus). The increase in labor productivity and decrease in labor input due to the Internet digital revolution has expanded quickly with telecommuting, remote work, and remote meetings using Zoom, Teams, etc., triggered by the Corona pandemic, prompting further increases in productivity and changes in work styles.

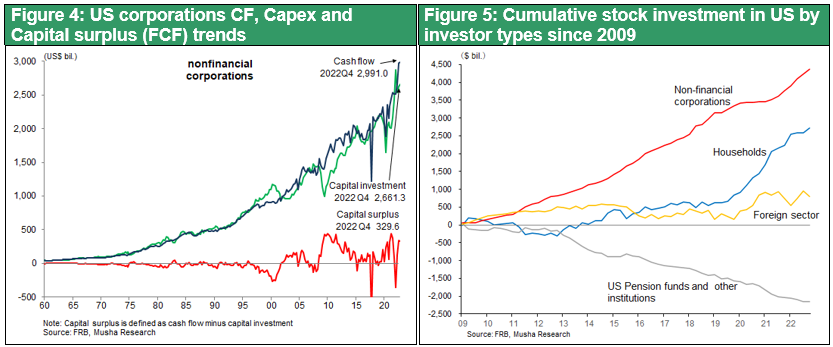

In addition, technological innovation has caused a rapid decline in the price of digital equipment and other facilities and equipment, and companies in the U.S. and Japan have long since stopped having to reinvest all depreciated amounts. Leading companies such as Apple and Google routinely have huge capital surpluses. Even in intangible asset investments such as software development, productivity has increased and the amount of required investment has decreased. This trend is accelerating as inexpensive and equitable AI finally enters the diffusion phase. FANNG are generating huge revenues, but the amount of reinvestment required to keep them in business is surprisingly small. These can be said as capital productivity gains (productivity gains per unit of capital), which have led to constant positive cash flow for the corporations. Figure 4 shows the trend of free cash flow (cash flow - capital investment) in the U.S. Free cash flow, which used to be consistently negative, has become consistently positive since around 2000. In the past, the profits (surpluses) of leading companies such as GE and GM returned to economic growth resources by allocating them to new plant construction and hiring new employee, but today's leading company FANNG has no such channel. Since the GFC, U.S. companies (excluding financials) have returned almost 100% of their profits to shareholders as share buybacks and dividends. Cash surpluses from excess depreciation have been used for financial expenditures such as M&A and investment in start-ups and have been the source of conglomeration.

(3) The era of deflationary risk is not completely over

The question is whether the basic structure of the past two decades of excess profits in the corporate sector, capital hoarding, and falling interest rates has changed with the current shift in inflation and monetary policy, but the reality observed in the U.S. economy today indicates that the framework of the deflationary economic era has not completely changed.

Surplus of Funds Has Not Changed

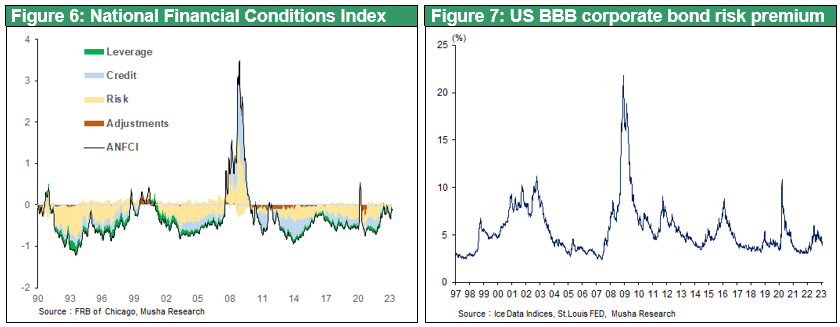

First, the global glut of investment capital remains unchanged. Despite historic rate hikes, ample liquidity remains robust, flowing into emerging market equities and lower-rated U.S. credit markets, and risk premiums have begun to decline (Figure 7). Most importantly, the yield on the 10-year U.S. Treasury note has fallen to around 3.5%, even though short-term interest rates have been raised to 5.0%. This is half the CPI and nominal GDP growth rate, and based on the Taylor rule, it can be said to still be at an accommodative level. It can also be said that the money glut is making monetary tightening ineffective. The Financial Conditions Index calculated by the Federal Reserve Bank of Chicago has improved significantly since the fourth quarter of last year (Figure 6). The fact that ample investment funds remain hefty despite the historic rate hikes was completely unexpected by many observers. It is as if we are witnessing a replay of the 2005 Fed Chairman Greenspan's “conundrum”.

