Mar 15, 2026

Strategy Bulletin Vol.397

The U.S.-China Confrontation Heading Toward Total War

~The Background of Surprise Military Operations in Venezuela and Iran~

An invasion of Venezuela and the abduction of President Maduro, the assassination of Supreme Leader Khamenei and other top leaders through airstrikes on Iran, and the seizure of air superiority through concentrated missile fire—events that seem straight out of an action movie are unfolding in the real world. With an all-out attack launched without a declaration of war, international law and governance by international organizations have been rendered meaningless; we are witnessing a display of the law of the jungle and justice by force. Commentators and governments alike are struggling to grasp the essence and unfolding of these events and are finding it difficult to respond.

A world where the law of the jungle reigns supreme

Ayatollah Mojtaba Khamenei, newly appointed as Iran’s Supreme Leader, has declared that he will “continue the blockade” of the Strait of Hormuz. Having lost air superiority and the ability to counter, Iran is attempting to hold the global economy hostage by blocking this vital chokepoint through which 20% of the world’s crude oil passes. The Financial Times reports: “According to a Goldman Sachs survey, approximately 18 million barrels of crude oil are currently being blocked in this waterway, which normally handles 20 million barrels per day. While about 3 million barrels can be rerouted via pipelines, that still leaves 15 million barrels of crude oil with nowhere to go. As a result, producers have been forced to halt production of approximately 6.5 million barrels of crude oil and 2 million barrels of refined petroleum products. At the peak of the Russian energy crisis in April 2022, Russian oil production suffered a blow of 1 million barrels per day. This time, production has already been hit by 6 million barrels per day. In other words, the scale is six times greater, and from an export perspective, this impact is equivalent to 15 times that of the 2022 crisis.” Furthermore, attempting to transform Iraq’s theocratic regime—the epicenter of terrorism—would require preparing for a protracted war involving the deployment of ground troops. The reason most Middle East and military experts are condemning this as a reckless policy is that, as experienced in Iraq and Afghanistan, they believe many lives will be lost and victory will not come easily.

Remarkable Stability in the Market

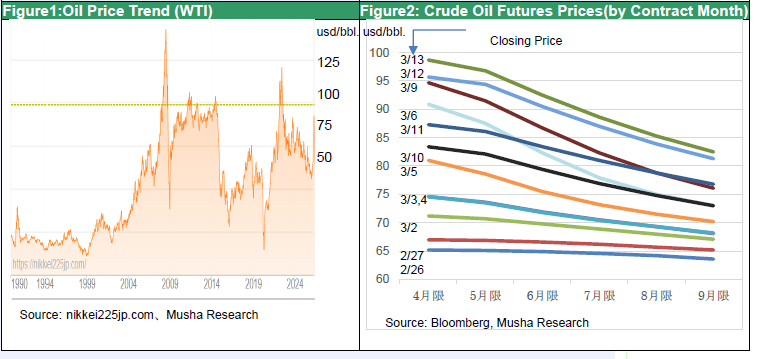

What is surprising is that, amid mounting criticism of the Trump administration’s high-handedness and the use of military force with no clear exit strategy, the market has maintained an almost unbelievable stability. Although crude oil futures (WTI) rose to around $120—the level seen at the outbreak of the Ukraine war—due to the blockade of the Strait of Hormuz, they have since returned to the $80–$90 range following the U.S. securing air superiority and the sinking of mine-laying vessels. Moreover, in contrast to the rise in near-month contracts, price increases for long-term contracts have been limited. Reports that efforts to reopen the Strait of Hormuz are facing difficulties caused WTI near-month futures prices to surge to $98 on Friday, March 13; however, September futures prices remained at $82, indicating a strengthening backwardation.

Figure 1: Crude Oil Price Trends (WTI)

Figure 2: Crude Oil Futures Prices Since the Airstrikes on Iraq (by Contract Month)

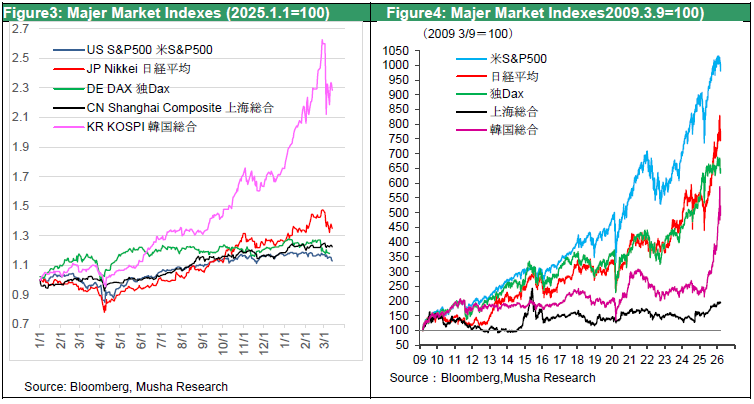

Stock market stability is even more pronounced: the U.S. S&P 500 Index has held steady at 6,600 points, down just 5% from its all-time high of 7,002 points at the end of January. Japanese stocks have also fallen by only 9% from their all-time high, representing less than half the impact of the crash caused by the mutual tariff hikes last April. Even South Korean stocks, which saw the largest decline, fell by 15% from their all-time high just before the airstrikes on Iran, but have since rebounded to a level 12% below that high. Moreover, considering that South Korean stocks surged by 77% over the past year and by 48% in January and February alone, this can be considered an extremely minor decline. As for the dollar and bonds, they have not fallen at all.

