Oct 19, 2021

Strategy Bulletin Vol.292

Stronger dollar and weaker yen will improve Japan's price competitiveness and boost corporate profit

(1) Moving into an era of a strong dollar, the changing role of the US, from a supplier of dollar liquidity to a creator of demand

Global locomotive role shifts from China to the US

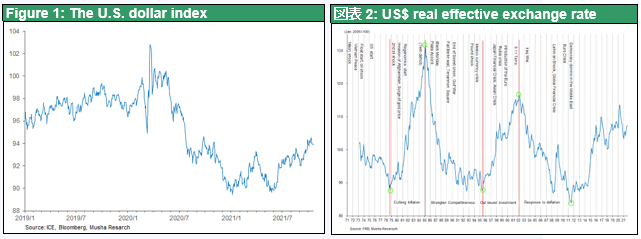

With the tapering of the US economy finally in sight, the era of dollar appreciation may have begun. The dollar index has risen by 5% since the end of May (Figure 1). The period when the US supplied the world with dollars in response to the Corona crisis and the dollar weakened as a result is over. The IMF's latest forecast for 2022 is 5.6% for China and 5.2% for the US. The IMF's latest October forecast for 2022 is 5.6% for China and 5.2% for the US, but Chinese slowdown in construction and real estate, triggered by the Evergrande Group crisis, could make the downturn even worse. On the other hand, US consumption is booming, and the locomotive of the global economy is shifting from China to the US.

The dollar is the U.S.'s secret weapon, and the confrontation between China and the U.S. will require a strong dollar

There may not have been many times when it has been so difficult to find a rationale for the dollar's weakness because of the many factors behind its strength. First of all, (1) with the end of ultra-easy monetary policy in the US, real interest rates in the US are expected to rise. In addition, (2) a strong dollar is advantageous for controlling inflation, and the dollar has been strongly linked to the price of oil (during the second oil shock, a sharp rise in the dollar offset higher oil prices), and (3) a change in the US policy mix (a shift towards tighter monetary policy and fiscal expansion...although not a marked one) is also a factor in the dollar's strength.

Perhaps most importantly, the dollar is the US's secret weapon. The dollar has at times been used to achieve US geopolitical objectives. In the past, the dollar was used against Japan, and now it is used as a strategy in the US-China conflict. We believe that a strong dollar is essential to the US's most pressing priority: building a global supply chain that excludes China. The temporary depreciation of the dollar during the Corona period is over, and the long-term trend of dollar strength that began at the bottom of 2011 will continue (Figure 2).

(2) The beginning of the era of yen depreciation

The yen's depreciation will be even greater than the dollar's appreciation, to 120-130 yen

