Feb 29, 2016

Strategy Bulletin Vol.157

The End of Risk Aversion Due to China and Oil Has Arrived

G20 will quell the China crisis; Yuan stability, capital controls and more spending will be critical

The Shanghai G20 meeting that took place on February 26 and 27 will probably become a breakthrough event that ends the risk-off mood in financial markets. The communique states that “the magnitude of recent market volatility has not reflected the underlying fundamentals of the global economy.” The communique also states that all policy tools will be used to achieve market stability. This communique makes clear the determination of the financial authorities of all G20 countries to act together to combat speculators whose selling has caused prices to plunge. Participants also agreed that they will use fiscal measures and other new initiatives.

Criticism that the statement is short on specific actions is incorrect. The G20 meeting clearly demonstrated the desire to stabilize currencies and the willingness to tighten measures for monitoring and controlling movements of capital. As a result, China’s freedom to take actions, which has been the focus of attention, has greatly increased. Furthermore, this part of the joint statement is very significant: “Excess volatility and disorderly movements in exchange rates can have adverse implications for economic and financial stability.” For the just cause of preventing competitive currency devaluations and preserving the yuan’s value, China will probably not hesitate to enact capital controls.

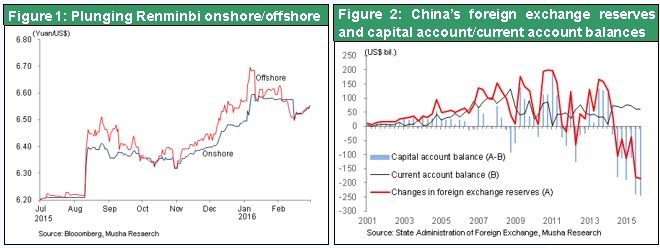

Taking this action will enable China to escape from the international financial trilemma and shut down the pathway for speculative sales of the yuan. George Soros thinks that a hard landing in China is unavoidable and expects a sell-off of the yuan, Hong Kong dollar and other Asian currencies. As a result, the yuan and matters involving foreign exchange have obviously become the key aspect of the China crisis. However, prospects for this situation to stabilize will probably improve going forward.

During the 19-month period from June 2014 to January 2016, China’s foreign exchange reserves plummeted by $760 billion, falling from $3.99 trillion to $3.23 trillion. During the same period, China had an estimated current account surplus of $400 billion. That means the total outflow of capital from China was a breathtaking $1.1 trillion. Everyone was watching to see if China could stop the rapid drop in foreign exchange reserves, the rapid growth in capital outflows and expectations for the yuan to decline. Now, the possibility of halting these events has emerged. If this happens, China may use numerous monetary and fiscal measures to restore economic growth. Consequently, the possibility of an international financial crisis originating in China is now much smaller (at least for the time being, but not from a longer perspective).

The consensus view is that crude oil has hit bottom; now oil will be a positive rather than negative factor

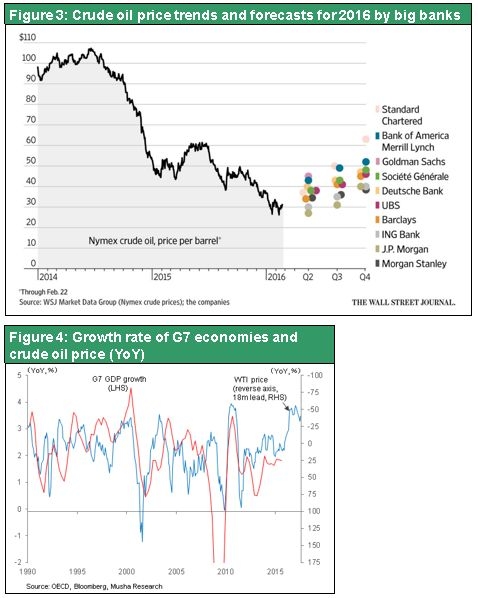

Crude oil as well will probably be a factor that reverses the global risk-off mood. First, there are unmistakable signs that the price of oil has stopped falling. Although the recovery is likely to be uneven, no one is predicting that the price will fall below the current $30/bbl (Figure 3). Whether the rebound is fast or slow, an upturn in the price of oil will reduce risk associated with oil-producing countries and resource companies. This will be good news for financial markets. Second, significant benefits of the lower cost of oil are about to appear in oil-consuming countries. As Figure 4 shows, there is a delay of about 18 months between a drop in the cost of oil and the emergence of economic benefits in industrialized countries. The price of oil started falling in the summer of 2014, so the benefits for U.S. households should finally start appearing about now.

