Jan 25, 2021

Strategy Bulletin Vol.272

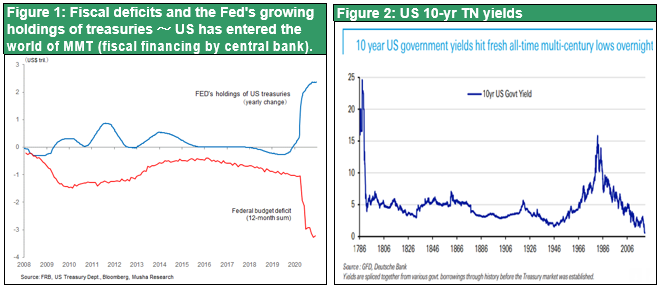

Japan must reflect on the Copernican turn in government debt theory

- A Yellen-Powell coalition will provide strong support for stocks

The comments by incoming Treasury Secretary at her January 19 congressional hearing may mark the beginning of a Copernican turn in government debt theory. Yellen asserted “Although debt will increase with large-scale economic stimulus measures, with interest rates at historic lows, the smartest thing we can do is act big. In the long run, I believe the benefits will far outweigh the costs.”

(1) Treasury Secretary Janet Yellen's Declaration of Debt Acceptance

Interest burden is more important than outstanding government debt

The following is an extract from Howard Schneider’s column on Reuters (January 21, 2021).

Her [Yellen] more extensive comments defending President Joe Biden’s $1.9 trillion coronavirus spending plan, however, reflected a steady shift in economists’ thinking about the mountains of government debt across the developed world that has been underway for a decade and has roots in the near collapse of the euro zone. Yet, in her testimony to Congress, Yellen said “the smartest thing we can do is act big.”

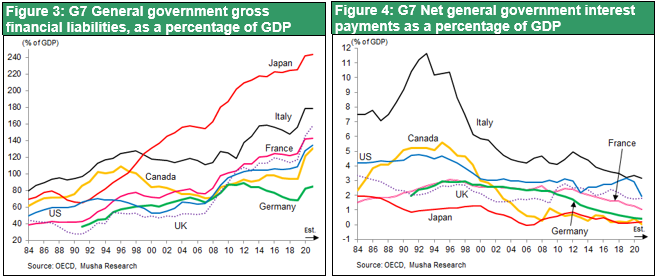

Forget about the amount being borrowed, Yellen, a former Federal Reserve chair, told members of the Senate Finance Committee. Focus instead on the interest rate being paid and the returns it will generate, an approach that argues the country’s future economic potential can support more borrowing today and makes the roughly $26.9 trillion in U.S. IOUs seem less formidable. The interest burden of the debt as a share of (gross domestic product) is no higher now than it was before the financial crisis in 2008, in spite of the fact that our debt has escalated,” Yellen said. “To avoid doing what we need to do now to address the pandemic and the economic damage that it is causing would likely leave us in a worse place ... than taking the steps that are necessary and doing that through deficit finance.

Federal government interest payments are now nearly $600 billion annually, but historically low global interest rates have kept them roughly stable as a share of the country’s economic output since the 1990s. That fact will be front and center when Congress debates Biden’s spending plan, and in particular will test whether Republicans remain willing to spend more to battle the pandemic now that they’ve lost control of both the White House and Congress to Democrats.

IMF reflects on recommendations to reduce budget deficit

In fact, at least among Yellen’s economic peers, there has been plenty of talk about the issue since the 2007 to 2009 financial crisis and recession, and the troubles in the euro zone that followed. When a group of smaller European countries, Greece in particular, ran into trouble repaying their debts in the aftermath of the global financial crisis, the response of larger euro zone members and the International Monetary Fund was to insist those nations make deep cuts to government spending. Instead of fostering a recovery, that harsh dose of austerity helped drive Greece into an even deeper hole, and in fact made its deficits worse. In hindsight, the IMF said it got it wrong. After extensive research, Olivier Blanchard, then the IMF’s chief economist, eventually concluded government spending can have outsized benefits, particularly in moments of crisis when overall demand for goods and services is weak - as is the case now.

If growth rate > interest rate, public investment should be made

Fast forward a few years. Previously unorthodox ideas, such as Modern Monetary Theory (MMT), that see a broader, stabilizing role for government spending began getting more attention, and mainstream economists began to rethink their views about debt in more fundamental ways. Blanchard, for one, started arguing that when interest rates are lower than an economy’s rate of growth - the case in many developed nations - countries shouldn’t hold back on well-conceived public investments.

The testimony by incoming Treasury Secretary Yellen is an invitation to bring this heretical argument to the policy center in Washington.