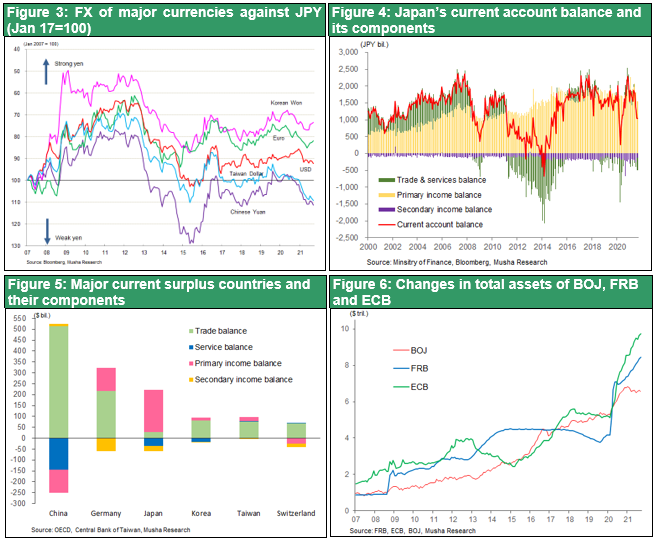

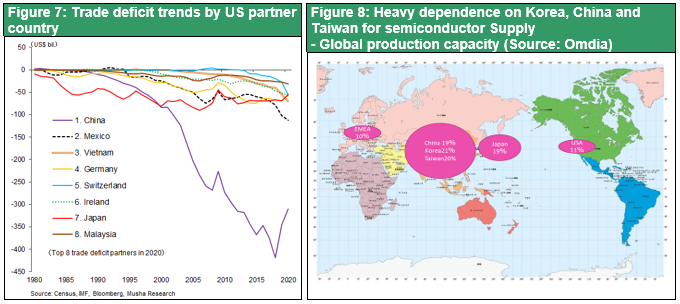

However, the Japanese yen has weakened not only against the dollar but also against other currencies. A year before the dollar began to appreciate, the yen had already begun to weaken (Figure 3). On the Japanese side, there are many more reasons for the yen's depreciation than the dollar's appreciation. (1) Japan's trade surplus has almost disappeared (Figure 3); (2) the current account surplus is mainly the income balance, which is reinvested locally and does not return to Japan (Figure 4, Figure5); (3) Japanese companies are allocating huge amounts of their retained earnings to global direct investment and capital outflows continue; and (4) Japanese securities investors are also aggressive to invest in the US. equities and treasuries.

While the world's major central banks, including the Fed and ECB, have been expanding their balance sheets since the beginning of 2021, only the Bank of Japan has been secretly reducing its asset purchases (stealth tapering) (Figure 6). The yen should be appreciating, but instead it has been weakening. The days of the yen as a safe haven asset may be over, and we may be looking at 120-130 yen to the dollar.

The US knows that a weak yen is the key to overcoming deflation and reviving Japan's economy

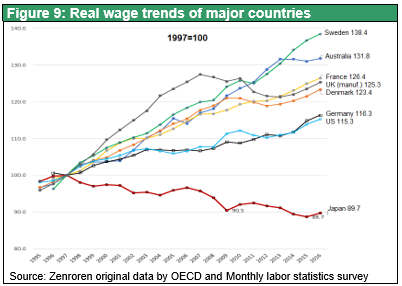

The US probably knows that a strong yen is the biggest cause of Japan's deflation and that a weak yen is the key to overcoming deflation. The question is whether the US will tolerate a weaker yen. A strong Japanese economy is essential in the face of the confrontation between the US and China, and the US must sincerely hope that Japan can overcome deflation. In addition, shifting the high-tech supply chain for semiconductors and other products, which is concentrated in the danger zones of China, South Korea and Taiwan, to the safe zones is an urgent issue, and the development and strengthening of high-tech industrial clusters in Japan is an important pillar (Figure 8). TSMC's decision to build a plant in Kumamoto as a joint venture with Sony is an important step in this direction. The Japanese government will reportedly subsidise 400 billion yen, half of the total investment of 800 billion yen, because of the high cost in Japan. However, if the yen falls to 120-130 yen to the dollar, Japan's cost inferiority will disappear.

(3) Japan's price competitiveness continues to be greatly enhanced

Weak yen in addition to "cheap Japan" has strengthened the price competitiveness of Japanese companies.

As we have reported many times before, Japan's low prices and low wages have been conspicuous. As a result, Japan ranks last with Italy in the G7 in terms of average wages, and was overtaken by South Korea in 2015, a gap that continues to widen (Figure 9). In addition, the price of a Big Mac is about half that of Switzerland, the highest, and cheaper than South Korea and Brazil. Diamond magazine reports that not only prices and wages, but also share prices and real estate prices have become bargains and are being bought up by foreign capital.

The weak yen will make "cheap Japan" even cheaper. Both "cheap Japan" and the "cheap yen making cheap Japan even cheaper" are in themselves the result of Japan's decline and are not desirable. But from the point of view of future prospects, they are good news for Japan. This is because, while international price competitiveness is undoubtedly the key to the rise and fall of any nation's economy, a "cheap Japan" and a weak yen will increase Japan's international competitiveness and create a virtuous circle for the Japanese economy. Expensive Japan and a strong yen were the starting point of the vicious circle. "The high cost of living in Japan has been made even more expensive by the strong yen, which has dramatically reduced Japan's price competitiveness. The root cause of Japan's decline was clearly the decline in price competitiveness, which was caused by the "high price of Japan" and the strong yen.