Some have interpreted the decline in long-term interest rates as a sign of economic uncertainty, but this does not make sense with the rising prices of riskier emerging market equities and junk bonds, as well as the increase in U.S. bank lending and the rise in the copper market, which linked to the global economy. Just as the decline in long-term interest rates since 1980 was not a harbinger of an economic downturn, the current decline in long-term interest rates could be due to other factors. As mentioned above, the value generated by the corporate sector is greater than the investment required by the corporate sector, resulting in a continuous capital surplus.

Labor Surplus Continues Even under Favorable Labor Supply and Demand

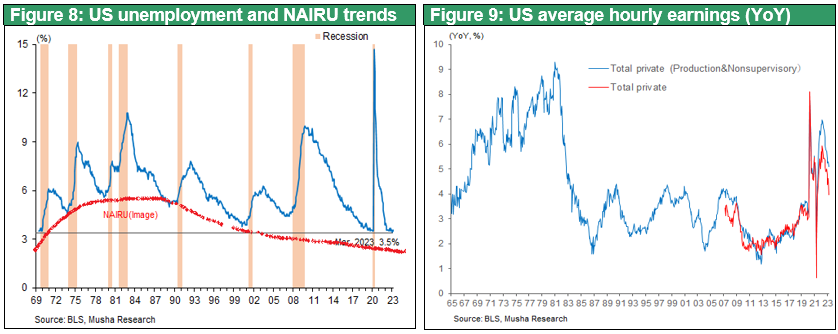

Second, the existence of a slack in the labor market has not disappeared. The unemployment rate fell to a 53-year low of 3.4% in January 2023 and remained at 3.6% and 3.5% in February and March, indicating that companies are strongly interested in hiring and employment is increasing in all sectors.

However, the rate of wage growth started to fall. Figure 9 shows that the average hourly wage (AHE) in January 2022 was 0.7% month-over-month but fell to 0.2% in February 2023 (0.3% in March). The labor shortage in the hospitality industry, including truck drivers, waiters, and waitresses, caused by the extraordinary labor supply-demand crunch under the Corona pandemic, has begun to ease, and the rate of wage growth in unskilled and low-wage sectors has begun to slow. Low employment growth in the higher-paying sectors of finance and the information sector has also pulled down overall wage level growth.

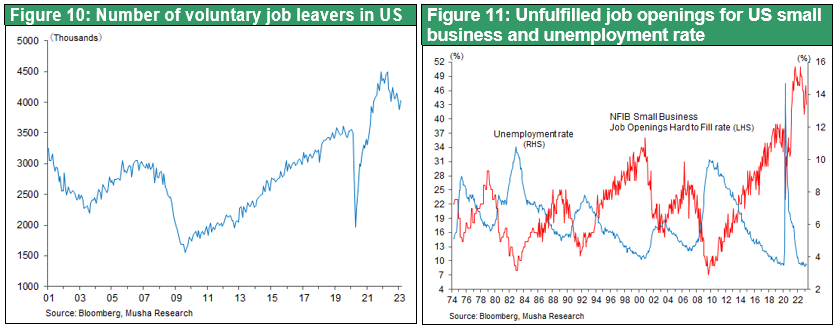

The labor market is moving more resiliently, and the allocation of resources became more efficiently. More specifically, the NAIRU (Non-Accelerating Inflation Rate of Unemployment) may be declining (Figure 8). In the labor market, the Internet has made it possible to instantly match job openings and job seekers. It has also enabled fairer labor wage determination. Job shifting due to skill development may have triggered a chain of salary increases plus productivity gains. The bargaining power of workers is alive and well. The number of workers voluntarily leaving their jobs is high, the percentage of unfilled job openings in firms, especially small and medium-sized firms, is high, and job hopping by workers in search of higher pay is strong. Workers can easily find jobs that match their skills, and the median duration of unemployment was 8.3 weeks in February 2023, lower than the 9.3 weeks in 2019 before the Corona disaster. This may be an environment in which wage growth is restrained while production increases.