(2) Chairman Powell also supports this turn in government debt theory

Fed Chairman Powell Concurs with Yellen

In concord with Yellen, Fed Chair Jerome Powell has also taken a fresh look at the fiscal debt debate. Powell denied the possibility of fiscal risks materializing in the coming years, arguing that both economic recovery and fiscal sustainability are important and that although the ratio of government debt to GDP is high, the cost of government debt is under control. As for the possibility of Congress requiring the Fed to maintain its low interest rate policy as the debt burden increases, he pointed out that the current situation is not one of "financial repression" and that the Fed can focus on achieving its policy goals for prices and employment (press conference after the FOMC meeting on December 17, 2020).

In January, when Chicago Fed President Evans, Atlanta Fed President Bostic, and others said that tapering was possible at the end of 2021 or in 2022 if conditions were favorable, Chair Powell immediately denied it, saying, "Now is not the time to discuss exit. I think that is another lesson of the global financial crisis - is be careful not to exit too early (from monetary easing)" (comments made on January 14).

Powell is also said to have expressed understanding of the argument that government debt levels were a long-term concern before he became Fed chair, but now he is taking a major turn.

WSJ looks at the Yellen-Powell partnership

The Wall Street Journal (WSJ) expresses caution about the collaboration between the Treasury and the Fed in reviewing the government debt theory. "Ms. Yellen worked with current Fed Chairman Jerome Powell during the Obama years, and they are likely to form a mind meld on fiscal and monetary policy. This will be good for Ms. Yellen's policy influence, but the same can’t be said for Fed independence. The Fed seems to be returning to the role it played before the famous Accord in 1951 when the Board of Governors agreed with the Treasury to separate its financing of government debt from monetary policy. This created what we came to know as the modern Fed. But nowadays the Fed is financing federal debt with enthusiasm, and Mr. Powell is signaling he’ll do as much of it as the politicians want.

With her ties to the Fed governors, and especially the Fed staff, Ms. Yellen is likely to have even more influence than most recent Treasury chiefs. This will be a good line of inquiry at her Treasury confirmation hearing.” (Opinion, Wall Street Journal, November 23)

The WSJ and the Republican Party are wary of fiscal and monetary coordination, but this does not necessarily mean they are right. The WSJ has been a staunch critic of QE, and there is some confusion in its editorial, such as when it defended the appointment of Judy Shelton, an advocate of a return to the gold standard, as a Fed governor. The Democrats are more consistent on macroeconomic policy than the Republicans. Yellen's pronouncements are consistent with the macroeconomic policies of the Democrats, who advocate big government, while the Republicans' macroeconomic policies have been lacked coherence under the Trump administration. This has spanned from opposition to QE and expressing an understanding of a return to the gold standard to criticism of Powell's rate hikes. Contrary to the Tea Party's criticism of the budget deficit and the party policy of pursuing small government, Trump increased the budget deficit.

(3) Flexibility in US policy choices: Japan is the one that needs a policy shift

US economists and policy makers committed to practical learning

In this way, US economists have reflected on the situation and gracefully changed their own theories. It is as if the US is the only country where economists can easily revise their previous theories. In the US, economics is a real science, a tool for deriving correct policies and investment/business strategies. By contrast, Japanese experts have no flexibility at all. Unlike the US, there is a tendency in Japan for economics to be regarded as metaphysics (something that exists without any connection to the real world), even if not referred to as a soft science.

The Nikkei editorial is typical of Japanese opinion leaders who are out of touch with the real world

Even after COVID-19, Japan remains unchanged proceeding with discussion in marked contrast to the US. In a January 23 editorial titled "Can't we face up to the reality of deteriorating public finances?" the Nikkei scolded the Japanese government for its lax stance on deficit reduction.

The gist of the article is that "The government has compiled medium-to-long-term economic and fiscal estimates. The primary balance (PB) of the national and local governments is expected to turn into a surplus as early as fiscal 2029. However, the assumptions for the economic growth rate and other factors are generally weak, and the estimates cannot be said to be reliable. The PB deficit will grow from ¥14.6 trillion in FY2019 to ¥69.4 trillion in FY2020 due to the economic measures taken in response to COVID-19. If the government can thereafter maintain an average annual growth rate of over 3% in nominal terms and over 2% in real terms, it will have a surplus of ¥0.3 trillion in FY2029 (but this is unreliable). ・・・・ can be criticized for not facing up to the harsh reality and covering it up with a naive outlook.

Individuals and companies in need should now be firmly supported. This is not the time to hesitate to mobilize the national and local governments to do so. However, the government also has a responsibility to correctly communicate the plight of its finances. ・・・・ The outstanding long-term debt of the central and local governments has ballooned to around ¥1,200 trillion, almost twice the size of Japan's gross domestic product (GDP). The deterioration of Japan's finances is more serious than any other major country, and the situation is not at all optimistic. If we overburden the public finances, even during a crisis, the bill will eventually come due. In addition to maintaining discipline and moderation through short-term budgetary measures, it will eventually be necessary to undertake full-scale revenue and expenditure reforms. If the government continues to set estimates and targets that are out of touch with reality, it will not be able to take the next step.”