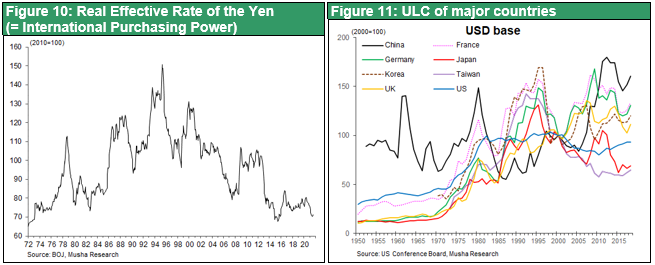

The real purchasing power of the yen (i.e. the cost of doing business) has returned to its level of 50 years ago.

In a feature article entitled "Cheap Japan: The era of the ultra-weak yen" (5 October), the Economist Weekly describes how the weak yen is reducing the purchasing power of the Japanese people and making them poorer as they are unable to raise their wages. The yen has depreciated in spite of deflation, so that in real effective terms the current level of 110 yen to the dollar is roughly equivalent to the level of 360 yen to the dollar before the change to a floating exchange rate system in 1973. In other words, the purchasing power of the yen has fallen to the level of 50 years ago (Figure 10). "The widespread reaction has been, "This is a disaster, this is a problem.

Japan's unit labor cost has fallen the most in the world since 2000

The opposite is probably true. This means that the price competitiveness of Japanese companies has returned to the era of 360 yen to the dollar. As can be seen in Figure 11, Japan's unit labor costs in dollar terms, which are a clear indicator of the price competitiveness of its manufacturing industry, have declined the most in the world since 2000 and manufacturing costs in Japan has declined more than China, Korea , US and Germany over the past 20 years. And further yen weakening would improve Japan’s price competitiveness further.

Corporate profit margins already back at record levels

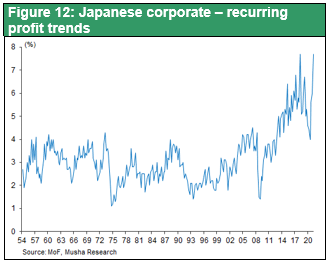

The weaker yen, combined with lower prices and wages, means that Japanese companies are now more price competitive than at any time in the last 30 years. The benefits of a weaker yen come in the form of higher yen equivalent of overseas corporate profits for companies that produce overseas. Already, corporate recurring profit margins have recovered to their highest level in April-June 2021, before the economy recovered from the Corona shock (Figure 12). Further improvements are almost certain and will lead to higher wages as companies become more solvent and the supply and demand for technical workers tightens.

The improvement in international competitiveness is likely to manifest itself in global manufacturing and in domestic tourism-related industries, which are expected to expand rapidly in the next few years. The important thing now is to sustain the ultra-easy monetary policy as long as possible in order to weaken the yen.

(4) Price competitiveness is particularly strong in relation to domestic demand, with high expectations for inbound business