Figure 3 and 4: Trends in Major Country Stock Indices

Trump's strategy toward Iran is likely to succeed

The market has shown almost no skepticism regarding President Trump’s statements that the fighting will end soon and that security in the Strait of Hormuz will be guaranteed.

Mr. Bessent stated, “Iranian tankers are passing through. Chinese-flagged tankers must have passed through as well. In other words, we know that Iran has not laid mines. As soon as it becomes militarily feasible, the U.S. Navy will likely escort ships in conjunction with an international coalition of the willing.”

Realistically speaking, it is unlikely that a blockade of the Strait of Hormuz would last more than a few months. This is not only due to the U.S.’s overwhelming military power and Iran’s exhausted economy and weakened governance. It is also because China—Iran’s biggest backer and the buyer of 90% of Iran’s crude oil—cannot withstand such a situation. China, now the world’s largest industrial nation, is also the largest importer of crude oil. It relies on imports for 70% of its crude oil demand, and it is said that 40% of that passes through the Strait of Hormuz. China’s crude oil reserves are limited to 100 days’ worth, compared to 200 days’ worth for developed nations. Compared to the United States—the world’s largest producer and exporter of crude oil and natural gas, which is entirely independent of the Strait of Hormuz—China’s energy vulnerability is striking, making a prolonged blockade of the Strait of Hormuz an unviable option.

The most likely scenario is that the Trump administration will secure stability in the Middle East and bring the fighting to a successful conclusion. The feared deployment of ground troops to Iran, a protracted conflict, and rising casualties will be avoided. It is likely that Trump will highlight the weakening of terrorist states in the Middle East and the decline in inflation caused by plummeting oil prices as he heads into the November midterm elections. If Trump stands to lose anything, it is only the stigma of violating international law—but such a stigma is precisely what Trump desires.

Policy toward China has become the top priority

What we should be considering now is the historical shift in the international environment that justifies such lawlessness. Underlying this is China’s remarkable rise and quest for global dominance. An era in which China—a one-party communist dictatorship with absolutely no freedom of speech, where every move of its citizens is monitored through advanced technology—governs the world alongside the United States has arrived; the G2 has become a reality. The dystopia depicted by George Orwell in his novel *1984* (published in 1949) exists right before our eyes.

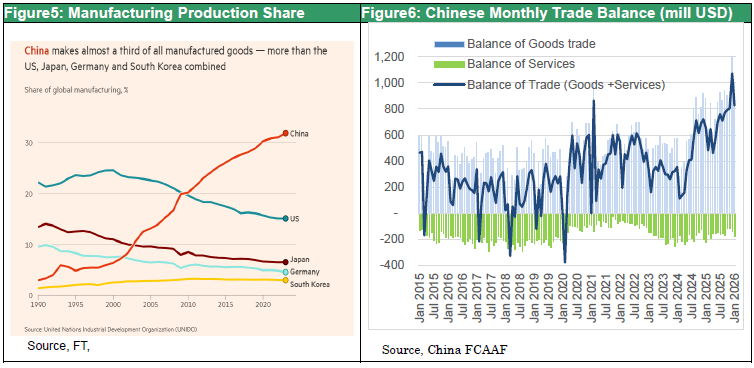

China, which accounts for only 17% of the world’s population, has amassed nearly 40% of global manufacturing output (more than double that of the U.S., according to Musha Research estimates based on PPP) and holds high global market shares: 50% in steel, 70% in shipbuilding, 80% in smartphones and drones, and 90% in PCs and TVs. This industrial power has enabled China to secure massive income and financial strength. In 2025, its trade surplus reached $1.18 trillion, accounting for 1% of global GDP. Over the past decade, $400 billion (300 billion in trade deficit payments plus 100 billion in net capital flows) has flowed annually from the U.S. to China, and this continues today. By channeling these funds into the Belt and Road Initiative, direct investment in the Global South, securities investments, and loans, China is exerting immense influence. China’s purchase of Russian crude oil and supply of goods to Russia have allowed it to circumvent sanctions against Russia, giving Russia the upper hand in the war in Ukraine. By importing 90% of Iran’s crude oil and 80% of Venezuela’s crude oil, China has brought these authoritarian states—which are on the brink of collapse—under its sphere of influence. The situation now appears to make the shift of hegemony from the United States to China virtually inevitable.

Figure 5: Trends in Industrial Production Share by Major Countries

Figure 6: Trends in China’s Trade Surplus

The U.S.-China conflict has reached a stage of total war, just one step away from open hostilities

Last year, President Trump attempted to diminish China’s industrial presence by raising tariffs on Chinese goods to 145%. However, he succumbed to China’s threat to cut off supplies of rare earth elements—materials essential to produce high-tech products, in which China holds a 90% global market share—and shelved nearly all trade sanctions against China. Faced with China’s industrial might, Trump had no choice but to make a humiliating policy reversal. If even the tool of tariffs cannot be used, what kind of approach should be taken toward China?

The surprise military operations carried out since the start of this year likely serve as a message that, under these circumstances, the United States is also stepping into a total war against China. These two operations have demonstrated the inadequacy of Chinese and Russian air defense systems, as well as the gap between them and U.S. intelligence capabilities and cutting-edge military technology.

President Trump likely believes that extraordinary measures, such as the exercise of force, are justified in pursuit of the overarching goal of winning the struggle for hegemony against China. Having demonstrated the overwhelming superiority of U.S. military capabilities during his visit to China in late March, President Trump is likely to steer the situation to his advantage.