Thus, the Nikkei editorial insists that government should convey the plight of public finances at a time when Ms. Yellen insists that "the smartest thing we can do is act big.” This argument focuses not on the cost of interest payments, which is Yellen's focus, but only on the government debt, which she says should be shelved. It is a bad argument that lacks balance.

Japan's interest payment cost is the lowest among advanced countries

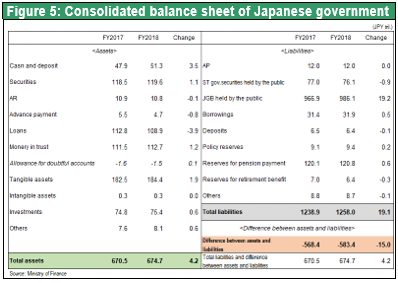

As shown in Figure 3, Japan has the world's worst absolute gross government debt (as a percentage of GDP), with a gross government debt ratio of 225.3% for Japan and 108.4% for the US according to the OECD (2019). However, in terms of net interest cost (as a percentage of GDP), which Ms. Yellen is now placing greater emphasis on, Japan's 2019 rate of 0.08% is the lowest among advanced economies and well below the US rate of 3.16%. (Figure 4). Japan has the most scope to expand its fiscal spending among the G7 nations. If the Nikkei had based its argument on this fact, it would have come to the opposite conclusion that more fiscal stimulus is needed.

MOF propaganda hides net debt

But what is even more disturbing upon closer inspection is the gap between Japan's gross debt (as a percentage of GDP) and net interest expenditure (as a percentage of GDP). In the past, when Japan was the outlier with its low interest rates, it seemed reasonable that interest payments would be low even if debt were high. However, it is strange that only Japan is able to maintain low interest payments that are far lower than its debt, while other developed countries in Europe are experiencing even lower interest rates than Japan. What is going on? Could it be an indicator of excessive debt? Almost half of the ¥1,200 trillion in government debt referred to in the Nikkei editorial is debt that does not accrue interest payments (or is offset by interest income), and the net debt is only ¥600 trillion. Looking at the integrated balance sheet of the Japanese government sector (FY2018) in Figure 5, total debt is ¥1,258 trillion (225% of GDP), but when subtracting assets (many of which generate interest) of ¥675 trillion, net debt drops to ¥583 trillion (104% of GDP). It is also possible that the overestimation of Japan's debt is a fabrication (!) by the Ministry of Finance. The Nikkei editorial, which is based on this false debt assessment, is making a double error.

(4) Legitimacy of introducing MMT - stimulating demand by utilizing surplus funds through both expansionary fiscal and monetary policies

Introduction of MMT, the best prescription for excess supply and excess savings

The introduction of MMT, which has already taken root in advanced countries, has been criticized for causing higher interest rates and inflation, which would lead to government bankruptcies, but for the time being, such fears are unfounded. Before the COVID-19 outbreak, the world economy was facing two fundamental problems: downward pressure on prices = lack of demand, and downward pressure on interest rates = too much savings. The shortage of demand was caused by the technological revolution of the internet, AI, and robotics, which boosted productivity and increased supply capacity. The decline in interest rates was caused by high corporate profits (value added by companies due to higher productivity) and excessive household savings, which delayed purchasing power. Therefore, it was necessary to stimulate demand by utilizing surplus funds through both expansionary fiscal and monetary policies. If the pandemic is an opportunity to utilize the capital and supply that have been idle, the economy should improve to better levels than before COVID-19.

MMT advocates argue persuasively that the obsession of academics, the media, and economists with the idea that budget deficits are bad has led to destructive policies in economies with large surpluses of supply and savings, such as Japan and other advanced economies today, that are not based on fundamental analysis. (For example, Professor William Mitchell, Newcastle University, "The Corona Crisis and Fiscal Expansion (1)," Nikkei Inc. Economic Classroom, December 22, 2020)

MMT likely to succeed and become a new means of financing

Musha Research believes that there is a strong possibility that the current fiscal financing (MMT) of advanced countries will achieve its policy objectives without a collapse. In the US, in particular, the animal spirit is still alive and well, as (1) lower interest rates lead to higher housing demand, and (2) the expected inflation rate has hardly declined even under COVID-19. There is a strong possibility that fiscal and monetary support will greatly boost demand, narrowing the output gap and realizing the Fed's desired 2% inflation target. In this process, long-term interest rates are likely to rise above 2%. In this way, MMT will prove its policy effectiveness and become an established means of financing spending in areas such as education, new technology development, and new social safety nets.