Extremely low prices for services in Japan

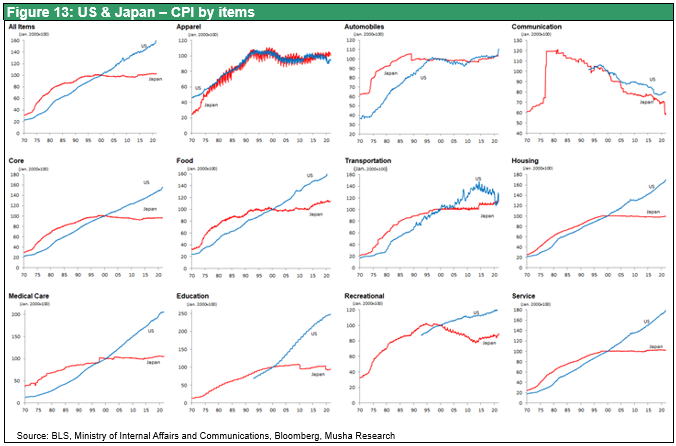

"Cheap Japan" is particularly pronounced in Japan's domestic demand industry and service prices, and the cost performance of tourism in Japan is considered to be extremely high by foreigners. A comparison of domestic and foreign prices, i.e. the gap in prices between Japan and the US, shows that the prices of manufacturing products such as cars, clothing, toys, televisions and computers are almost the same. The difference between Japan and the US is solely in the price of domestic services. While the price of a smartphone or a car in Japan and the US is not very different, there are extreme price differences in services such as restaurant prices, transportation, health care and education. For example, a bowl of ramen costs 500 yen in Tokyo and 2,000 yen in New York (Figure 13). The reason why there is such a huge gap in the prices of domestic demand-type services is that foreigners cannot buy Japan's cheap domestic demand-type services, and the undervaluation of Japan's domestic demand prices has not been corrected.

Foreigners know that "there is no place as cheap, safe and delicious as Japan"

However, the rise of cross-border tourism has led to a welcome shift in the way Japan's domestic demand is met by foreigners, something that would have been unthinkable 10 years ago. Travelers from all over the world have discovered that there is no cheaper, safer or tastier place to travel than Japan. After the end of the Corona pandemic, tourism demand will soar as people seek out Japan's low-cost, high-quality tourism resources and services. In other words, Japan's domestic demand (i.e. domestic industry) will open its doors to global demand. This will lead to a significant correction in the level of domestic service-related prices, which have been left at a significantly undervalued level.

For more on the reasons for the large differences between domestic and foreign prices, see our supplementary article, "Japan's tourism sector is particularly good at cost-cutting; the Balassa-Samuelson hypothesis works".

Criticism of "cheap Japan" and "weaker yen" is wrong

Criticism of "cheap Japan" and criticism of the yen's weakness to make "cheap Japan" even cheaper swirl around the debate, confusing causality with tautology. Both "cheap Japan" and the weak yen are the result of the decline of the Japanese economy, which in itself may be undesirable. Yukio Noguchi, for example, argues that "the idea that a weak yen is desirable is wrong. From the consumer's point of view, it reduces purchasing power. It also discourages Japanese industry from adding value through innovation and makes it impossible to attract talented foreigners." (Weekly Economist), but that is only the result.

The biggest bullish factor for Japan

Among the many factors that surround us today, it is essential to sift through the facts based on cause-and-effect analysis to determine what is a result of what happened in the past and what is a cause of what will happen in the future. Again, Musha Research believes that the most important factor in the analysis of each country's economy as a cause of the future is international price competitiveness, which is one of the most bullish factors for Japan's future.

The Balassa-Samuelson Theorem is alive and well in Japan's tourism industry, which is particularly good for business.

The reason why Japanese domestic prices are so attractive to foreigners can be interpreted in terms of the Balassa-Samuelson hypothesis of international economic theory. It starts from the principle that world wages are one price and that two countries with identical labor productivity will have identical wages. However, this is only true for tradable goods (mainly manufacturing) which are mutually competitive in the international market. Then, how is the wage of the domestic demand industry of each country, such as the service industry, which does not compete in the international market, determined by the domestic wage rate formed in the trade goods industry of the country? In other words, if the productivity of country A in the tradable goods industry is twice that of country B, the wage in the tradable goods industry of country A will be twice that of the tradable goods industry of country B. The wage in the service industry of country A will also be twice that of the wage in country B. This means that wages in the service industries of countries A and B will be determined independently of their productivity. In general, the productivity of service industries, for example barbers, is not very different in developed and emerging countries. However, the wages of a barber in a developed country can be ten times higher than in an emerging country. This means that the wage-price per unit of productivity gap is particularly wide in the service sector.

However, if international exchange becomes more active and the service sector attracts foreign customers, the situation will change foreign demand will rush to the cheaper service sector in country B (where productivity is not much different but prices are half as high). It is clear that Japan's tourism-related prices are much cheaper than those in other countries, so tourism demand will increase significantly. It is expected that the "cheap Japan" will be greatly corrected by the external demand that appears in the domestic industry of tourism. In this way, "Cheap Japan" will increase the upside pressure on domestic industries even more than on manufacturing. We believe that the flourishing tourism industry will be the driving force behind Japan's overcoming of deflation.