Employment may not be a lagging indicator

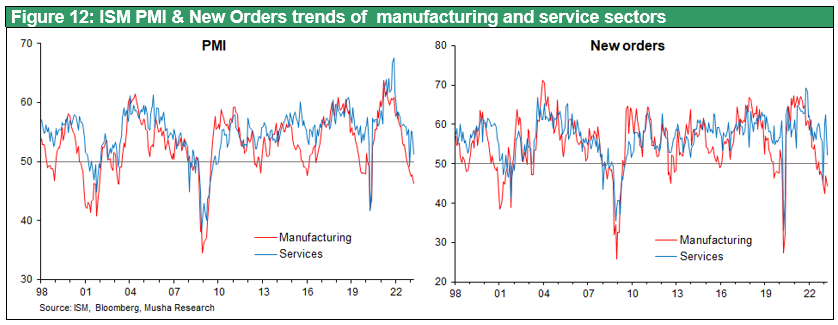

Thus, the employment boom is continuing even under tightening monetary policy and the capital surplus is continuing, and wage growth has peaked out under the employment boom, which is a "too convenient truth" that defies common sense. In this context, the next virtuous cycle may have already begun to take place. While the manufacturing PMI is falling, the non-manufacturing PMI is rebounding (Figure 12). New orders are particularly strong in the non-manufacturing sector, which is supported by a strong labor market and consumption. If this is the case, employment is a leading indicator, not a lagging one, which is another "too convenient truth" that defies common sense.

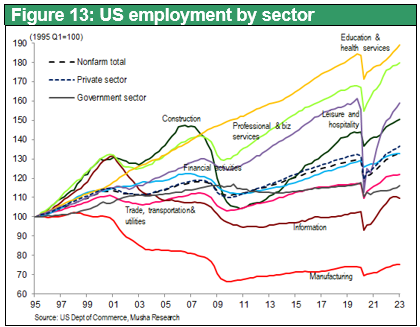

Businesses are willing to hire, and employment is increasing in all sectors (see Figure 13). The virtuous cycle of strong consumption bringing broad employment opportunities has not been undermined at all. During the business process reengineering (BPR) revolutions in the 1990s, there was a phase of jobless recovery when employment was stagnant as white-collar workers were replaced by machines. Compared to those times, one can see how vigorous the creation of new employment opportunities is today.

(4) Policy Implications and Outlook

Increasingly wary of deflation risk (recession risk)

If the NAIRU is declining, there is still a slack in the U.S. labor market, and the Fed's hasty rate hikes will increase the risk of deflation. If the capital surplus has not changed, a reversal of short- and long-term interest rates under such conditions would hurt the profitability of financial institutions and cause an unnecessary financial stress, again increasing the risk of deflation. The chain of bank failures after SVB that occurred in March indicates heightened financial stress.

This means that the risk from here on is not inflation, but recession and deflation. What do the U.S. markets and the U.S. authorities think about this? It seems as if an implicit consensus has formed around this dovish viewpoint. Chairman Powell's comments changed slightly, pointing to disinflation and not completely ruling out the possibility of a rate cut before the end of the year.

US authorities and economists essentially doves

The key here is to determine what the real enemies of U.S. policymakers are. The Fed is essentially fighting deflation. The consensus among U.S. economists and policymakers seems to be that deflation is the result of a failure to achieve highest growth potential, which means policy sabotage, not inevitability. The ultimate goal of U.S. economic policy is to raise the standard of living, although this goal is not clear in Japan, and the Fed's dual mandate of maximum employment and price stability is merely a means to that end. In this regard, the reappointment in December of Treasury Secretary Janett Yellen, a high-pressure economic theorist who is more concerned about the risk of deflation, is highly significant.

The Fed will turn the corner sooner rather than later its unreasonable and unnecessary tightening. If this becomes evident, stock prices will soar. It will be a sign that the AI Internet revolution, innovation, and more efficient labor and capital markets in the U.S. are strengthening the resilience of the U.S. economy.

This report is an updated version of my contribution article published in the May/June issue of World Economic Review (written on February 15).