We have reached the point where people will start using savings from cheaper gasoline for other expenditures. Since the summer of 2014, financial markets have viewed falling price of oil as bad news. Revenues of oil-producing countries and resource companies have decreased. Investors have focused their attention only on negative consequences like sales of stocks and other risk assets by oil-producing countries and the weaker currencies of oil and other resource-rich countries. The result was a big increase in risk-off sentiment. But from now on, oil will become a reason to switch to a risk-on stance. Investor sentiment will undergo a dramatic switch due to a double dose of good news: growth in revenues of oil-producing countries and resource companies and growth in demand in oil-consuming countries.

No more worries means the end of the risk-off mood of early 2016

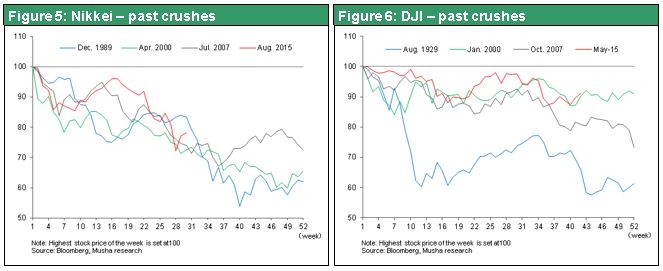

Plunging stock prices worldwide as 2016 started have terrified investors. Many people expect an economic and financial crisis of the same magnitude as the global financial crisis that began in 2008. From their highs in 2015, the Shanghai Stock Exchange Composite Index is down 49%, the Hong Kong Hang Seng Index is down 36%, the German DAX is down 30% and the Nikkei is down 28%. After China, Germany and Japan have suffered the biggest downturns. These stock market declines are all about the same as during the global financial crisis. (However, the U.S. Dow Jones Industrial Average is down only 15%, which is much less than the drop that occurred during the global financial crisis.) Stock prices have factored in the possibility of a 2016 global recession as well as an international currency crisis sparked by China.

For the foreseeable future, though, the probability of these events actually happening is very small. The health of the US economy makes a recession very unlikely. Moreover, China’s initiatives to end the crisis will probably be successful, so the yuan will remain steady and there will be no global financial crisis. Once investors are confident about these two points, the Nikkei is likely to stage a powerful rebound from its current trading range of 15,000 yen – 16,000 yen. We can expect to see a quick surge to ¥19,000 to ¥20,000, where prices were before the recent bear market. As the G20 communique states, financial markets today are factoring in too much risk. In particular, we may see a big recovery in Japanese stocks, which have been oversold as a substitute for dumping Chinese stocks.

The dollar/yen rate will also be part of this rebound. The consensus among investors has undergone a dramatic shift to expectations for the yen to strengthen. However, it is doubtful that the fundamentals have changed to the point that justifies this shift. Compared with Japan, the United States has higher interest rates and higher economic growth (Japan’s posted negative GDP growth in the fourth quarter of 2015). Furthermore, the Fed is raising interest rates while the Bank of Japan has introduced a negative interest rate. All indicators point to the superiority of the United States, which means a stronger dollar.

Nevertheless, the yen has appreciated rapidly. The reason is that financial markets reacted reflexively to events just like Pavlov’s dogs. During the past 20 years, the yen has always been bought as a safe haven during an economic downturn or global financial instability. In other words, people bought the yen whenever markets were in a risk-off phase. This is not a theoretical cause-and-effect connection. Instead, it is a well-established habit of investors. This time as well, the market was in a risk-off phase as people worried about China triggering a financial crisis and about a US recession. Once investors begin to anticipate a period of crisis, they instinctively start buying the yen. This is probably why the yen has strengthened. Therefore, if investors reject the possibility of a financial crisis and end their aversion to risk, we should automatically return to a world where the dollar rises and the yen falls.

The decisive US advantage: Sound credit

As a result, the key to this outlook is certainty about the US economy. Significantly, there are many positive factors involving US credit that underscore this certainty.

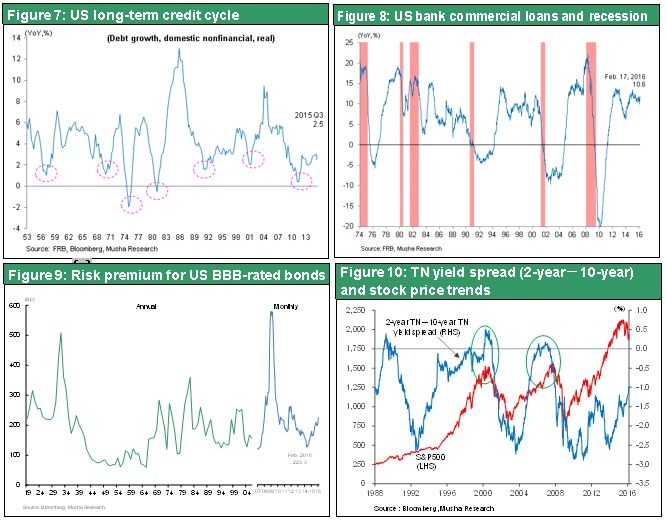

First, the US credit cycle is still in an expansionary stage. Numerous pessimists believe the credit cycle will stop growing as credit tightens because of the Fed’s December interest rate hike, the first in nine years. But as you can see in Figure 7, which shows the US credit cycle (real growth in debt) over the past 50 years, the US is still a long way from the end of this credit cycle. In the past, years ending with a one were usually the bottom of a cycle. So credit bottomed out in 1971, 1981, 1991, 2001 and 2011. That means we can expect the next bottom to occur five years from now in 2021. Looking back at the regular movements of the credit cycle in the past, it would be very difficult and unlikely for credit to stop growing at this point.

In addition to this regular pattern and experience, the current status of lenders and borrowers also points to a continuation in the growth of credit. On the lending side, there is obviously no reason for concern about the Fed reducing credit because of inflation worries or about banks cutting back loans because of worries about balance sheet soundness (Figure 10). On the borrowing side, there is currently an unprecedented capacity to take on more debt. This is evident in the interest coverage ratio (operating income divided by interest expenses). With operating income at an all-time high and interest rates at an all-time low, this ratio is now at the highest level ever recorded.

Never before have companies been in a better position to increase debt. This is not a time to repay loans. Instead, companies should obtain loans at favorable terms for buying back stock, acquiring other companies, making investments and other financial activities. Consequently, from the standpoints of past credit cycles and the status of lenders and borrowers, it is clearly very unlikely for the US economy to fall into a recession due to a credit crunch. This is a critical difference between the situation today and the environment during the global financial crisis.

Additionally, there are concerns about a chain reaction of financial worries caused by the deteriorating financial soundness of energy-sector companies, bankruptcies of these companies and non-performing loans to these companies. But these worries are overblown.

The risk premium of US corporate bonds can be gauged by watching movements in the corporate bankruptcy rate. Figure 9 shows the risk premium for BBB-rated bonds in the United States from 1919 to 2016. During the global financial crisis, the risk premium was higher than during the Great Depression that began in 1929, but dropped suddenly thereafter. Although the risk premium has subsequently recovered, it is still only at the historical average.

In this financial environment, it is logical to expect a risk-on phase and an upturn in stock prices. This is obvious if you look at the interest rate gap between US 2-year and 10-year Treasuries and movements in stock prices (the S&P500) as shown in Figure 10. When stock prices plunged in the past, there was a reversal of the yield curve as rising interest rates caused by tighter credit made short-term rates higher than long-term rates. This happened in 1997, 2000 and 2006. But today’s yield curve is nowhere near becoming negative.

This leads to the question of why speculative sales and a risk-off stance were so successful even in the midst of such a favorable credit environment. The answer is that large numbers of market participants showed contempt for central banks. They believed that central banks could no longer do anything because any action they took would be ineffective. As a result, investors established positions that challenged central banks. But is this belief justified?

“Don’t fight the Fed” is a well-known maxim among US investors. It means that an investor who goes against actions by a central bank will lose. This is true for all market conditions and all financial markets in the world. The reason is that central banks are responsible for producing results. Central banks have unlimited ammunition for achieving their goals. This is why central banks are not at all like market observers and irresponsible commentators and speculators.

For the reasons outlined in this bulletin, I believe that once the risk-off mood that dominated global financial markets early in 2016 switches to a risk-on sentiment, investors can expect to see a dramatic reversal in the direction of these markets.